Overview

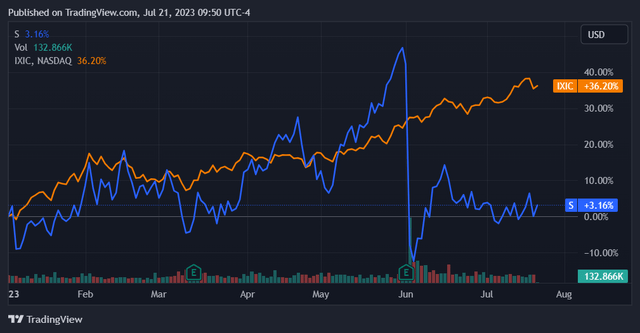

SentinelOne (NYSE:S) stock started the year off strong but depreciated significantly after its latest earnings report, one in which it exceeded consensus EPS expectations but failed to match them on revenues. While trading choppily throughout the year and well exceeding the NASDAQ Composite in the run up to its fiscal Q1 2024 earnings release, the stock cratered after the print and is now trailing the index. Price action since then has seen the stock regain some of its lost value.

Seeking Alpha

Such a steep sell-off directly after an earnings report indicates that there is something that investors didn’t like in the quarterly filing. While SentinelOne did miss against consensus revenue expectations, it only did so by 2.4%. As such there may very well be other elements of the latest earnings report that investors found disconcerting. While it has been nearly two months since the fiscal Q1 ’24 earnings report, there is no clear consensus on what drove the depreciation. In this article I will ascertain what elements were likely culpable and whether they are as significant as the market has so far been implying. Additionally I will compare SentinelOne to its peers in order to determine if it’s a good investment at current prices.

The Earnings Report and The Sell-Off

While it may be fair to say that the company’s miss against revenue expectations is what drove the sell-off, I would like to investigate further. Nonetheless, I will say that this revenue miss was certainly a material factor in driving down the price of this stock; SentinelOne is a fast-growing company and most definitely a growth stock. As such it is sensible that an underperformance in revenue growth drove a significant sell-off in its shares.

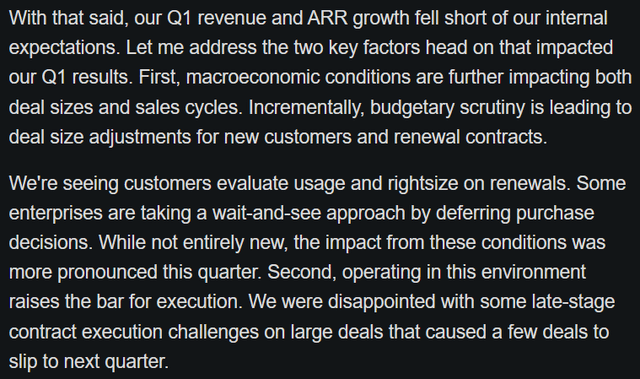

Reviewing the earnings transcript, we see that the company made reference to the macroeconomic environment as well as stalled deals. Management was explicit in saying that at least one sales process was pushed in to next quarter as a result of budgetary tightening.

Seeking Alpha S FQ1 ’24 Transcript

Overall, this commentary by the CEO makes it sound as if SentinelOne is in for a difficult few quarters. This appears to have cast a shadow over SentinelOne’s near-term prospects. Combined with lower than expected revenues for the quarter, investors are likely pricing in a material slowdown in the firm’s growth.

Looking further, however, I believe that the picture is more nuanced. For one we must note that SentinelOne still grew revenues at an astounding 70.5% y/y in this quarter. While this is a drop-off from the recent historical trend, which has up until the quarter prior been in the triple digits, it is nothing to scoff at.

Seeking Alpha

Additionally, customer growth overall was still robust, growing at 43% y/y in the most recent quarter. Also worth noting is that SentinelOne added another member of the Fortune to its customer base and is now providing services to half of the 10 largest companies in the US. Customer acquisition was evidently still good.

For a SaaS company like SentinelOne, however, revenue retention is just as important as customer acquisition. Here the number declined quarter/quarter. While net revenue retention (NRR) was over 130% in fiscal Q4 2023, this number declined to 125% in the most recent quarter. This implies less marginal revenues from existing customers.

Overall it seems that SentinelOne’s revenue growth prospects faced multiple headwinds in the most recent quarter. Investors likely balked at a combination of lower than expected revenues as well as a lower net revenue retention rate. That combination implies slower growth from both existing and new customers and is likely what drove down the stock.

Comparative Financials

SentinelOne can be compared to other pure-play cybersecurity companies in order to determine its prospects as well as its relative valuation. This makes for six stocks in total, of which SentinelOne is the smallest by market capitalization.

