Last month, management of Medical Properties Trust (NYSE:MPW) provided an investor update presentation that highlighted the case for the company’s stock price to be higher. While the company made several good points to justify an investment in their stock, the absence of certain cash flow information leads me to believe they will need to take on additional leverage to meet their current dividend obligations.

The presentation started by highlighting the discount in Medical Properties Trust stock value in relation to its peers. Historically, the company traded at a slight price to earnings and price to book discounts compared to its peers. Now, the stock is trading at less than half of the earnings multiple of its peers and at greater than 40% discount to book value (listed as net asset value).

Medical Properties Trust, June Investor Update

Management believes the share price is being driven down by a series of false narratives surrounding how the company acquires properties, the way it handles rents, and the financial condition of its tenants. Management effectively demonstrates how the company is unlocking the value of its assets through above market rents, partnership agreements, leasing agreements, and asset sales above their cost. Additionally, the company’s response to the financial conditions of its tenants does hold merit, as even bankruptcy does not mean tenant rents cannot be collected.

Medical Properties Trust, June Investor Update

Medical Properties Trust, June Investor Update

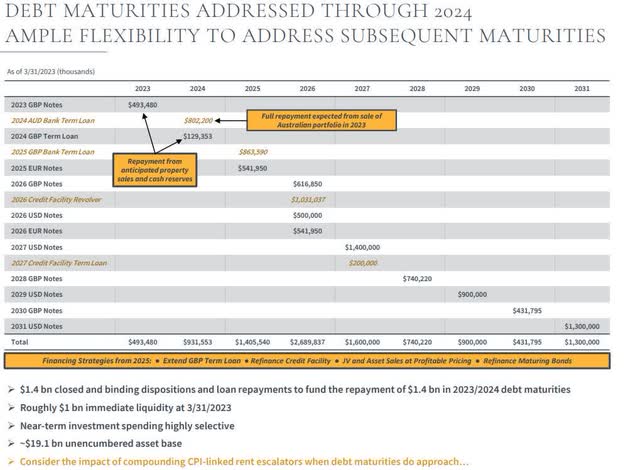

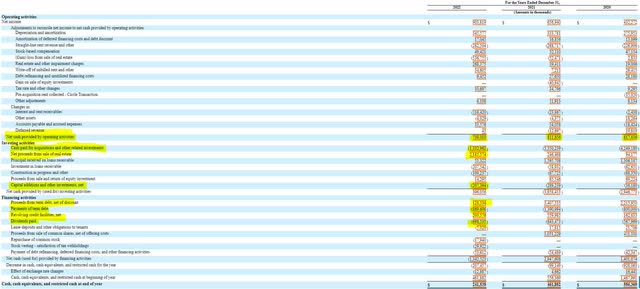

Where I begin to get concerned with the company’s outlook is when the presentation starts outlining the numbers. While Medical Properties Trust has its 2023 and 2024 debt maturities covered, it is utilizing cash on hand and asset sales to fund these maturities. This would lead the company to have less liquidity and a smaller balance sheet when it comes time to address the $1.4 billion in maturities coming due in 2025. These challenges come in light of the company having expended nearly all of its operating cash flow on dividends, leaving capital expenditures to be financed by asset sales.

Medical Properties Trust, June Investor Update

SEC 10-K for 2022

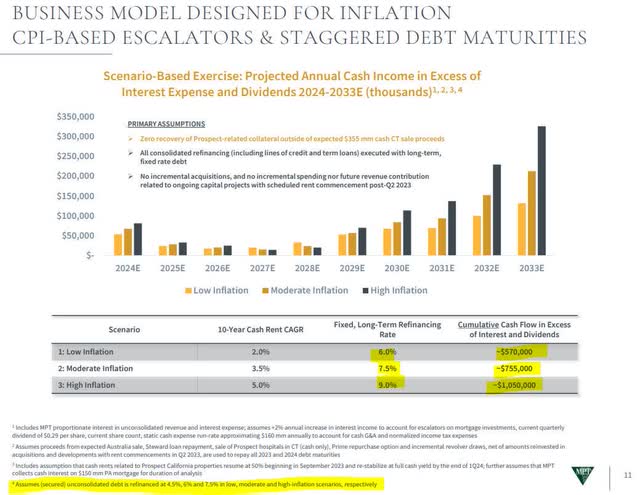

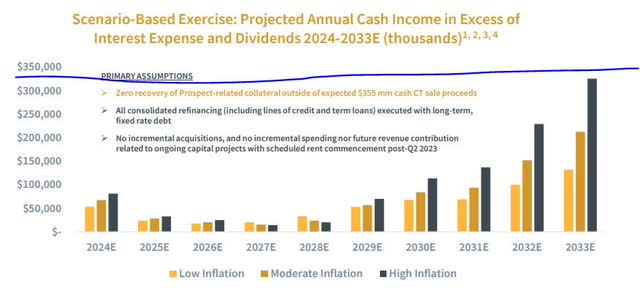

My concerns over the business magnify when examining the annual cash projections that management presented for the next 10 years. These projections were designed to assure investors that the organization was protected by high inflation, and consequently, higher interest rates. Medical Properties’ management is projecting earnings to decline notably from 2025 through 2028 and rebound into the next decade. My biggest problem with this projection is that while it includes dividend payments, it excludes capital expenditures.

