DuPont de Nemours (NYSE:DD) would be an excellent addition to a long-term portfolio with its diverse revenue streams from numerous end markets and a growing healthcare business. But the shares are overvalued, and the dividend yield is low. Investors may have to wait for the stock to drop below $60 before buying. At closer to $57, the stock would yield 2.5%.

Weak demand in electronics puts pressure on revenue and EBITDA

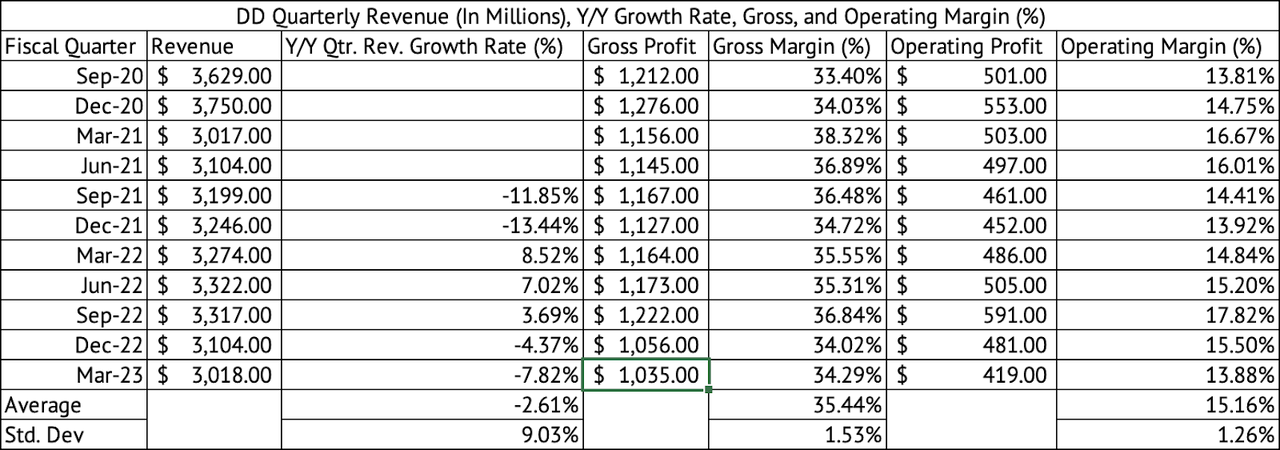

In Q1 2023, the company saw its sales decrease by 7.8% y/y, but organic sales were only down by 3% (Exhibit 1). The revenue declined by 3% due to a strong dollar, and portfolio divestitures accounted for a 2% drop in revenue. Volumes were down 7% y/y, which impacted revenue and reduced EBITDA.

Exhibit 1:

DuPont Quarterly Revenue, Gross, Operating Profit, and Margins (%) (Seeking Alpha, Author Compilation)

In Q2 2023, the company expects continued pressure on revenue due to slower consumer demand and inventory destocking in the electronics sector. The company expects continued strength in its water, auto adhesives, and industrial markets, including healthcare.

