Siemens Healthineers (OTCPK:SMMNY), a global medical technology (‘MedTech’) leader in the imaging and diagnostics markets, has seen a rather mixed fundamental performance over the last quarter. Top-line growth (adjusted for COVID-19 antigen tests) was stronger than expected, along with overall order intake. In contrast, earnings (ex-COVID) fell short of expectations due to headwinds in diagnostics and concerning impairments at Corindus.

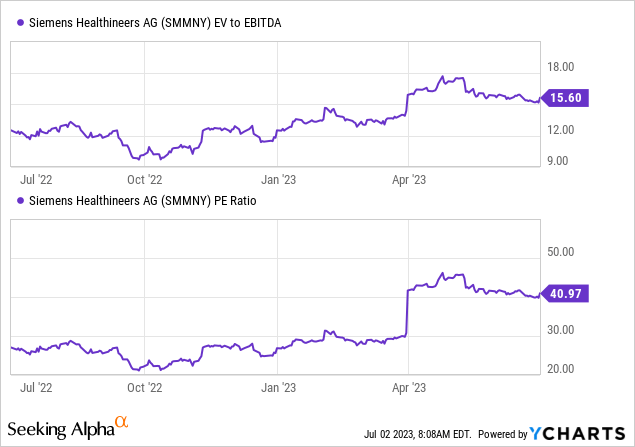

With management reaffirming its FY23 targets, however, the bar is high and could be prone to downward revisions should the company fail to deliver on organic sales and EPS outgrowth vs. its European MedTech peers. The stock isn’t cheap either at >40x P/E (>25x fwd) vs. a mid-teens % near-term organic earnings growth path – in stark contrast to the discounted valuation when I last covered the stock. In the likely case that the market is embedding some M&A growth premium here, I would be cautious. Management’s capital allocation track record has been mixed, with another round of goodwill write-downs last quarter for robotic-assisted MedTech platform Corindus (vs. initial expectations for EPS accretion this year) being a case in point. Net, I would remain sidelined here pending a meaningful valuation reset.

Ex-COVID Growth Strong in H1 but Softening Order Book Warrants Caution

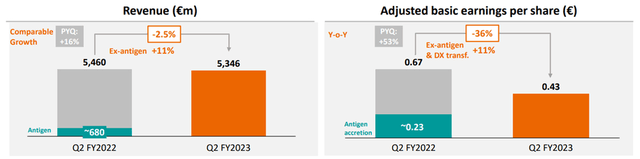

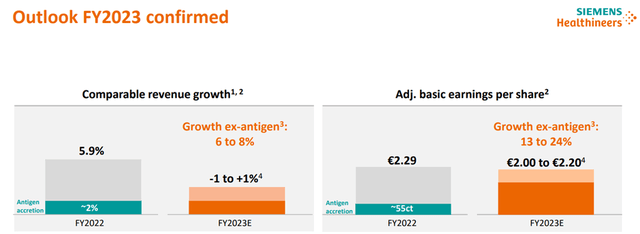

A quick glance at the headline results from Siemens Healthineers would paint a bleak picture – revenue was down ~2.5% YoY to EUR5.3bn, while on an organic basis, headline growth was still underwhelming at +2.5% YoY. But normalizing for the COVID base effect (i.e., antigen tests which are now down to near-zero), organic growth would have been an impressive +11% YoY on strong equipment sales and service growth. Radiation oncology acquisition Varian was another bright spot, as easing supply chain bottlenecks allowed it to address the pent-up backlog. At the group level, management has reiterated its comparable revenue growth guidance for the full year at -1% to 1% YoY. The most significant acceleration is expected from Varian, where a low teens % growth algorithm is likely on the cards post-resolution of supply chain issues.

