Mixed near-term prospects for Autodesk (NASDAQ:ADSK) continues to deliver strong revenue and profit growth but is undergoing temporary headwinds to free cash flows which should resolve longer term. Well positioned to benefit from long term growth opportunities in cloud adoption.

Q1 2024: revenues and profits up but soft guidance

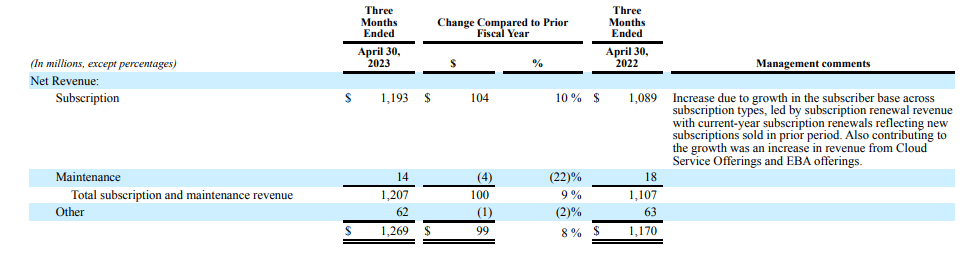

For Q1 2024 (quarter ended April 2023), Autodesk’s revenues rose 8.5% YoY on a reported basis (up 12% YoY on a constant currency basis) to USD1.26 billion. The performance is largely consistent with the previous quarter (Q4 2023) when reported revenues rose 9% YoY (12% on a constant currency basis).

Subscription revenues were up 10% YoY driven by subscriber growth, a noteworthy performance considering macroeconomic headwinds. Billings rose 4% YoY USD1.17 billion while current remaining performance obligations (recognized as the amount of revenue expected to realize over the next 12 months) rose 12% to USD3.5 billion.

Autodesk 10-Q, Q1 2023

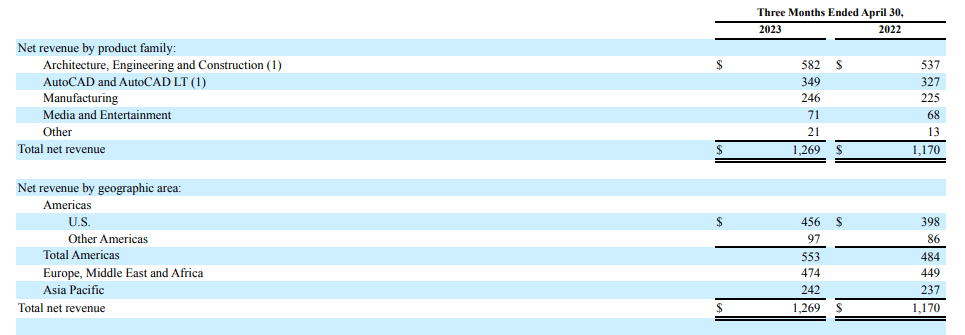

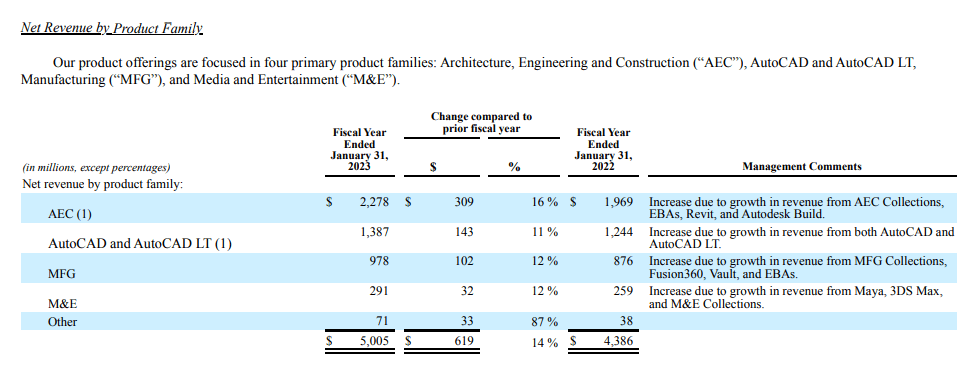

All product segments and regions saw revenue growth in the quarter.

Autodesk 10-Q, Q1 2023

GAAP operating income rose to USD217 million compared with USD214 million in the same quarter last year.