Stretched valuation

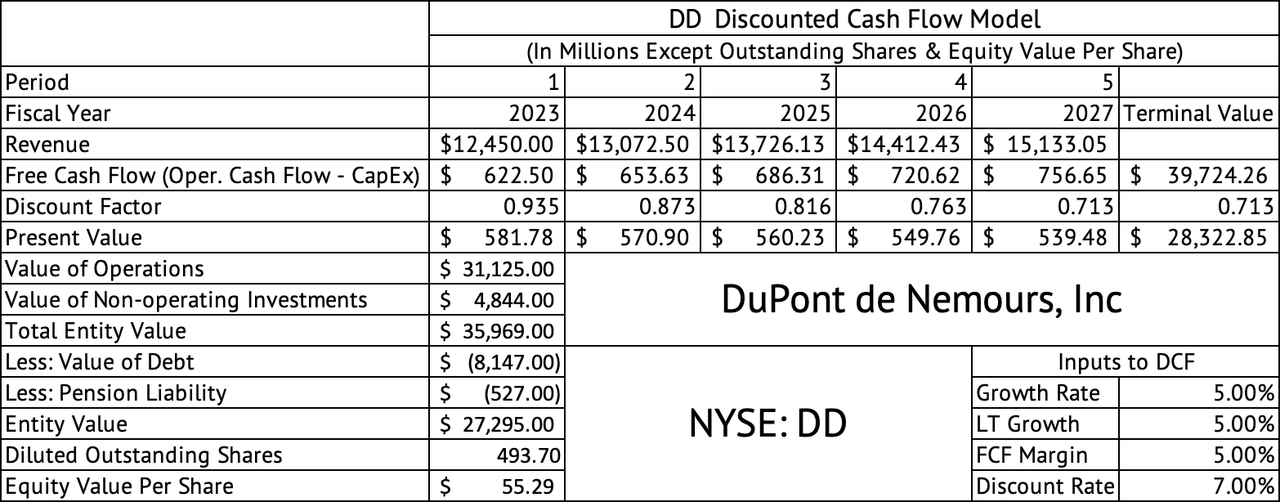

DuPont can be a long-term portfolio holding if purchased at a reasonable valuation. The stock is overvalued at current prices. The company is trading at a forward GAAP PE of 28x compared to the Materials sector median of 14x. But, on a forward EV to EBITDA multiple, the company looks reasonable, trading at 11.7x. A discounted cash flow model estimates the per-share equity value at $55 (Exhibit 2). This model makes generous assumptions for the company’s revenue growth and discount rates. A 5% revenue growth and a 7% discount rate are assumed for this model. A 5% free cash flow model is assumed, which may be too conservative for this company based on its long-term prospects.

Exhibit 2:

DuPont Discounted Cash Flow Model (Seeking Alpha, Author Assumptions & Calculations)

