It’s no surprise that amid harsh macro conditions, struggling smaller companies have found it even more difficult to survive. Blue Apron (NYSE:APRN), in particular, has been in a massive upheaval over the past few years as the company has struggled with the tapering down of post-pandemic demand.

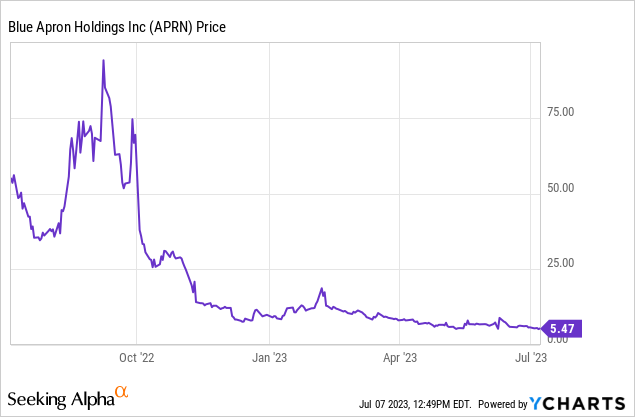

Year to date, the stock has sunk ~40% (severely underperforming most small-cap stocks that have rebounded as investors’ risk appetites have recovered) – though some hope was sparked over the past month as the company announced a major business transition.

Owing to the company’s latest strategic moves that have at least bought Blue Apron additional time, I am upgrading my view on the company to neutral (from a prior bearish outlook). I’m still jittery on the stock as a big investment, but neither do I think the stock will collapse at year-end, especially if it can start to make progress with its capital-light business model and generate adjusted EBITDA next year.

In this article, I’ll cover Blue Apron’s major business transition as well as the harsh realities still surrounding the company (orders and revenue are still declining, which is unlikely to change anytime soon), but my bottom line take is this: Blue Apron may be worth some short-term trades for quick gains, but given the massive uncertainty especially around demand trends for the company’s meal kits, this is a position you’ll have to monitor closely and not hold onto for too long.

Assets sold to FreshRealm

First, let’s center in on where Blue Apron was as of its last reported quarter (Q1, the March quarter which Blue Apron released in May).

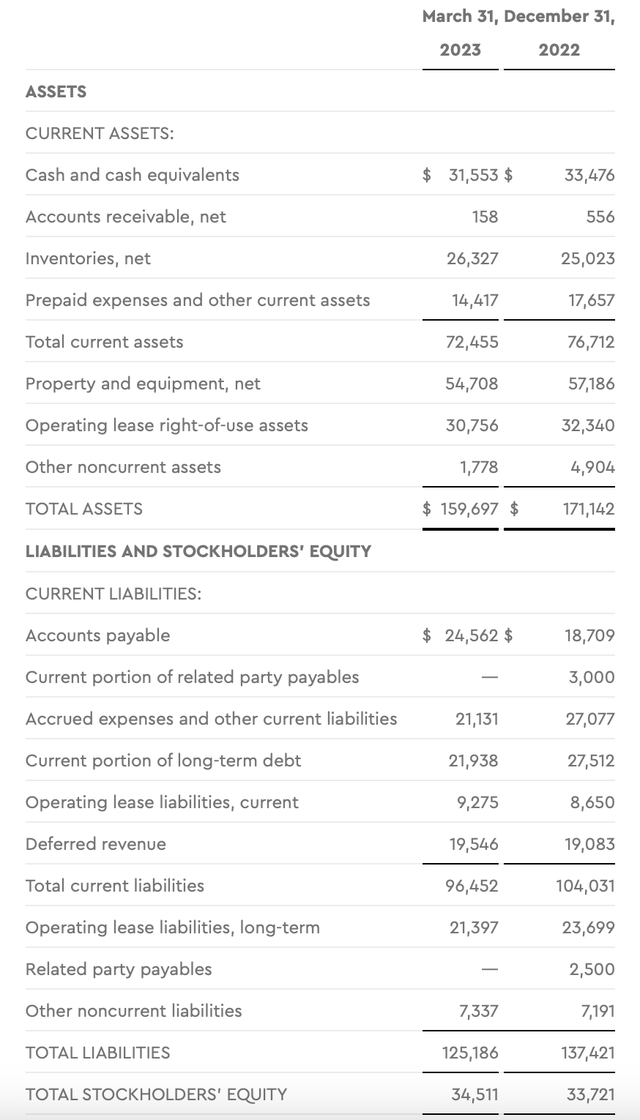

The balance sheet is the first place to start with a company in Blue Apron’s dire straits. As of March, the company had only $31.5 million of cash left, alongside $21.9 million of debt: which, needless to say, isn’t much for a company whose Q1 adjusted EBITDA and free cash flow were -$8.7 million and -$10.8 million, respectively.

