Investment Thesis

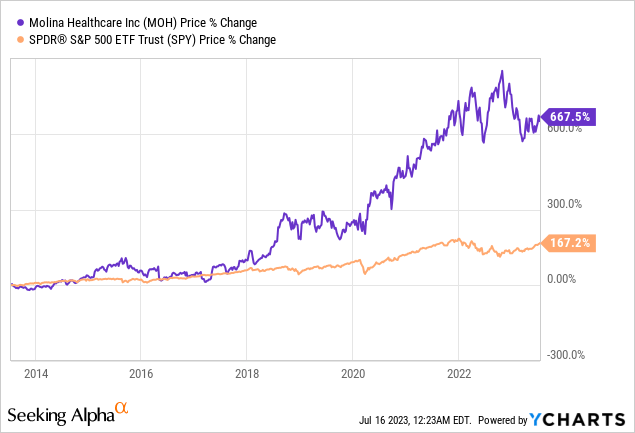

Molina Healthcare (NYSE:MOH) has been a hidden compounder in the past decade, with shares up nearly 670% during the period, vastly outperforming the S&P 500 Index (SPY) by a wide margin. The company operates in the massive Medicaid space, which continues to benefit from the aging population. The fragmented market also presents ample acquisition opportunities that further boost growth. These two catalysts and great cost control continue to help the company generate solid financials, as demonstrated in the previous earnings. With the valuation now headed back down, I believe the company presents a compelling investment opportunity.

Huge Market Opportunity

Molina Healthcare is a Fortune 500 managed healthcare company based in the US. The company provides health insurance plans and healthcare services to low-income individuals and families through government-sponsored programs such as Medicaid and Medicare. It currently operates across 20 states with over 5.1 million members, generating over $30 billion annually.

Medicaid, which accounts for 82% of total revenue, is a large and expanding market. According to the company, Medicaid spending should reach $443 billion in 2023 and is expected to grow at a solid long-term CAGR (compounded annual growth rate) of 8%. The number of Medicaid enrolments is also forecasted to grow from 79.3 million in 2023 to 82 million in 2027, as shown in the chart below by Statista. The growth is mostly driven by the aging population, which increases the need and usage of healthcare services. Considering the company’s current market share of just 6% and its limited geographical presence, it should continue to see significant expansion opportunities moving forward.

Statista

In order the accelerate its expansion, Molina Healthcare has also been actively pursuing different M&A (merger and acquisition) opportunities. Due to the fragmented nature of Medicaid and Medicare, there are currently over 300 companies in the market, which gives the company plenty of options to choose from. For instance, it has acquired 6 companies in the past 4 years alone. These acquisitions allow the company to quickly enter new markets and increase its presence. Given the large number of potential acquisition targets, I believe M&A will continue to play a huge role in the company’s future growth.

Joe Zubretsky, CEO, on acquisition opportunities

Our acquisition pipeline remains replete with actionable opportunities. While the timing of transactions remains inherently difficult to predict, the strength of our pipeline and our track record of success give us confidence in our ability to drive further growth from this important element of our growth strategy.

Medical Costs Concern

Many healthcare insurance companies have been under pressure in the past few weeks due to the concern about rising medical costs. For instance, many patients are now resuming their postponed surgeries or procedures, as hospital capacity finally eased amid lower COVID cases and better labor availability. However, the impact is largely overstated in my opinion.

As shown in UnitedHealth’s (UNH) earnings last week, the medical cost ratio was up, but only by 170 basis points from 81.5% to 83.2%, which is much better than feared. The impact should also be temporary and the cost should revert back to average after the delayed surgeries and procedures are being handled. Thanks to Molina Healthcare’s low-income demographic, it should also be relatively immune to this phenomenon, as its members tend to be more frugal.

Financials and Valuation

Molina Healthcare’s latest earnings were very solid, especially the bottom line. The company reported revenue of $8.15 billion, up 4% YoY (year over year) compared to $7.77 billion. The MCR (medical care ratio) was 87.1%, flat YoY thanks to outstanding cost management. The MCR for Medicaid and Medicare was 88.4% and 88% respectively. The MCR for Marketplace was 68.6%, largely attributed to favorable pricing and seasonal trends.

The bottom line was particularly strong amid flat MCR and improved operating leverage. For instance, G&A (general and administrative) expenses as a percentage of revenue declined 20 basis points from 7.4% to 7.2% This resulted in the operating income up 22.3% YoY from $372 million to $455 million. The operating margin expanded by 80% from 4.8% to 5.6%. The net income increased 24.4% from $258 million to $321 million. The diluted EPS was $5.52 compared to $4.39, up 25.7% YoY, as it benefited from a lower share count.

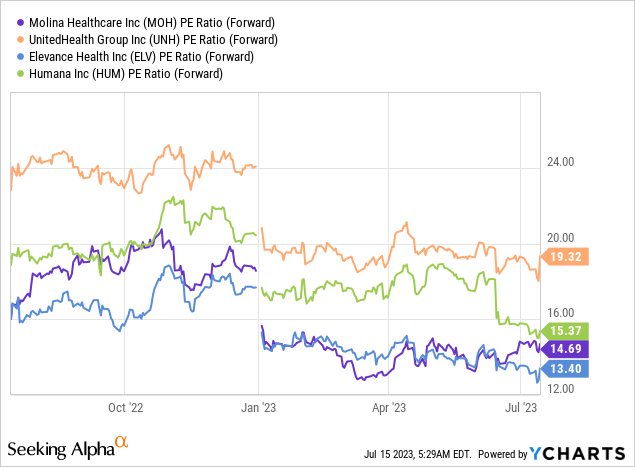

After the 20% decline in share price since last October, Molina Healthcare’s valuation is looking compelling once again. The company is currently trading at an fwd PE of 14.7x, which is lower than other major managed healthcare companies including UnitedHealth, Elevance Health (ELV), and Humana (HUM). As shown in the chart below, the peer group has an average fwd PE ratio of 16x, which represents a premium of 9%. The company is also cheap on a historical basis. For instance, the current multiple represents a discount of 10% compared to its 5-year average fwd PE ratio of 16.3x.

Risks

Regulation will always be a potential risk for Molina Healthcare. Due to the company’s heavy reliance on government-sponsored programs such as Medicaid and Medicare, any changes around the program will likely cause meaningful impacts. As the company continues to grow in size, acquisitions may also get much harder due to antitrust concerns. This is certainly something investors should be aware of as well.

Investor Takeaway

Molina Healthcare is a cheap and reliable compounder in my opinion. Medicaid is non-discretionary and the market is forecasted to continue its expansion as the population ages rapidly. Ongoing M&A is also another major catalyst that should further drive growth moving forward. As shown in the latest earnings, the company is doing an excellent job on cost control which continue to drive strong bottom-line growth. After the pullback, the valuation is now back to discounted territory, which should present solid upside potential. Therefore I rate Molina Healthcare as a buy at the current price.

Read the full article here