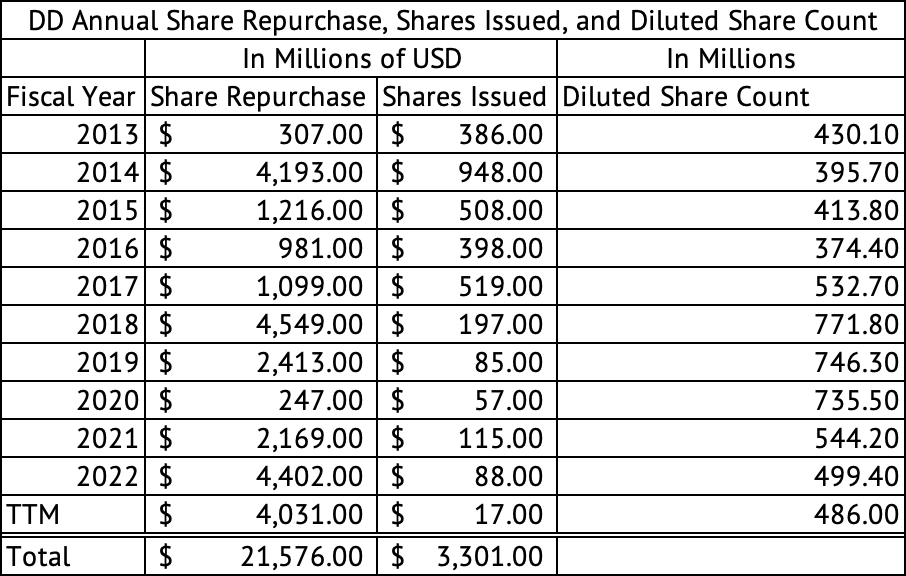

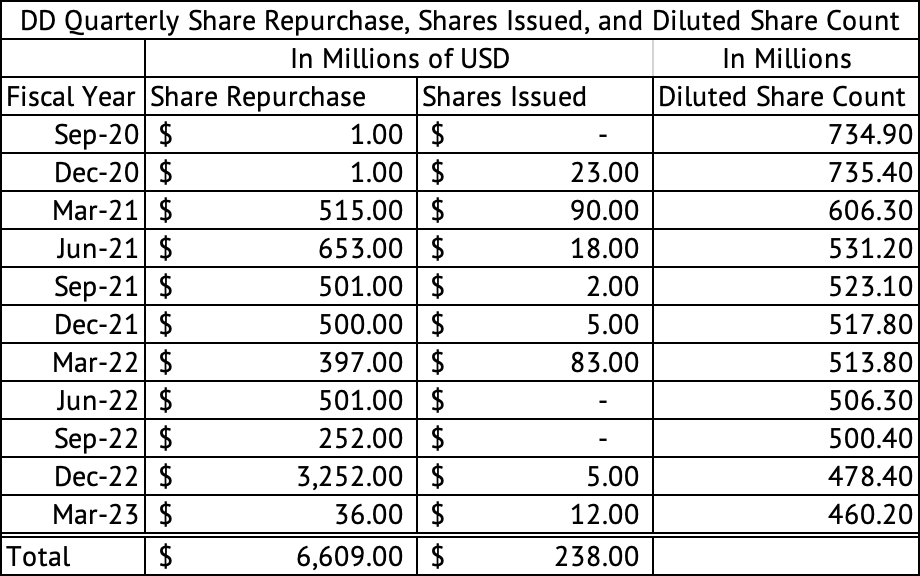

The stock’s 2% dividend yield is low but safe, with a payout ratio of 39%. The company’s priorities for its excess cash are share buybacks and acquisitions. So, dividend growth may take a backseat based on the acquisitions it might make. The company has spent $21.5 billion on share buybacks since 2013 and has issued $3.3 billion in new shares (Exhibit 3). In effect, $18.2 billion of shareholder cash was used to reduce the shares, while the rest was used to reverse dilution effects from the issued shares. The company used the proceeds from its divestitures to make massive share buybacks over the past few quarters. The company made $6.6 billion in share repurchases since September 2020. Share buybacks are the company’s top priority for its capital (Exhibit 4).

Exhibit 3:

DuPont Annual Share Repurchase (Seeking Alpha, Author Compilation)

Exhibit 4:

DuPont Quarterly Share Repurchase (Seeking Alpha, Author Compilation)

Although the yield is better than the 1.5% yield of the Vanguard S&P 500 Index ETF and the 1.9% yield offered by the Vanguard Materials Index ETF, it may be best for investors to wait for the stock to pull back and its yield to rise to 2.5%. The stock would have to drop closer to $57 to yield 2.5%. The stock is overvalued based on the valuation metrics, discounted cash flow model, and dividend yield.

DuPont’s healthcare business can provide long-term revenue and profitability growth.

