Key takeaways

On January 18, 2022, we published the article “Vipshop: A Compelling Value Opportunity” on Seeking Alpha. We had a Strong Buy rating on the stock. We believed that the company was extremely undervalued when considering its durable franchise and many misguided controversies. Our valuation over the medium term (3-5 years) implied that the stock could be worth as high as $25.6, which was almost 3x the share price then $9.2.

We continue to like Vipshop (NYSE:VIPS) today. Based on our estimates, VIPS stock is >50% undervalued to its intrinsic value in the next 2-3 years. VIPS has been building its business moats, while the economic recovery in China will likely fuel double digit growth for VIPS in 2023. The company’s profitability has been very healthy, thanks to its cost discipline. Moreover, the idiosyncratic risks of delisting, VIE ban and tech regulations have either disappeared entirely or largely subsided.

VIPS has been buying back shares at an aggressive rate. In just 1 year between March 2022 and March 2023, the company bought back $1B worth of its own share, reducing its share count by almost 15%. More than a vote of confidence, the massive share buyback has increased existing shareholders’ ownership in the company by 15%, which helps improve shareholders’ returns.

In this follow-up article, we would like to evaluate the business progress the company has made in the last 1.5 years and update our views on the company’s valuation.

Original thesis

Our original thesis in January 2022 was that VIPS had a durable business franchise in its niche Ecommerce category: discounted apparel. This would help the company generate 5-10% revenue growth and 4-4.5% in the foreseeable future. In other words, we believed the revenue growth deceleration and margin compression at the time were temporary. Furthermore, our view was that the various concerns then (delisting, VIE and tech regulation) were overblown. We didn’t think they would affect the future prospect of VIPS, nor would they affect our ability to invest in the company.

What has transpired

After we wrote our thesis in January 2022, China went into a strict COVID lockdown which lasted until January 2023. This delayed VIPS’s revenue recovery trajectory, as the company saw its revenue decline 11.9% in 2022. It wasn’t until Q1 2023 that the company registered a positive YoY revenue growth of 9.1%. For Q2 2023, the company guided for an even higher revenue growth of 10-15% YoY. Interestingly, despite revenue declines throughout 2022, VIPS was able to expand its profit margin thanks to its cost discipline (primarily in marketing expenses).

Separately, delisting risk has been averted as China has provided the SEC/PCAOB with required disclosures. We have never doubted the integrity of China’s financial system. It was the fear of the unknown that caused investors to imagine the worst.

Moreover, the rumor on a VIE ban turned out to be false as well. At the time, we had quoted the China Securities Regulatory Commission (“CSRC”) which rebuked the VIE ban rumor. In fact, we saw that VIPS already had the option to list in Hong Kong Exchange, which had accepted the company’s VIE structure.

Lastly, tech regulations have largely subsided. Our argument then was that VIPS would be least affected by any anti-monopoly regulations. Its data is limited and less sensitive, so any personal privacy laws would be a wash as well.

What is next?

Beyond the fear of the unknown which investors have for China and its relationship with the US, what we believe the most important drivers for VIPS’s economics are its ability to defend its business moats. VIPS operates in a very competitive Ecommerce space, with existing 800-pound gorillas like Alibaba and JD, as well as fast growing newcomers like PDD and Shein. VIPS has identified its core competencies which are merchandising and customer service.

The company has made significant progress in merchandising, by strengthening its relationships with core brands. The strong brand relationships allow the company to secure higher quality and even exclusive merchandise. Management also recognizes that it needs to prioritize the core brands (roughly one thousand or so) instead of being all things to everyone.

