IBEX Limited (NASDAQ:IBEX) is a company that specializes in technology that bridges the gap between a business and its customers. The company offers customer service outsourcing, customer acquisition and survey analytics. Given the company’s historical modest growth, recession-proof revenues, and modest valuation, I believe the stock is worth a buy-rating.

The Company

IBEX’s offering has three solutions – ibex Connect, ibex Digital, and ibex CX:

IBEX’s Solutions (ibex.co)

Its offering helps companies with customer service with ibex Connect, customer acquisition with ibex Digital, and an all-around customer satisfaction and experience measurement system with ibex CX.

Looking at its offering, the company has products which have growing demand – the company presents that digital marketing, which ibex Digital represents, grows at a 10% annual rate according to eMarketer. CX and Customer feedback is expected to grow even faster at a 13% rate according to MarketsandMarkets. Ibex Connect is the company’s most stagnant solution, as it is only expected to grow at a four percent rate. This should support the company’s growth going forward.

IBEX serves multiple verticals, as told in the company’s May Investor Presentation:

IBEX’s Largest Verticals (Ibex May Management Presentation)

In addition, the company serves banking and travel verticals; revenues are diversified in terms of their source. As clients are often signed with multi-year agreements, IBEX’s revenues should be quite defensive as short-term weaknesses in the economy shouldn’t affect its revenues.

IBEX leverages countries with low average salaries for its customer support segment, ibex Connect – according to the company’s website, the company has around 30 thousand employees for customer management, with the company’s main sites being in countries like Pakistan, Philippines, and Jamaica.

On a qualitative side, I believe the company’s awards reflect a good standard in their offering – IBEX has released news of won awards such as Contact Center Technology Award by CUSTOMER Magazine, CRM Excellence Award by TMC, and was a finalist for 2023 CCW Excellence Awards.

Financials

IBEX has had modest growth in its recent years, as the company’s compounded growth from FY16 to FY22 has been around 7.3%. Growth has accelerated slightly in recent years, as FY2022’s growth was 11.2%. The company continues to sign new clients as it diversifies its revenues:

Ibex May Management Presentation

IBEX’s margins are scaling, as the current guidance has the company’s adjusted EBITDA margins at 17 percent. In terms of operating margins, the company currently has a trailing margin of 8.3 percent – a significant jump from 5.3 percent in FY2022. I believe these margins are sustainable for the company. This is supported by the company’s Q3/FY23 Earnings Call, where David Koning asks about IBEX’s margins’ sustainability. This question is answered by CEO Robert Dechant:

“I think [IBEX’s EBITDA margin] is sustainable and hopefully we can even improve upon that by continued selling in. We have the strong pipeline of clients that continue to go into our high-margin regions, with a lot of capacity available still that will drive strong margin flow through. And then, as I said, we’ve rationalized our U.S. footprint, some sizable capacity moved out that will be completed this quarter. So as we move into FY ’24, we really like the position we’re in.”

I expect the company’s margins to grow slightly but stagnate at around 9 percent.

In terms of the company’s balance sheet, IBEX doesn’t hold almost any interest-bearing debt apart from capital leases, that are operative in nature. IBEX holds around $43.7 million in cash, though, securing the company in case of weakened cash flows.

Valuation

At the time of writing the company’s stock is priced at $20.94, corresponding to a EV/EBIT ratio of around 9.6, a modest level in my opinion. With anticipated growth and further improved margins, this valuation seems attractive to me.

More than the EV/EBIT ratio, a Discounted cash flow analysis shows the stock’s cheap nature:

DCF Model (Author’s Calculation)

In the model, I expect the company to continue to grow very modestly in coming years, slightly below the company’s historical growth rates, and slowing down into a perpetual growth rate of two percent. This is coupled with slightly growing EBIT-margins – for FY23, I’m going with the company’s EBITDA guidance and turning it into related EBIT margins, and with the company’s operating margin growing by around 81 basis points in the following years. The company should convert its operating profit into cash flows quite well, as I believe their needs for capital expenditures isn’t too high.

The DCF model gives a fair value estimate of $37.16, around 77 percent above its current price. If the mentioned estimates come true, I believe the stock is quite severely undervalued.

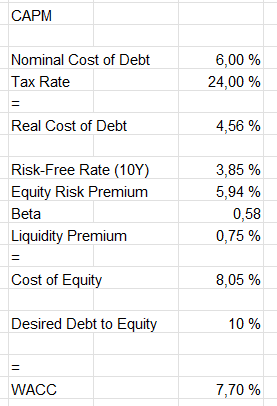

I used a weighted average cost of capital of 7.7% – a low rate for a stock. This is explained by the company’s defensive nature; IBEX’s solutions seem to be perceived as recession-proof, as Yahoo Finance has IBEX’s beta at 0.58. I constructed a capital asset pricing model of the company to illustrate the mentioned discount rate:

CAPM (Author’s Calculation)

IBEX doesn’t leverage debt to its advantage too well, so I’m expecting a debt-to-equity ratio of only ten percent with a cost of debt of six percent. On the cost of equity rate, I used the United States’ 10-year bond yield as the risk-free rate. For the equity risk premium, I use Professor Aswath Damodaran’s latest estimate. Finally, I add a 0.75% premium due to the stock’s sometimes limited liquidity.

Risks

The company could be posed with risks going forward. If the company can’t maintain a competitive offering, it could stop winning or even lose clients. This could be a significant risk for IBEX, as the company needs to maintain a good level of revenue to stay profitable.

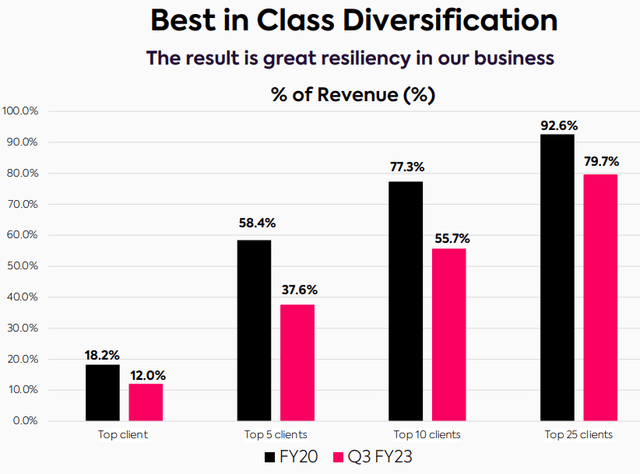

Churn relating to a large client would be a big risk. Although the company has diversified its revenues, IBEX’s largest client still represents around twelve percent of their revenue:

IBEX’s Clients (Ibex May Management Presentation)

This risk should continue to get smaller, as the company signs new clients, reducing the significance of single large clients.

Closing Remarks

I believe the company is currently cheaply valued if the company continues to grow near historical rates and expands or maintains its operating margin. With two of IBEX’s three solutions having a growing addressable market, the company should be in a good position to continue its growth. As long as the company’s fairly strong performance continues, I believe the company is worth a buy-rating at current levels.

Read the full article here