Overview

Amadeus IT Group (OTCPK:AMADF) is one of the leading suppliers of IT solutions to the airline industry, providing airlines with access to one of the world’s largest global distribution systems [GDS] and offering a range of software solutions to the airline industry.

Previously, I discussed my beliefs that AMADF is a promising long for those looking for exposure to the airline industry and the technology services that support it. Despite the mature nature of the global distribution systems industry, AMADF has room for expansion through cross-selling and new customer acquisition. In addition, its hospitality business is also a promising area of growth.

Just as I expected, the business continues to do well in Air Information Technology [IT] which I continue to see compelling medium-term structural air travel growth tailwinds. Even though volume was slightly weak, AMADF has maintained its pricing power in the Distribution sector by capitalizing on the product’s stickiness. Although the bear case will continue to focus on the bookings recovery trajectory in Distribution, I believe that Air IT’s continued strong performance, with revenues now above pre-COVID levels, will become the main bulk of the AMADF thesis going forward. Finally, management has resumed its share buyback program, which is consistent with my expectation and further supports my view that business is thriving and has resumed its cash-generating mode. I reiterate my buy rating.

Travel recovery

In my opinion, AMADF has not yet reaped the full benefits of the uptick in air travel demand. Although the global air traffic recovery trend is continuing as expected, it is now dominated by domestic short-haul flights as consumers switch to low-cost carriers (LCCs) that rely less on the GDS channel (such as AMADF). Additionally, AMADF does not directly benefit from the recent months’ significant recovery of air traffic because it does not include domestic China traffic in its portfolio. However, this means that AMADF will grow at a faster rate when the economy improves, as the recovery of long-haul flights will necessitate a greater reliance on GDS. The resumption of trans-Asian transportation links to and from China is good news for AMADF as well. This is significant for AMADF because the it has a large position in Asia as the preeminent distributor and provider of Passenger Service Systems.

Share buyback program

AMADF has officially announced the start of its share repurchase program. The maximum buyback under the program is €433.3 million, or about 1.3% of the company’s current market cap. Although this buyback will improve returns slightly, the fact that management is confident enough to return capital is the more important takeaway. Which is a reflection of the robustness of underlying demand. Given its ability to lever up its balance sheet (see my previous post for details), I anticipate AMADF will eventually return to its historical share buyback profile.

Hard to decide if AI is good or bad today

It is currently difficult to determine whether AI poses a risk to AMADF. As there are multiple perspectives on this that are difficult to validate, I believe it is best to remain neutral on generative AI until we see more evidence of how things play out. The negative narrative is that it will lead to consolidation among travel agencies because the larger player will be able to use AI to further scale the business (larger player has more data and marketing power, for example). The subscale player, on the other hand, will simply be swallowed by a larger player because they lack the necessary scale to acquire inventory and distribute it. As a result, a larger travel agency customer would have more bargaining power when it came to incentive fees. This could be a major issue, but I’m not sure how much negotiating power the travel agents will have because the front desk staff is already well-trained to use AMADF. It will also be difficult for them to rip out and replace with another system, as AMADF is aware.

There is also the possibility that large tech players with advanced AI will enter the GDS space. This is possible, but the value of GDS lies in the live connections to airline inventory, not in search. As a result, the big tech companies will still have to use AMADF data, for which AMADF can charge a fee. Furthermore, training the models must be based on travel data, and the GDS is the industry’s universal data aggregator.

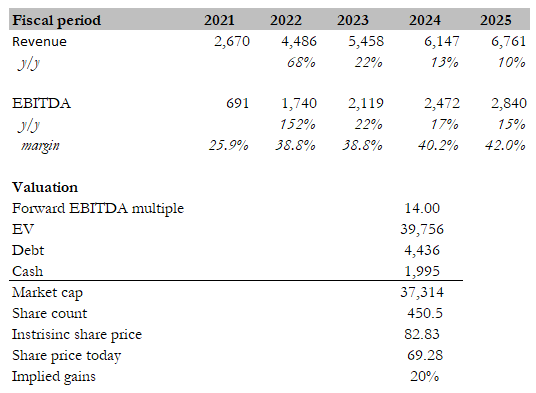

Valuation

I modelled AMADF to grow at an elevated pace in FY23 and FY24 as it experiences the full recovery of long-haul and Asia flights, and growth to return to historical high single digits – low-teens growth. This will be accompanied by margin expansion as AMADF continues to raise prices (high margins) and see higher mix from Air IT services. Given AMADF scale and potential for elevated growth, I believe it deserves to trade at a premium to Sabre Corp (SABR) which is trading at 12x EBITDA today.

Own model

Risks

Firstly, the potential impact of worse-than-expected macro conditions poses a risk to the company’s overall outlook. Economic factors such as inflation, interest rates, and global market volatility can significantly influence business operations and consumer behavior, thereby affecting the company’s financial performance.

Secondly, another key risk lies in the slower recovery of air travel following the COVID-19 pandemic. As the company operates in an industry closely tied to air travel, any delays or setbacks in the recovery of this sector could have adverse effects on its revenue and profitability. Factors like prolonged travel restrictions, reduced consumer confidence, or the emergence of new variants can hinder the resumption of air travel to pre-pandemic levels, potentially prolonging the company’s recovery timeline.

Conclusion

I expect AMADF to continue riding the wave of travel recovery. Despite the current dominance of domestic short-haul flights and the exclusion of domestic China traffic from its portfolio, AMADF’s strong performance in the Air IT sector, with revenues surpassing pre-COVID levels, remains a compelling factor. The company’s share buyback program and its ability to leverage its balance sheet indicate confidence in its underlying demand. While the impact of AI on AMADF is uncertain, it is important to remain neutral until more evidence emerges.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here