It was a strong quarter for emerging markets (EM) debt despite a mixed economic backdrop around the world. Market volatility subsided, aiding investor demand for higher-carry strategies. Positive EM debt performance was even more impressive, in our view, in the context of rising U.S. Treasury yields and poor investment flows.

A View of the Potential Opportunities: Overweight/Underweight

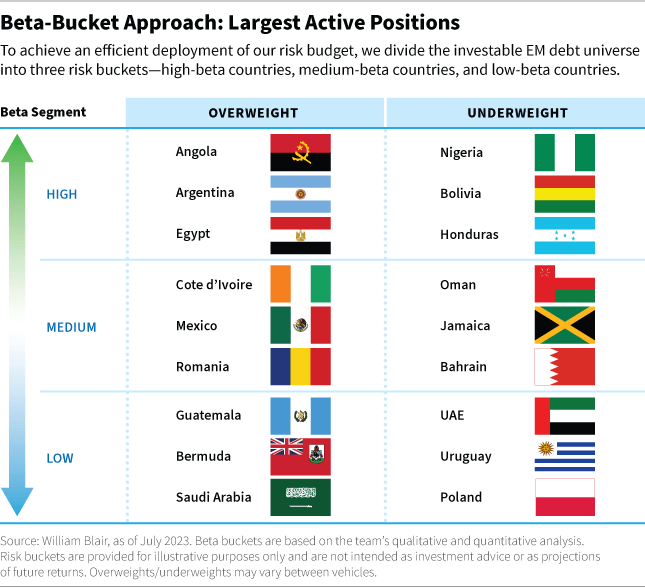

As we make our way through the third quarter, we continue to see value in high-beta, high-yield credit and are positioned for high-yield/investment-grade spread compression – although we continue to see scope for fundamental differentiation, and prefer countries with easier access to multilateral and bilateral funding. Our highest-conviction overweight and underweight positions are shown in the table below.

High-Beta Bucket

In the high-beta bucket, our largest overweight positions are in Angola, Argentina, and Egypt, and our largest underweight positions are in Nigeria, Bolivia, and Honduras.

Angola (overweight): Authorities have a strong commitment to fiscal discipline, and we believe the flexible exchange rate could help macroeconomic performance.

Argentina (overweight): The outlook is starting to look more promising. Although a shortage of dollars has led to exceptionally challenging macroeconomic conditions, it appears increasingly likely that a more pragmatic government will assume office in 2024. Minister Sergio Massa has traveled to Washington, D.C. in hopes of renegotiating a new International Monetary Fund (IMF) deal, and such a deal could alleviate some pressure on the fragile international reserve position. Ultimately, though, a change in foreign exchange (FX) policy is needed to create stability.

Egypt (overweight): We believe Egypt’s external financing needs will be met with support from the IMF and the country’s partners in the Middle East. We see scope for Egypt to catch up to the broader move in high-yield debt and believe valuations are attractive.

Nigeria (underweight): Nigerian bonds have outperformed, and we have concerns about structural shortcomings in the country’s fiscal performance (notably, a high interest-rate burden and low revenue collection).

Bolivia (underweight): We are concerned about the longer-term trajectory of the country’s economy. Fiscal deficits remain too large given the fixed exchange rate, leading to what we believe are unsustainable debt dynamics.

Honduras (underweight): Although Honduras has the capacity to service its debt, fundamentals have been declining. The electricity sector has been particularly mismanaged, in our view, which has created fiscal challenges. The new government has threatened repudiation of the country’s debt obligations, which gives us some concerns about Honduras’s willingness to pay. Given valuations and the small chance of debt repudiation, we believe there is better value elsewhere.

Medium-Beta Bucket

In the medium-beta bucket, our largest overweight positions are in Cote d’Ivoire, Mexico, and Romania, and our largest underweight positions are in Oman, Jamaica, and Bahrain.

