Stellus Capital Investment Corporation (NYSE:SCM) remains a strong business development company choice for passive income investors that are concerned with a recession descending on the U.S. economy in the near future.

The BDC has a first-lien focus and has the potential to raise its dividend, in my view, as the company has positioned itself to profit from rising interest rates.

Stellus Capital’s dividend coverage deteriorated in 1Q-23, but only because the BDC handed passive income investors a generous dividend raise. The BDC’s stock price has seen a slow and steady recovery since June, but the stock itself still remains undervalued, in my view.

First Lien Focus Provides Recession Protection

BDCs that focus primarily on first-lien debt have a competitive advantage over BDCs that focus more on second-lien debt, unsecured debt, or equity investments in order to spice up their investment returns, particularly in a recession environment when loan defaults are on the rise.

First liens are the highest-rated form of debt and loans are typically highly collateralized, giving the lender a high degree of certainty that the principal will be recovered in the event the borrower experiences financial difficulties.

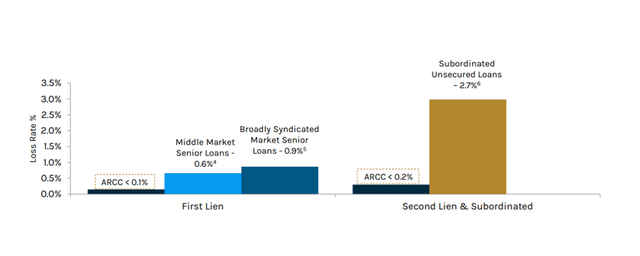

Based on information provided by the BDC Ares Capital (ARCC), middle market senior loans as well as syndicated market senior loans had loan loss rates of less than 1% while second liens and subordinated debt had much higher loan loss default rates of 2.7% (performance period 2007-2022). A concentration in first liens gives the BDC a competitive advantage over other BDCs that are more heavily concentrated in (higher risk) second liens.

Loan Loss Rates (Ares Capital Corp)

Stellus Capital primarily invests in private middle market companies that generate between $5 million and $60 million of annual EBITDA and many of those companies are backed by private equity companies. Typically, companies that seek debt capital from Stellus Capital do so because they need funds to finance their expansion, want to acquire another company, or do a recapitalization.

A high degree of implied recession protection is what I value the most about Stellus Capital, even though the BDC does not completely give up its equity upside.

The BDC’s total investment portfolio consists primarily of senior secured debt (92% of its debt was either first lien or second lien at the end of 1Q-23) and equity does not play an outsized role.

Stellus Capital had $60.5 million (7%) of its investment portfolio (a total of $877.5 million) invested in equity, which makes Stellus Capital a defensively-oriented BDC. I am also glad that unsecured debt, the riskiest form of debt, accounted for less than 1% of the company’s portfolio value (based on fair value).

Senior Secured Debt (Stellus Capital Investment Corporation)

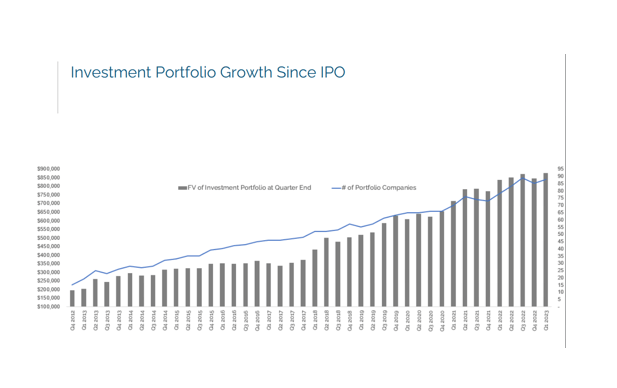

Stellus Capital’s portfolio, as of 31 March 2023, included 88 portfolio companies and the BDC has seen consistent and stable portfolio growth over the last decade. The BDC achieved its highest portfolio value ever in 1Q-23 and will probably report a new ‘portfolio high’ for the second quarter.

SCM was founded in 2012 and the company managed to do well for itself during the Covid-19 pandemic. Even during this recession, the BDC grew its overall portfolio value. As I said, the long-term growth history is favorable.