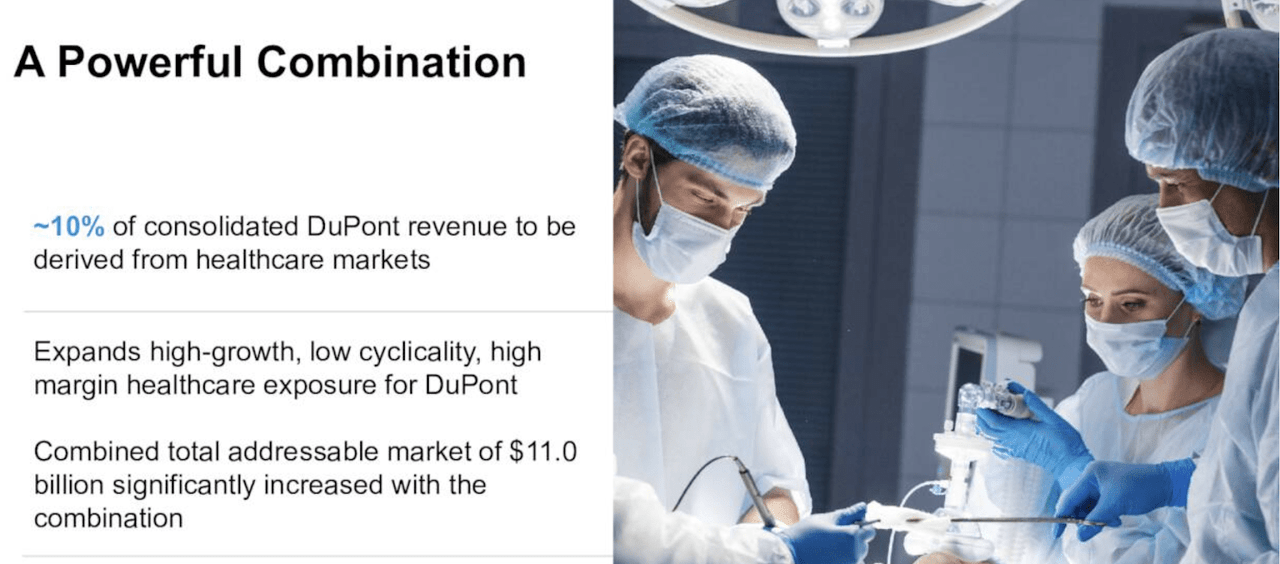

The company added to its healthcare business by acquiring Spectrum, a leading manufacturer of critical components and devices for medical markets. It paid $1.75 billion for the company. DuPont expects the company to generate $500 million in revenue in 2023. After accounting for cost synergies, DuPont paid 13.2x EBITDA for Spectrum. Spectrum generates 25% in EBITDA margins based on this EBITDA multiple. Since September 2020, the company has averaged a 24% EBITDA margin with low variability (standard deviation) of 0.98%. With this acquisition, the company now generates 10% of its revenue from the healthcare sector (Exhibit 5).

Exhibit 5:

DuPont’s Growing Healthcare Business (DuPont Investor Presentation)

Healthcare is a growing business worldwide and can grow faster than the GDP. The aging demographics are a factor behind the increased healthcare spending in the developed world. For DuPont, the healthcare sector can reduce its revenue and profitability volatility. But, the runaway inflation in the healthcare sector, especially in the U.S., is a major concern. The U.S. is already spending over $4 trillion on healthcare annually, amounting to $12,914 per person, the highest in the world. The Centers for Medicare and Medicaid recently forecasted that annual U.S. healthcare expenditures will reach $7.2 trillion by 2031. Assuming the economy is much larger by then, the healthcare expenditures would amount to 20% of GDP.

Unsurprisingly, every company, from Best Buy (BBY) to Walmart (WMT), wants to capture revenue from this fast-growing healthcare sector. DuPont has a much higher probability of succeeding in its push to increase its healthcare revenue, given that it has been supplying many healthcare markets and players in the sector for many years. Investors looking to own DuPont for the long term should closely watch the company’s progress on the healthcare front and assess the stability in revenue and profitability. The company could command a higher valuation as the healthcare sector accounts for a much more significant percentage of its overall revenue than its current 10%.

The underwhelming performance of the Materials sector over the past year.

The past year has been interesting for the stock markets. In October 2022, the S&P 500 Index was in a bear market, dropping over 20% from its highs. Almost everybody was predicting that the U.S. would enter a recession in 2023. Many people loudly complained that we were talking ourselves into a recession. Fast forward to June 2023, the U.S. economy is yet to enter a recession, and the stock market has seen one of the most astounding recoveries ever, with the S&P 500 Index going from 3,491 last year at its bottom to 4409, a return of 26%. On a 1-year basis, the S&P 500 Index (SP500) has returned 20.2%, while the Vanguard Information Technology Index fund ETF (VGT) has returned an astounding 39%.