On the customer side, similarly, VIPS is deepening its relationship with its core customers. The company has identified roughly 15M highest value customers from its 85M annual active customer base. The company has been able to sign up 6.3M of them to its Super VIP (“SVIP”) membership program. The SVIP membership has a subscription fee of RMB 199 per year. In return, the SVIP members receive higher discounts on core brands. They also gain exclusive access to special SVIP sales days on the 28th of every month. As shown below, SVIP membership and GMV share have been growing steadily.

|

SVIP membership growth (%) |

SVIP GMV share (%) |

|

|

2023-Q1 |

15% (6.3M) |

42% |

|

2022-Q4 |

13% |

42% |

|

2022-Q3 |

21% |

40% |

|

2022-Q2 |

21% |

38% |

|

2022-Q1 |

37% |

38% |

|

2021-Q4 |

50% |

36% |

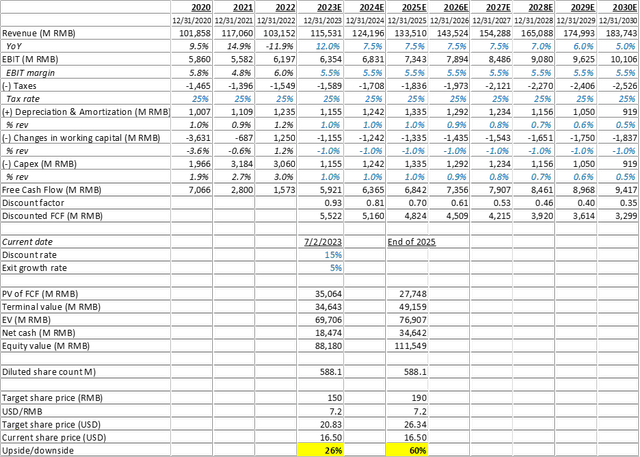

Updated valuation

We have refreshed our valuation model based on the latest financials. Based on a discount rate of 15%, we estimate that VIPS’s fair value share price is $20.8 today and $26.3 by the end of 2025. In other words, VIPS is relatively undervalued today, and should generate a 60% upside if we hold the share for 2.5 more years.

Our assumptions are:

- Revenue growth will be 7.5% in the medium term before reverting to 5.0% in perpetuity. The 5.0-7.5% growth is broadly in line with China’s nominal GDP growth in the future.

- EBIT margin will be 5.5% with net margin being 4.1%.

- Tax rate at 25%.

- Depreciation and CapEx will moderate and cancel each other as the company is now in its mature phase.

- Discount rate 15%, which is the discount rate required by XSTAR in all of our investments.

DCF Valuation by XSTAR Fund Management LLC (XSTAR Fund Management LLC)

Risks

We see several risks with VIPS as a business and as a stock.

As a business, VIPS operates in an intensely contested Ecommerce battleground. Given VIPS’s already established position in its niche market, we don’t think VIPS can outgrow the market. Therefore, in our valuation, we only assume a 5.0-7.5% revenue growth in the future. It is possible that fierce competition, especially in a low growth environment, may prevent VIPS from achieving our revenue growth rate of 5.0-7.5%.

As a stock, VIPS cannot escape the gravity of the “China discount,” which is driven by both a worsening US/China relation and the CCP’s control on its companies. The risk associated with the worsening US/China relation can be less capital invested in Chinese companies, thereby lowering their valuations. We don’t believe a ban on investing in Chinese companies will happen. However, if China and the US enter an outright war, potentially triggered by the Taiwan conflict, it is possible to see the US banning investing in Chinese companies – similar to what has happened with the Russian capital market.

Moreover, operating in China means that VIPS will need to play by the rules of the CCP, which demands a complete alignment with the CCP’s long-term visions for the country. We don’t think this is unreasonable. Here, we believe the fear of the unknown (of a different political and regulatory system) often makes investors imagine the worst, when in reality, the action and intention of the CCP may not be bad.

Conclusion

It is worth noting that VIPS has been buying back its share aggressively. The company completed its $1B share repurchase program announced in March 2022 in less than 1 year. Subsequently, it announced a new $1B share repurchase program ($500M announced on 3/30/2023 and $500M on 5/22/2023), which will be effective until March 2025. Between Q4 2021 and Q1 2023, VIPS’s share count has decreased by ~14%, generating significant upsides to its EPS growth and shareholders’ return.

We believe that despite recent rally, VIPS’s valuation is still very attractive, thanks to its durable franchise, cash flow generation and management’s share buyback action.

Read the full article here