Cote d’Ivoire (overweight): Valuations in long-dated euro-denominated bonds are attractive, and we believe fundamentals remain relatively supportive.

Mexico (overweight): Our overweight is largely due to our position in the state-owned oil company, Pemex, which offers one of the largest spreads over its sovereign of any EM country, and we believe government support of the issue is likely.

Romania (overweight): We see a more positive fiscal trajectory, a more positive outlook for growth (now that interest-rate cuts are beginning to be priced in), and more attractive valuations relative to medium-beta peers. We also believe the potential for large-scale issuance has declined after Romania front-loaded the cycle by bringing both euro- and U.S.-dollar-denominated bonds to market in the first half of the year.

Oman and Bahrain (underweight): Our underweight is predominantly due to tight valuations and heavy positioning. Both countries have enjoyed a strong fiscal reform story over the past couple of years, but we believe this story is now fairly priced in. Meanwhile, both countries are still very dependent on oil, whose prices have been vulnerable to slowing global growth. In both countries, there is the potential for the positive reform momentum to stall if oil prices fall below the fiscal breakeven.

Jamaica (underweight): Jamaica has continued to implement an impressive fiscal-consolidation agenda, even following the pandemic. However, we believe market expectations and dollar prices for many Jamaican bonds are too high. In our opinion, there are more efficient ways to allocate capital in the EM universe.

Low-Beta Bucket

In the low-beta bucket, our largest overweight positions are in Guatemala, Bermuda, and Saudi Arabia, and our largest underweight positions are in United Arab Emirates (UAE), Uruguay, and Poland.

Guatemala (overweight): Guatemala has attractive valuations and strong macroeconomic conditions. Although electoral uncertainty weighs on the credit following the first-round elections in June, we believe institutions will remain resilient and bonds are attractively priced.

Bermuda (overweight): We favor its valuations and fundamentals relative to other low-beta sovereigns. Bermuda has similar valuations to Peru and Chile, but a stronger fundamental trajectory, in our view, as there is less institutional uncertainty in Bermuda.

Saudi Arabia (overweight): In the Gulf Cooperation Council (GCC) countries, we prefer Saudi Arabia to UAE, and reflecting this, hold a relative overweight spread duration position in Saudi Arabia. This overweight is driven by the more positive reform story in Saudi Arabia.

UAE (underweight): Bonds in weaker UAE credits, such as Sharjah and Dubai, have rallied to the point where we believe valuations are no longer attractive relative to fundamentals.

Uruguay (underweight): Valuations are unappealing. Fundamentals remain strong, but bond prices have compressed materially since the COVID-19 pandemic, and we believe this offers limited potential spread tightening.

Poland (underweight): We believe there is some value to be unlocked in Polish spreads, but await more clarity on the growth, issuance, and monetary policy outlook before investing capital here.

Potential Opportunities in Corporates

We also see select opportunities in EM corporate credit, where we believe a combination of differentiated fundamental drivers, favorable supply technical conditions, and attractive relative valuations to sovereign curves continue to provide ample investment opportunities.

Given near-term growth concerns and intermittent primary markets, we continue to focus on corporate issuers with low refinancing needs, robust balance sheets, and positive credit trajectories. With the peak of the U.S. interest-rate cycle within sight, we have also added some longer bonds, although availability and duration are lower than in sovereigns.

In terms of sectors, in Latin America, we are diversified across oil and gas; technology, media, and telecommunications (TMT); utilities; industrials; and financials. Our focus remains on Colombia, Brazil, Mexico, and Central America, but we have recently added corporates in Peru, Chile, and Panama.

In Central and Eastern Europe, the Middle East, and Africa (CEEMEA), we are diversified across financials; oil and gas; TMT; utilities; metals and mining; and real estate. Our country exposure is focused on UAE, Eastern Europe, and diversified African countries.

In Asia, we are diversified across oil and gas; financials; industrials; metals and mining; technology; utilities; and real estate (with positions in China, India, and Indonesia, predominantly).

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here