Blue Apron Q1 balance sheet (Blue Apron Q1 earnings release)

For investors who are newer to this stock, the core of Blue Apron’s issue (which we’ll cover in the next section, and which will be largely unchanged by the company’s business model shift) is declining order rates and loss of economies of scale which have hurt the company’s gross margins.

In June, however, the company decided to sell all of its fulfillment centers, equipment, and related personnel teams to a company called FreshRealm, another meal-kit competitor. The deal, worth $50 million all-in, included the following consideration:

- $25 million upfront cash

- $3.5 million in the form of a note payable

- $4 million in contingent cash, subject to Blue Apron hitting certain financial and operational milestones

- $17.5 million in rebates for FreshRealm’s production

The company used the upfront cash payment to extinguish its debt, eliminating its interest payments and clearing up its balance sheet to avoid a near-term cash shortfall.

In a press release announcing the move, Blue Apron wrote:

Blue Apron is now an asset-light company, focused on the growth of its direct-to-consumer business. The Company plans to continue to build its strong brand and deliver the high-quality products its customers have come to love. In addition, Blue Apron expects to accelerate the expansion of its product offerings, including the addition of new convenient options.”

FreshRealm is now the exclusive supplier of meal kits to Blue Apron, and Blue Apron now intends to focus solely on brand management and customer acquisition, leaving the production operations to FreshRealm.

My take here: by eliminating in-house production, Blue Apron removes the burden of its flailing gross margins and will enable a path to profitability more quickly. At the same time, however, if Blue Apron does “take off” and become popular again, sacrificing production to a third party (which presumably makes a margin off Blue Apron’s orders) reduces Blue Apron’s ability to generate eventual economies of scale. Regardless, however, this was the right short-term move for Blue Apron to prevent bankruptcy.

Will customers return?

Ultimately, from a customer angle, this is a behind-the-scenes transaction that doesn’t impact the customer experience. Blue Apron’s core issue still remains: can it revive interest in its meal kits?

Certainly, the company doesn’t have price on its side. Even the highest-volume of its meal plans are priced at $8/serving plus shipping, and the company has historically relied heavily on introductory promos to bring new customers in (who eventually churn when they have to pay full price). In the current macro environment, asking consumers to pay $8 for a home-cooked meal may alienate certain buyers.

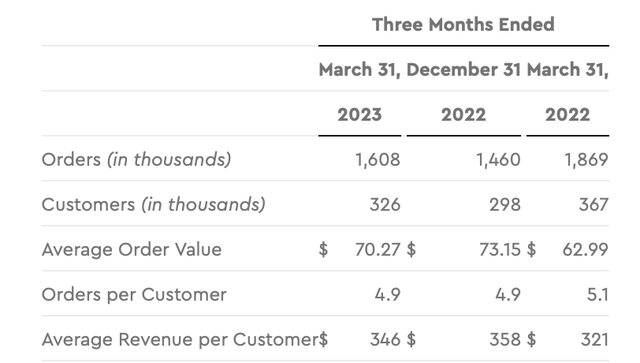

Orders in the March quarter fell -19% y/y to 1.61 million, while customer counts also declined by ~31k year over year. Order frequency per customer is also down.

Blue Apron Q1 customer metrics (Blue Apron Q1 earnings release)

The “bright side” of this coin is that by removing concerns about production, Blue Apron can focus its financial and human resources on customer acquisition and marketing to revive demand trends. It’s also plausible to think that the dozens of other meal-kit competitors (many of whom are private) are undergoing similar issues as Blue Apron, and those who are unable to strike deals like Blue Apron did to eliminate liquidity woes and centralize production will eventually fold – driving more demand toward Blue Apron.

Blue Apron has stated a target of generating positive adjusted EBITDA by Q2 of FY24 (a year ahead from now). This will be predicated, of course, on the company’s ability to grow its customer base.

Key takeaways

In my view, Blue Apron has cured its most immediate-term concern: the liquidity crunch that would have put a halt on the company’s business at year-end. Outsourcing production to FreshRealm and converting its fixed assets to cash will help the company centralize its resources on growing its brand – but there’s a huge execution risk here too. If Blue Apron sinks its limited cash into a big marketing push that fails, the company will still exhaust the lifeline it has set up.

All in all, maintain caution here, but in my view, there is no longer an immediate de-listing risk for this stock anymore.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here