Siemens Healthineers

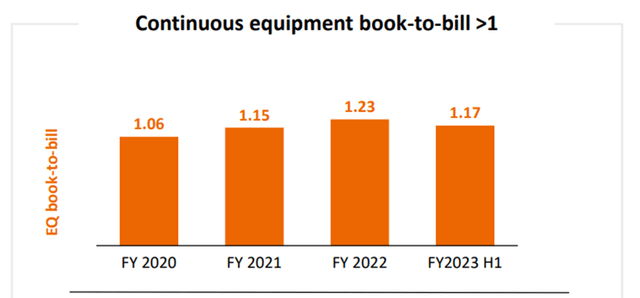

More concerning is the softening order book – following flattish order growth in its latest fiscal quarter, the company disclosed a low to mid-teens % decline in order intake. In tandem, overall book-to-bill is down to 1.0x (vs. 1.4x previously), with guidance calling for a flat equipment book-to-bill ratio of 1.1x for H2 (vs. 1.17 equipment book-to-bill in H1). The equipment book-to-bill has still outperformed peers like Koninklijke Philips N.V. (PHG) and GE HealthCare (GEHC), though, which is commendable. The breadth of its product portfolio and innovation has been key, and as management stressed, it retains an advantage in critical areas like imaging (e.g., photon-counting computed tomography). Still, it’s important to note that recurring revenues now make up >50% of the business; so while weaker order flow is a factor for forward revenues, the company should still make its top-line guidance numbers.

Siemens Healthineers

Earnings Guidance Intact Despite Below-Par Profitability

As resilient as the top-line results were, earnings weren’t quite as great. The headwind from the COVID-19 business was significant, as expected, though the key surprise was the higher diagnostic transformation costs at EUR77m (over double the EUR34m FQ1 base). Yet, management has somewhat optimistically kept the adj EPS guidance intact at EUR2.00-2.20/share (vs. EUR2.29/share in FY22). As this still embeds EUR100-EUR 150m of transformation costs related to the Diagnostics business (vs. the >EUR100m already incurred), there isn’t a huge amount of margin for error here.

And with a good deal of the implied margin improvement now pushed to the back end of the fiscal year, downward revisions to the margin trajectory could well be on the cards in the coming months. Beyond volumes, lower freight costs and pricing trends (vs. the improvements already realized in the order book) will also be worth keeping an eye on to gauge where EPS eventually lands.

Siemens Healthineers

Poor Capital Allocation Decisions are Starting to Bite

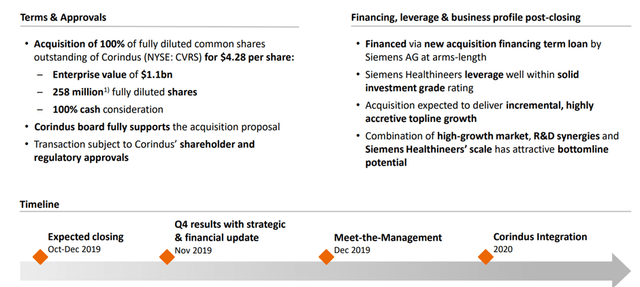

Having completed the acquisition of Varian recently, management has rightly focused its near-term priorities on integration. While management has indicated limited M&A appetite for now, recent reporting of Siemens Healthineers considering a bid for Medtronic’s patient-monitoring and respiratory-intervention businesses means opportunistic deals may still be on the table. Further acquisitions won’t be well-received by investors, in my view, given the underperformance of the robotic-assisted technology platform Corindus post-deal.

Siemens Healthineers

Relative to expectations for EPS accretion in FY23 (based on optimistic assumptions about the adoption of robotics in a broad range of procedures), performance has fallen well short, driving dilution to advanced therapies segment margins. The latest Corindus pivot to solely neurovascular interventions is likely staving off a full impairment of the $1.1bn price tag, though further disappointments risk more markdowns to the ~EUR18bn goodwill balance.

Siemens Healthineers

Still an Interesting MedTech Name but Now at a Premium

Coming off a mixed quarterly report which saw resilient order intake but below-par profitability, Siemens Healthineers retained its forward guidance for the year. While I like the company’s product portfolio and its ability to outgrow its EU MedTech peers over the mid-term, the valuation isn’t cheap any longer at a premium >25x fwd PE. Hence, continued share gains in imaging and a high-single-digits % growth boost from Varian probably won’t be enough to meet market expectations. Against the optimism, the company’s order book hasn’t impressed, while fundamental challenges in Advanced Therapies (note the continuous Corindus impairments in recent years) and Diagnostics threaten to de-rate the stock. This could push management into more M&A (note the recent chatter regarding a Medtronic acquisition), which won’t be well-received by investors given the bloated goodwill balance and heightened risk of further impairments down the line.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here