The hype surrounding AI has pushed some technology stocks to stratospheric heights. But, not all sectors have participated in this rally. The Vanguard Materials Index ETF (VAW) has returned just 10% over the past year, and the Vanguard Financials Index Fund ETF has returned 7.6%. The lag in the performance of the Materials sector is concerning and may indicate the weakness in the global economy. Although there is a lot of focus on the digital world, the physical world is where people live, and materials are an integral part of every consumer’s life. So, when the Materials sector is lagging, either the economic conditions have to improve for the Materials to catch up to the rest of the sectors, or the rest will soon drop to reflect the actual drop in global demand and, in turn, revenues and profitability.

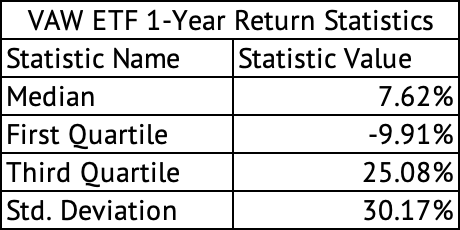

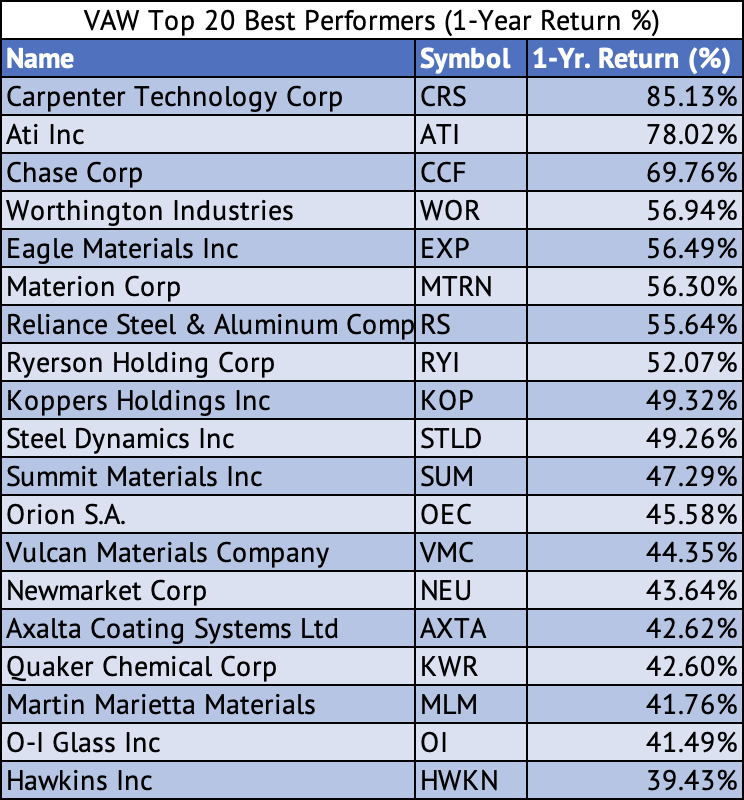

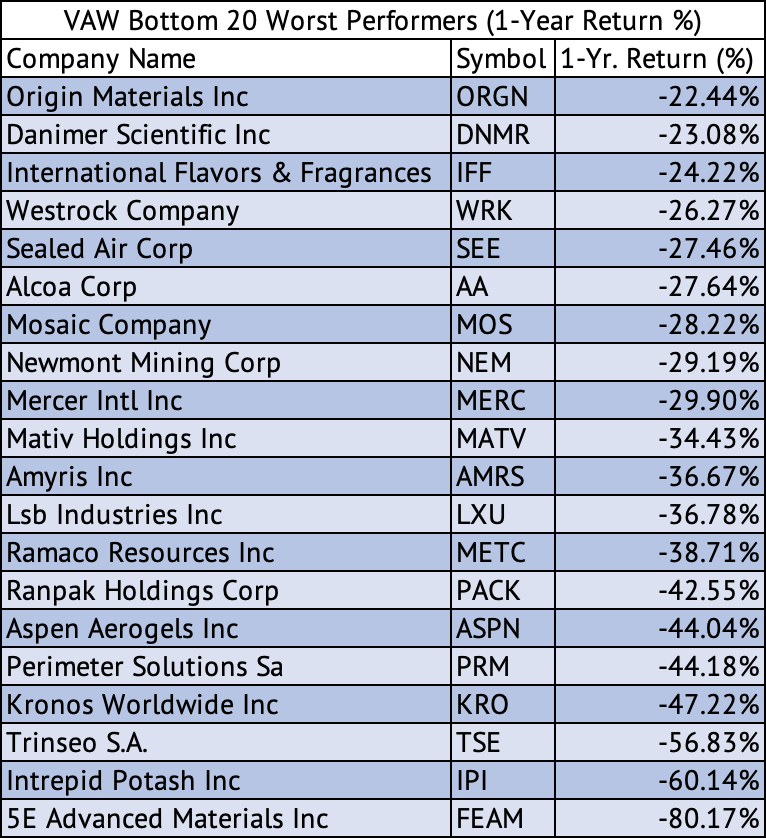

The Vanguard Materials Index ETF companies had a median return of 7.6% (Exhibit 6). About 25% (first Quartile) of the companies dropped over 9.9%, and 75% (Third Quartile) returned below 25% over the past year (Exhibit 6). Carpenter Technology Corporation (CRS), a manufacturer, fabricator, and distributor of specialty metals used in aerospace, defense, medical, and other end markets, is the best-performing stock in the index with a return of 85% (Exhibit 7). Seven companies in the Materials Index have lost over 40% over the past year (Exhibit 8).

Exhibit 6:

VAW ETF 1-Year Return Statistics (Barchart.com, Data Provided by IEX Cloud, Author Calculations)

Exhibit 7:

VAW ETF Top 20 Best Performers Based on 1-Year Returns (Barchart.com, Data Provided by IEX Cloud, Author Calculations)

Exhibit 8:

VAW ETF Bottom 20 Worst Performers on a 1-Year Return Basis (Barchart.com, Data Provided by IEX Cloud, Author Compilation)

One company among these bottom performers, Kronos Worldwide (KRO), caught my attention. Kronos produces Titanium Dioxide, an essential product in paints and coatings, cosmetics, glass, and ceramics. Seeking Alpha analyst, Elah Valley Capital, says that since Kronos is in a cyclical business, it may be an opportunistic buy after the stock’s steep fall, losing over 50% in the past year.

