Businesses update

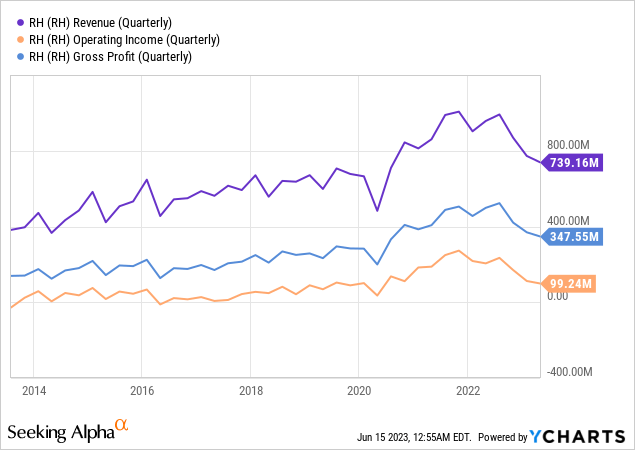

RH’s (NYSE:RH) most recent financial results for 2023 Q1 exceeded their own expectations, with revenues reaching $739 million and an adjusted operating margin of 14.9%. This outperformance is not bad considering the challenging macroeconomic conditions, such as high 30-year mortgage rates, ongoing economic tightening, and uncertainty stemming from the regional banking crisis. It is evident that RH has moved past the extraordinary tailwinds brought about by the pandemic. The remarkable margins and growth rates witnessed in 2021 and early 2022 are no longer sustainable in my view, and both the scope and profitability of the business are currently declining without any signs of an immediate rebound.

The chart below clearly illustrates a significant pullback in RH’s revenue, bringing it back to levels seen in early 2020. Additionally, the operating income has dropped nearly to pre-pandemic levels. This decline in profitability has had a negative impact on the return on invested capital and has potentially eroded shareholder confidence. Despite RH’s expansion and increased asset base during the pandemic, the company failed to generate continuously higher revenues and profits.

RH Remains Committed to Its Investment Strategy Despite Challenges

Amid a challenging luxury housing market and economic conditions in 2023 and beyond, RH’s CEO Gary Friedman seems to embrace a contrarian stance to his business. In the conference call, he said:

it’s times like these that businesses tend to move in herds, pursuing broadly adopted short-term strategies that lead to mostly similar outcomes. It’s also times like these that present opportunities to pursue long-term strategies that can create strategic separation and significant value creation for those teams willing to take the road less traveled and pursue their own unique path.

In a time of cost-cutting and business slowdown, RH stands out with its unwavering commitment to investment. The company seems determined to accelerate the expansion of its product portfolio, with plans to release a record-breaking collection of 70 new furniture and upholstery products. Additionally, RH has recently opened a stunning new gallery at the historic Aynho Park, UK, with three restaurants. RH has set its sights on opening locations in Brussels, Dusseldorf, Munich, and Madrid, along with an Interior Design Studio in London within the next 18 months. Moreover, RH plans to extend its presence to Paris, London, Milan, and Sydney by 2024 and 2025. Domestically, the company has identified 40 smaller markets where it aims to build design studios catering to the needs of affluent clientele. I believe RH’s bold investment strategy demonstrates its confidence in the future and its determination to provide exceptional experiences to customers worldwide, in my view.

All these projects need money and investments. RH chose to take advantage of the $2.5B of long-term debt they raised before the market tightened. From January 2022 to this quarter, RH decreased cash by around $600m while net property, plant & equipment increased by around $400m. RH remains committed to its strategy, aiming to gain market shares and strengthen its position. These investments, supported by strategic financing, position RH for growth and success in the industry in my belief.

RH is a very special brand with a great reputation

RH focuses on catering to the exclusive needs of the wealthy 1% who prioritize quality and individuality over cost. They have created an ecosystem that enhances the value of their products appear to resonate with this elite customer base. RH aims to cultivate an image of being the tastemaker in the realm of interior design. Their unique approach involves offering immersive experiences through their numerous galleries and showrooms. By integrating hospitality services like restaurants and wine bars into their retail locations, customers can fully immerse themselves in the concept of their product designs. In addition, RH provides additional touchpoints for affluent customers through their guesthouses, private jet services, and luxury yacht offerings.

What sets RH apart is this immersive approach to brand elevation. Unlike traditional companies, RH is truly product-oriented and does not have a dedicated marketing department. Instead, they rely on their products to speak for themselves and surprise consumers with their thoughtful design philosophy. If the quality of RH’s products is exceptional, positive word-of-mouth marketing naturally follows. RH has demonstrated its prowess in intriguing the general populace with its successful designs such as the cloud couch, as well as its unique hospitality offerings, including the RH restaurants. As time goes on, I think RH’s brand image will strengthen, leading to increased profitability in the long term.

Bottom Line

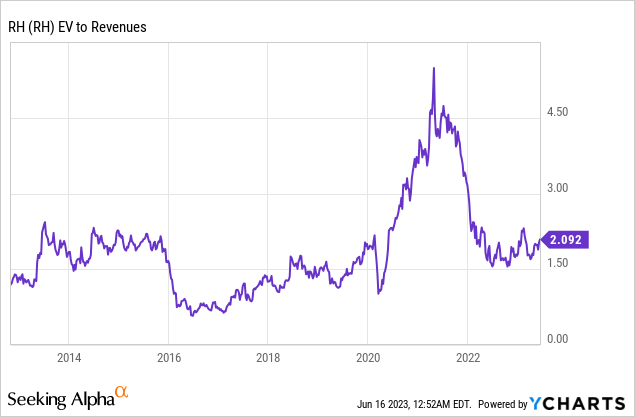

The outlook for RH in the coming quarters may present some challenges, as the company has provided guidance of $3 to $3.1 billion in revenue, representing a 15% year-over-year decline, and an operational margin of 14.5% to 15.5%, compared to 20% in 2022. Despite this, RH is expected to maintain profitability and there is no immediate risk of bankruptcy. The current EV/Sales ratio of 2.72x is within the historical range seen between 2014 and 2016, as well as pre-pandemic levels. In comparison, competitor Arhaus has a lower EV/Sales ratio of 1.21x. However, RH generates significantly more operating cash flow, approximately 9 times that of Arhaus. Overall, I believe RH is fairly valued and worth monitoring as the company continues to introduce new developments in both the hospitality and global expansion sectors. The performance of these investments remains uncertain, but could have a significant impact on the stock’s future.

It is true that Warren Buffett’s Berkshire Hathaway (BRK.A) (BRK.B) no longer owns RH, and there could be various reasons for that decision. One possible reason could be the concern over RH’s ability to defend its margins, as the luxury furniture business can be cyclical in nature. The assumption that the wealthy will always demand luxury furniture has been challenged, particularly during the year 2022. In fact, RH’s revenue and profitability decline has been higher than the overall market. Additionally, RH’s long-term debt has increased from $579 million in 2021 to the current $2.5 billion, which has had an impact on the company’s return on invested capital and could be a cause for concern.

Overall, I still believe in the positive outlook on RH’s long-term prospects as a consumer-facing business in the vast housing and furniture market. I believe the company’s unique business model and a clear focus on executing CEO Gary Friedman’s vision provide the potential for significant growth.

Read the full article here