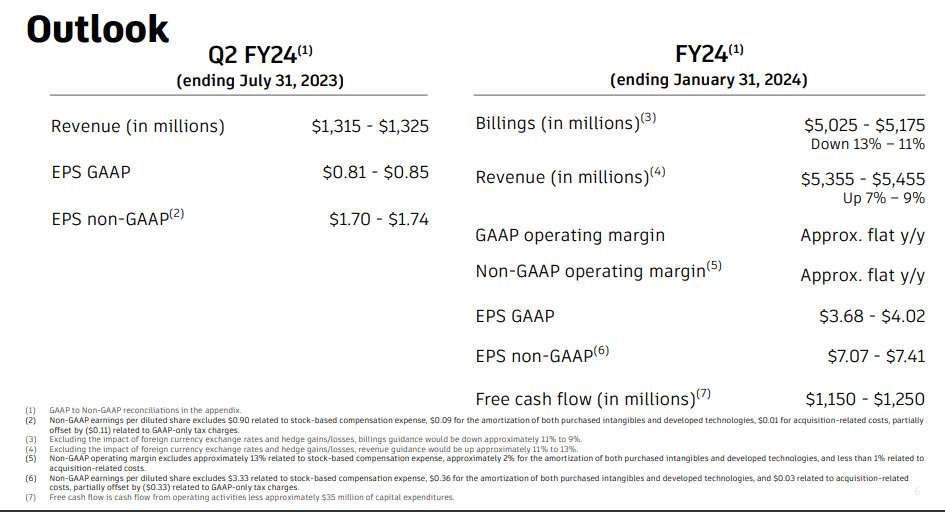

Near term, Autodesk’s outlook is mixed. Revenues are projected to grow in the high single digits (7%-9%) but billings are expected to decline by 13%-11% on the back of the company’s transition of customers’ multi-year contracts from upfront billings to annual billing installments. The transition to annual billings is also expected to impact cash flows with full year FY2024 free cash flows projected to drop to USD1.15 billion – USD1.25 billion, a significant decline compared to the USD2.03 billion in free cash flows generated last year.

Autodesk investor presentation, Q1 2023

Despite mixed near term prospects, Autodesk’s longer term prospects are more optimistic thanks to positive trends like cloud adoption and government mandates which bodes well for the company’s two biggest revenue generators.

Increasing cloud adoption in AEC sector an opportunity for Autodesk’s engineering software

Autodesk generates 45% of revenues from its AEC product family (which includes Autodesk’s portfolio of engineering software such as Autodesk Civil 3D, Autodesk InfraWorks, and Autodesk Construction Cloud).

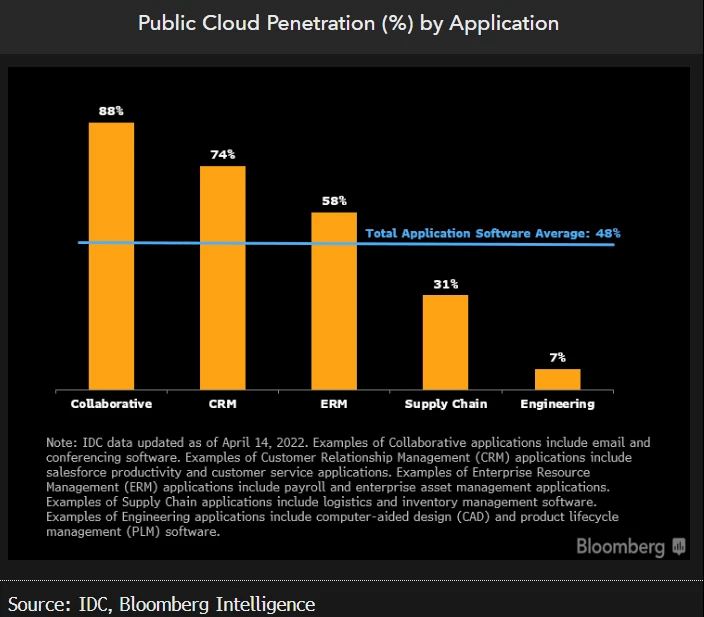

The Architecture, Engineering, and Construction sector (AEC) is known to be among the least digitized sectors of the economy, and cloud adoption remains relatively low.

For instance, according to data from the IDC, public cloud represents just 7% of engineering software sales, compared with 70% for customer relationship software sales and an average of 48% for the overall application-software market, an opportunity for players like Autodesk.

Bloomberg

While part of this may have to do with a resistance to change, part of it may also have to do with the difficulty transferring and storing their typically large file sizes over slow networks). 5G adoption (which is still in early stages considering just 30% penetration in the U.S., and nearly 25% in China), and growing remote/hybrid working trends however are serving as catalysts for digitalization presenting an opportunity.