Seeking Alpha

For further context we can note that SentinelOne stock has been the worst performer of the bunch YTD. Prior to the steep sell-off it looks to have maintained a price return somewhere slightly above the average.

Seeking Alpha

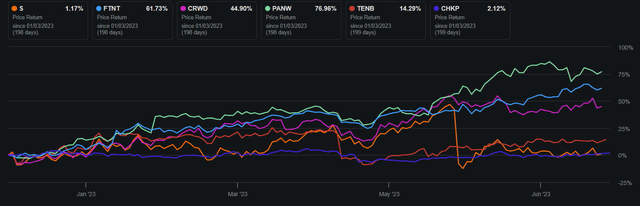

Moving on to comparative metrics, the picture immediately changes. SentinelOne is the fastest-growing company in this group by a large margin. It has outpaced its peers on one year trailing revenue growth, one year forward growth expectations, and its trailing 3 year compound annual growth rate.

Seeking Alpha

This additional context makes it clear why revenue growth is such an important metric for the company – investors likely have bought into it because it is leading the pack in this regard. It maintains this leading position.

These growth metrics reflect the reality of SentinelOne being an earlier stage company than its peers. For context, it only conducted its initial public offering in Q2 2021. This also means that it is not yet profitable, like most of its peers, and is also further away from profitability than the rest:

Seeking Alpha

Additionally, it is the only company in this set that is not yet cash flow positive:

Seeking Alpha

This is due to the fact that SentinelOne is earlier in its business lifecycle than its peers. Indeed, the company continues to lose cash from operations and has not yet established a clear trajectory in this regard.

Seeking Alpha

This financial context makes it difficult to readily compare SentinelOne against its peers. Since we have neither positive earnings nor cash flows, we can’t establish a multiple for the shares that we can then compare against the rest. This is also the case for margins, which are too far removed from where they will end up being to be of much use. The stock is then set to continue trading purely on the basis of its growth prospects, which form both the downside (RISK) and the upside for this stock.

Risks

As mentioned above, we cannot readily compare SentinelOne to its peers – it is simply a company in a different stage of its lifecycle than the rest. Since revenues and revenue growth are all that investors have to go off of, that is what’s driving the stock and will continue to do so. This further reaffirms the logic of the negative price action that the stock experienced in the wake of its latest earnings report.

The risk, then, is centered around growth. If SentinelOne continues to miss expectations on growth, the stock will likely sell off further. If revenue growth rates deteriorate to somewhere closer to its peers, it will be particularly bad for the stock; it will then be missing its central differentiator.

Conclusion

While we may not have a price/earnings ratio or a cash flow multiple for SentinelOne, we do have another metric – price/sales. While I am generally much more careful with valuations using this metric, they can still be useful and certainly are here. This gives us an idea of the price that the market is putting on SentinelOne’s current (and future) revenues.

Seeking Alpha Seeking Alpha

Here we can see that SentinelOne is trading more cheaply on a price/sales basis than 3 of its peers but less than two of them – Tenable Holdings (NASDAQ:TENB) and Check Point Software (NASDAQ:CHKP). There is not a clear logic to this, as Tenable Holdings and Check Point have materially divergent growth rates from each other. SentinelOne nonetheless exceeds both significantly.

Of course, SentinelOne exceeds the other 3 companies in terms of revenue growth rates as well. There is again no clear pattern here. This is additionally made more complex of a comparison as we are considering future revenues. This is sensible to consider because valuations include future prospects baked in to current prices, and we can expect the same with the price/sales multiple. Prior to its sell-off SentinelOne maintained a price/sales ratio much closer to that of its larger peers; a back-of-the-napkin calculation yields a price/sales ratio of 12.43 at its pre-earnings share price of $21.21.

This means that the market is now discounting SentinelOne’s future revenues much more than before. This does not seem warranted. Considering that the company is still the fastest-growing one in its peer group by a large margin, along with the ongoing traction that it is seeing with the largest customers, make me inclined to think that this discounting by the market is short-sighted. The nature of compounding is such that SentinelOne will be a lot closer to its peers in terms of overall revenues if it can maintain the growth rates that it posted in its most recent quarter. Essentially I think SentinelOne still has a robust and growing business that has not been disproven by a few underperforming metrics in its most recent quarter. On a forward basis, this level of compounding in its revenues should see it do well. This should get reflected in its share price over time.

I am inclined to take the optimistic view here and believe that this stock has been oversold. The growth thesis for this company is still alive and well, and a few blips don’t disprove it. While the timeframe for share price appreciation is not particularly certain, I think SentinelOne will do well over the long-term. On the basis of it continuing to grow, and returning to parity or above as to revenue expectations, its shares should climb back up. This will take at least 1 year and possibly longer. On that horizon I am calling it a buy.

Read the full article here