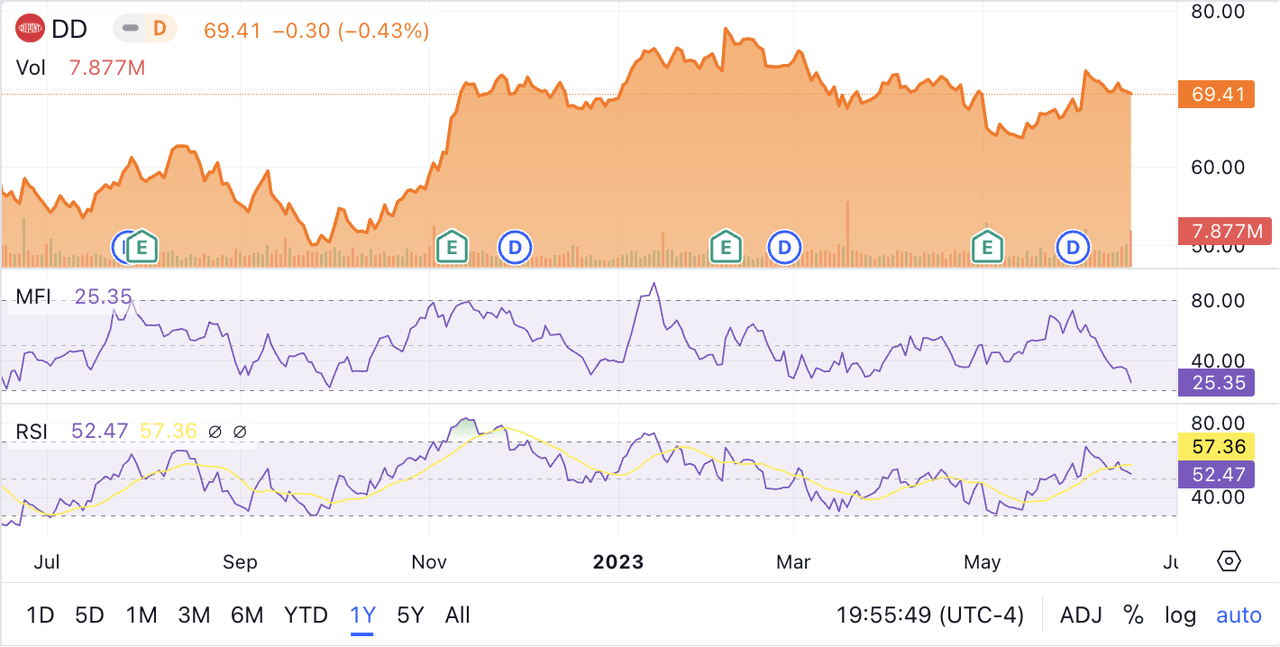

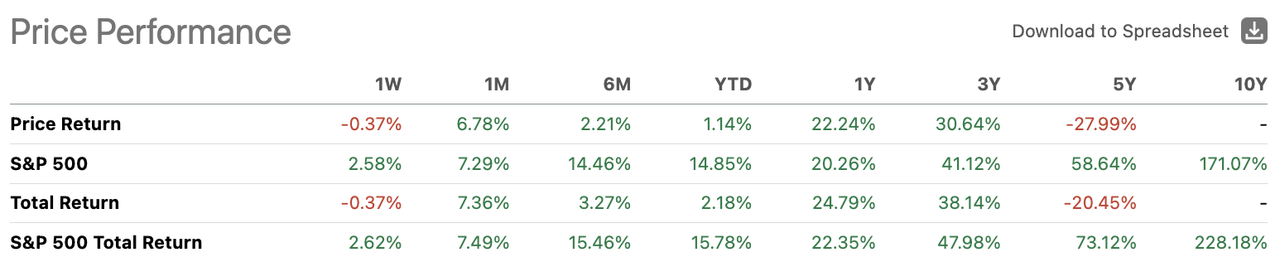

DuPont’s one-year return of 22% falls in the third quartile in the Materials sector. The stock’s momentum may weaken, with RSI and MFI technical indicators trending toward oversold levels (Exhibit 9). But, the stock is overvalued at these levels. The stock has underperformed the S&P 500 over a 3-year and 5-year period (Exhibit 10). Over the past few years, DuPont has transformed itself into a more focused company, and its chosen end markets, such as healthcare products, have the potential to produce good long-term returns.

Exhibit 9:

DuPont’s RSI and MFI Technical Indicators (Seeking Alpha)

Exhibit 10:

DuPont’s Price Performance (Seeking Alpha)

DuPont serves attractive end markets, and investors should keep an eye on its growing healthcare business. Acquisitions and share buybacks are the company’s top capital allocation priorities. Dividend growth may take a backseat, so investors should wait for the stock to pull back and yield 2.5% before buying. As a long-term dividend income investor, investing in a low-yield stock may not be prudent. Even a 2.5% yield in today’s rate environment may be low, but a growing dividend could increase an investor’s yield-on-cost. DuPont could generate superior returns for the patient long-term investor when bought at a more reasonable valuation.

Read the full article here