Medical Properties Trust, June Investor Update

Based on the last two years of financial data, Medical Properties Trust has spent approximately $300 to $350 million per year towards capital expenditures. When that number is included in the management projections, a totally different picture appears. Based on the appearance of the amended chart, Medical Properties is going to conservatively need $250 million per year from 2024 to 2030 ($1.75 billion total) in funding to cover capital expenditures. Even under the high inflation assumption, 2033 results still come in slightly under capital expenditure need.

Medical Properties Trust, June Investor Update with CapEx Line Added

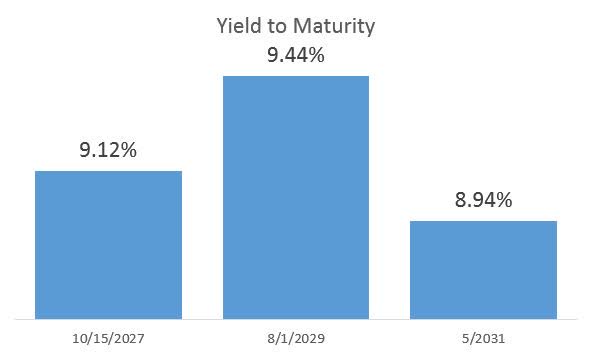

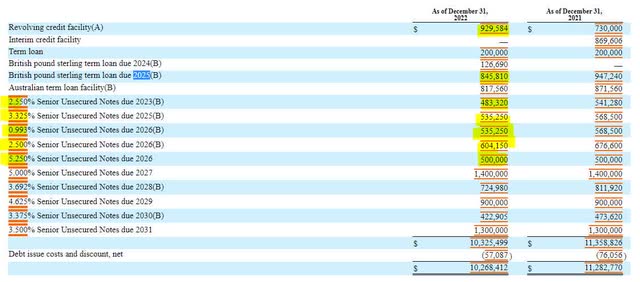

Another concern I have with the model is the debt refinancing assumptions. Management states that in their three scenarios, interest rates on refinanced debt are assumed to be 4.5%, 6%, and 7.5%, on secured debt and 6%, 7.5%, and 9% on unsecured debt. Unfortunately, we are in an environment of declining inflation and Medical Properties Trust debt is just now trading at around 9% after a recent rally. While it is possible for new debt to be financed at these levels, I would consider management projections to be slightly optimistic and in potential trouble if the company were to receive a credit downgrade.

FINRA data in Spreadsheet

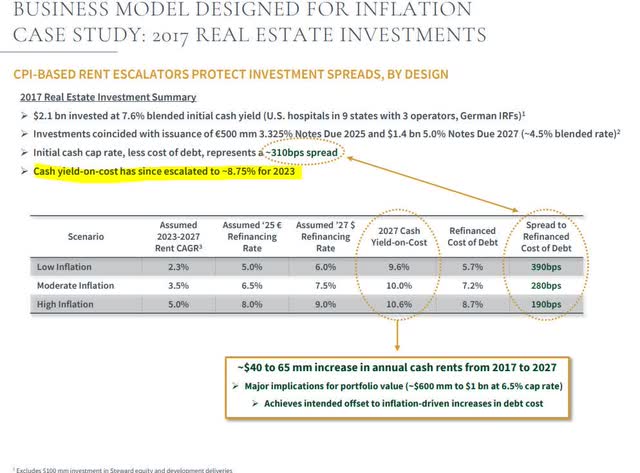

Another concern I have is regarding the return on invested capital or returns based on investment. Towards the end of their presentation, management presents the case that their capital investments have outperformed debt financing costs. They use assets acquired in 2017 to show how the returns outpaced projected refinancing costs by 190 to 390 basis points.

Medical Properties Trust, June Investor Update

The problem I have here is the study does not incorporate beyond one point in time. By looking at the cash flow statements dating back to 2018, I found that Medical Properties Trust has invested $14 billion (net of asset sales) into capital expenditures over the last five years. To achieve this, they borrowed $6.2 billion in long term debt and issued approximately $4 billion in shares. The result is an estimated $216 million increase in annual operating cash flow or 152 basis points of real estate investments.

TIKR

The problem is that Medical Properties has not generated enough cash to cover its dividends and capital expenditures combined. This will become problematic when low interest rate debt matures over the next four years, and be refinanced with higher interest rates that will erode cash flow generation. Management could issue new shares, but not with a cost of capital over 11.5% (current dividend yield). Reducing the dividend would increase the company’s options for raising cash while simultaneously decreasing the need for cash.

SEC 10-K for 2022

I’m still bullish on holding Medical Properties Trust debt as a good income investment. I believe that management will eventually find religion and adjust the dividend to more accurately reflect the current state of the business and the headwinds they are projecting for the second half of this decade.

Read the full article here