Government mandates propelling BIM software

The construction industry is notoriously slow to embrace innovation but government mandates making BIM (Building Information Modeling) software mandatory, is driving increased BIM software adoption. About 72% of U.S. construction companies use BIM software, and the figure is likely lower in developing economies – a growth opportunity for Autodesk’s Revit, one of the world’s leading BIM software tools on the market with a market share of more than 40% according to some estimates. Autodesk does not break down Revit’s revenues but it is part of Autodesk’s AEC product family, its biggest revenue generator, which was also its fastest-growing last year with sales growth of 16% YoY.

Autodesk FY2023, 10-K

Cloud adoption growth opportunity in CAD software

Autodesk generates about 27% of its revenues from AutoCAD software sales which is a leader in the CAD software market with a (AutoCAD a 37% market share followed by Dassault System’s Solidworks 12%. Customer migration from on-premise to cloud versions of their AutoCAD software still has (Autodesk stopped selling perpetual licenses in 2016, the maintenance plan was discontinued in 2021, and multi-user plans were stopped just last year).

The cloud-based CAD SaaS market is projected to grow by the double digits over the next few years, far outstripping the general CAD software market which is projected to increase by the mid single digits according to various research producer providers. Not only could a subscription model generate recurring revenues over time compared with a perpetual license model, it could also potentially expand Autodesk’s user base to cater to smaller companies (and therefore capture market share) who previously may have struggled to afford the most recognized CAD software in the market.

Continued innovation could support market share

Autodesk’s continued innovation efforts could help sustain market share. The company’s pay-as-you-go Flex offering for instance could significantly expand its reach to occasional users. Meanwhile Autodesk continues to add new features to its programs, the most significant one lately being the availability of Apple silicon-native programs for AutoCAD and Maya, announced this year. Like rival Dassault Systemes, Autodesk has been quick to incorporate AI into their programs to enhance functionality and optimize user productivity (for instance through AI-powered predictive/generative tools used to speed up tedious processes)

Risks

Open source software

Open source software which is free to use is becoming extremely good and emerging as formidable competitors to paid versions from software developers like Autodesk. Blender for instance is a free and open-source 3D graphics and modeling software, a formidable competitor to Autodesk’s Maya (both of whom together dominate the 3D graphics space).

Technology risks

Emerging technologies and trends such as digital twinning may reduce physical prototyping and therefore potentially reduce CAD usage. A recent survey by Altair confirmed a surge in digital twin adoption worldwide, but more importantly, about two-thirds of those surveyed expect digital twin solutions to make the need for physical prototypes obsolete (translation: less physical prototyping potentially means less usage of CAD software which may impact usage of one of Autodesk’s bread and butter products – AutoCAD). Digital twins are more accurate than CAD drawings, which means fewer design iterations with better outcomes. BMW offers a case in point; the German premium car maker has already embraced the technology, with the company building a digital twin (using Nvidia’s Omniverse software) of a new factory that will open for real in 2025. Prior to the new technology, engineers would draw “millions” of CAD drawings, and meet for thousands of hours but despite all the planning there would still be a long list of bugs to fix when the factory finally opens. A digital twin allows them to find bugs way before the factory is constructed, saving considerable time and effort on modifications and revisions due to design errors. Digital twins are not likely to make CAD programs obsolete however as CAD software would still be necessary to create digital twins themselves but the possibility of reduced usage cannot be ruled out.

Conclusion

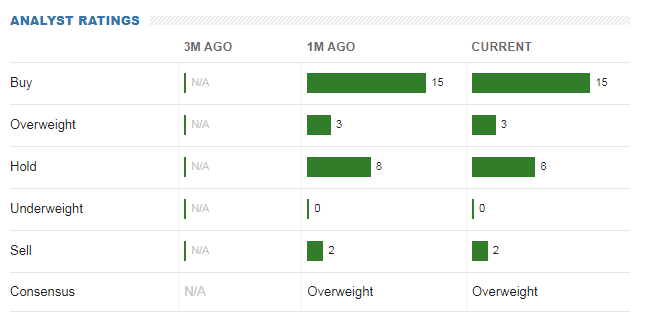

Analysts are mostly bullish on the stock.

MarketWatch

With a market capitalization of USD45 billion, Autodesk is trading at a market value that is roughly 36 times higher than their projected cash flows the current fiscal year which is not exactly a bargain, but considering the company’s free cash flow generation is being impaired by the company’s shift to from multiyear upfront billing to annual contracts (a temporary headwind which should resolve longer term), and the company is well placed to benefit from longer term growth opportunities stemming from an industry-wide shift to the cloud, the stock may be worth a look for longer-term investors.

Read the full article here