Investment Portfolio Growth Since IPO (Stellus Capital Investment Corporation)

NII Kicker And Potential For Improved Dividend Coverage

I am singling out Stellus Capital as a promising yield play in particular because the BDC has a large concentration in floating-rate debt, which I think will drive the BDC’s net interest income growth moving forward.

Though Stellus Capital also originates new loans, higher net interest income in a rising-rate environment is a potential NII kicker for Stellus Capital as well as a lower payout ratio.

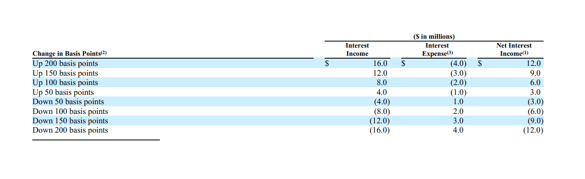

Approximately 97% of the BDC’s debt investments were made in floating-rate loans and were subjected to interest rate floors, at the end of the first quarter. This aggressive floating-rate exposure is set to drive Stellus Capital’s net interest income in a rising-rate environment. According to the company’s 10-Q report, a 100 basis point increase in key interest rates is set to add another $6 million in net interest income to the company’s bottom line.

Change In Basis Points (Stellus Capital Investment Corporation)

Risks Affecting The Investment Thesis

Cooling inflation and the central bank pulling back from rate hikes would be negatives for my investment thesis as higher potential net interest income is the main reason why I added to my position in Stellus Capital in the last month. A deterioration of the BDC’s portfolio quality would also be a negative development.

On the contrary, a strong hiring situation would support my argument for buying BDCs with aggressive floating-rate debt positioning. Though non-farm payrolls increased only 209,000 in June, which was below estimates, the labor market remained tight with an unemployment rate of 3.6%. This bodes well for additional rate hikes.

Stellus Capital’s Payout Ratio Deteriorated In 1Q-23 But Could Improve Moving Forward

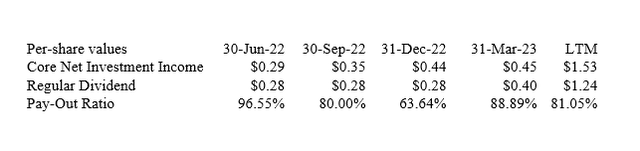

Stellus Capital has seen an increase in its dividend payout ratio in 2023 with the payout ratio jumping quite dramatically from 64% in 4Q-22 to 89% in 1Q-23.

The rise in the payout ratio, however, was primarily due to a massive increase in the regular dividend (which jumped from $0.28 per share to $0.40 per share) that realigned the BDC’s dividend with its underlying net investment income. With an LTM payout ratio of 81%, Stellus Capital also has potential to absorb a potential hit to net investment income, in my view, in case loan defaults rise.

Moving forward, Stellus Capital could experience higher net investment income if the central bank hikes interest rates in response to a strong hiring situation.

With unemployment being below 4%, the U.S. economy enjoys full employment. Further rate hikes should, therefore, result in higher net interest income as well as an improved dividend payout ratio which, in turn, could lead to another dividend raise.

Dividend (Author Created Table Using BDC Information)

Stellus Capital Is Attractively Valued

Stellus Capital’s net asset value was $13.87 per share at the end of 1Q-23 and with the stock trading at $14.33, the BDC’s valuation presently reflects a 7% premium to net asset value. The premium is neither large nor small, in my view, and other comparable BDCs sell at similar NAV multiples.

Taking into account the BDC’s aggressive positioning with respect to floating-rate loans, I think that SCM could eventually trade at a 10-15% premium to net asset value, implying a fair price range of $15.26-15.95 per share.

My Conclusion

Stellus Capital, in my opinion, not only offers an 11.2% yield but also upside potential. The realisation of the BDC’s net interest revenue potential in a rising-rate environment might close the value difference.

Stellus Capital also offers recession protection as its debt portfolio is defensively positioned in senior secured loans. Equity exposure remains small, which limits the risk of an investment going sour.

I would also note that the increase in Stellus Capital’s payout ratio in 1Q-23 did not reflect a change in NII prospects. Rather, the BDC realigned its dividend with its underlying growth in net investment income.

Read the full article here