Elevator Pitch

My rating for Lear Corporation (NYSE:LEA) shares is a Buy. In my prior write-up for LEA published on January 3, 2023, I reviewed Lear Corporation’s recent M&A deals.

I focus on LEA’s updated FY 2023 financial guidance and takeaways from the company’s Seating Product Day in the current update. In the near term, Lear Corporation’s 2023 outlook has become much more favorable after the company updated its guidance for the current fiscal year. In the long run, LEA’s new innovative products, as outlined at its recent Seating Product Day, ensure that it is well-placed to beat its rivals and win new business. Therefore, I have upgraded my investment rating for Lear Corporation from a Hold to a Buy.

Updated 2023 Guidance

Lear Corporation has recently raised its expectations about the company’s fiscal 2023 financial performance, as indicated in a June 27, 2023 Seeking Alpha News article.

Specifically, the mid-point of LEA’s FY 2023 topline guidance was increased by +4.6% from $21.7 billion previously to $22.7 billion now. This implies that Lear Corporation currently expects its revenue growth to accelerate from +8.5% in FY 2022 to +8.7% in FY 2023 on a YoY basis.

Separately, Lear Corporation lifted the mid-point of its FY 2023 normalized net profit guidance by +13.6% from $590 million earlier to $670 million now. This points to an expected +28.2% YoY growth in LEA’s non-GAAP adjusted earnings for FY 2023, which is way better than the company’s FY 2022 normalized net income expansion of +8.9% YoY.

Notably, LEA’s actual Q1 2023 topline and bottom line had already beaten Wall Street’s consensus financial projections by +4.4% and +9.2%, respectively. At the company’s Seating Product Day on June 27, 2023, Lear Corporation stressed that “the strength of the first half really made an increase in the full year outlook a pretty easy decision”, taking into the fact that LEA is “on track for a strong second quarter.”

As such, Lear Corporation’s revised FY 2023 management guidance should give investors the confidence that the company will be able to deliver a better set of financial results for FY 2023 as compared to FY 2022 in my view.

Positive Takeaways From Seating Product Day

In the preceding section, I made reference to LEA’s management comments at the company’s recent investor event referred to as Seating Product Day. In its press release dated June 27, 2023, Lear Corporation mentioned that it “will update its long-term seating growth strategy and seating market share target for 2027” at the Seating Product Day.

I noted in my earlier January 3, 2023 article that “LEA’s target is to achieve a 28% market share in the worldwide auto seating industry in the next five years.” At the recent Seating Product Day, Lear Corporation revised its 2027 global automotive seating industry market share goal upwards from 28% to 29%. This is significant, as LEA estimates that a one percentage point of market share gain in the seating industry translates into incremental sales of around $700 million for the company.

Lear Corporation emphasized at the Seating Product Day on June 27, 2023 that the company’s “primary competitors have not matched our level of investment.” In contrast, LEA has continued to invest in technology, and this has paid off in the form of new products which give it an edge over its competitors. This is the key factor supporting LEA’s ability to grab market share away from its rivals.

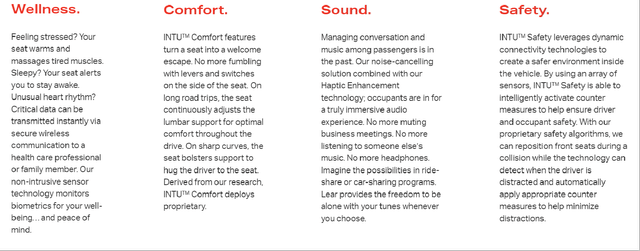

One example of a key new product is FlexAir, which LEA refers to a “urethane cushion alternative” that is 20% lighter and emits only half as much carbon dioxide emissions. Another example of Lear Corporation’s product differentiation is the company’s intelligent seating system branded as INTU. In its corporate presentation slides, LEA revealed that it was recently “awarded first-to-market contract to supply INTU products” for “an ultra-luxury European automaker”, which indicates that there is strong demand for INTU.

INTU’s Key Features

Lear’s Corporate Website

In my opinion, Lear has a very good chance of realizing its new 2027 Seating business market share target, as the company has innovative products that can boost its future sales at the expense of its rivals.

Closing Thoughts

LEA’s favorable short-term (FY 2023) and long-term (market share gains for Seating business) prospects don’t seem to have been fully priced into the stock’s valuations.

Lear Corporation is now valued by the market at 12.7 times (source: S&P Capital IQ) consensus forward next twelve months’ normalized P/E. In contrast, Lear Corporation has guided for a +28.2% growth in normalized earnings for FY 2023, while its consensus forward FY 2022-2026 adjusted EPS CAGR is +31.2% as per S&P Capital IQ.

Lear Corporation’s shares are trading at a low teens forward P/E multiple, and I deem LEA stock to be undervalued considering its bottom line growth outlook. This explains my decision to assign a Buy rating to Lear Corporation.

Read the full article here