Thesis

In this analysis, I delve into the performance and prospects of John Wiley & Sons, Inc. (NYSE:WLY), a key player in the Communication Services sector/Publishing industry. Although the company’s evaluation presents a mixed picture with its ‘B-‘ grade and certain areas of concern, there are also promising signals that point towards potential opportunities for the discerning investor. I explore various financial indicators, from Non-GAAP P/E ratios to dividend yields, and provide a comprehensive review of the firm’s earnings, operational strategies, and potential challenges. While some caution is merited, there are strong indications that holding onto WLY’s stock could prove beneficial in the longer run.

Company Overview

John Wiley & Sons, Inc. holds a prominent position in the global landscape as a research and educational entity. The company’s operations are categorized into three distinct segments: Research Publishing & Platforms, Academic & Professional Learning, and Education Services.

In the Research Publishing & Platforms division, the company’s offerings span a broad spectrum, providing scholarly journals that cater to a vast array of disciplines such as physical sciences, health sciences, social sciences, and humanities. This division not only serves individual researchers, academic libraries, and professionals but also collaborates with learned societies, corporate entities, and government libraries. A notable aspect of this segment is the Literatum platform – a dynamic software and service that empowers scholarly societies and publishers to manage, market, and enhance their web content. The company’s distribution strategy here leverages various channels, from research libraries and library consortia to online booksellers and professional society members.

The Academic & Professional Learning division pivots on the provision of education publishing and professional learning services. This includes a gamut of products such as scientific, professional, and educational print and digital books, digital courseware, and test preparation services. This segment primarily caters to students, professionals, researchers, libraries, and corporations. To maximize reach, this segment employs various distribution channels, encompassing chain and online booksellers, colleges and universities, corporate entities, and online applications.

The third segment, Education Services, specializes in providing online program management services for higher education institutions. In addition to this, it offers talent development services, including placement and training solutions for professionals and businesses.

John Wiley & Sons, Inc., a company with a remarkable legacy dating back to 1807, anchors its operations from Hoboken, New Jersey. As it evolves in this ever-changing digital era, the firm continues to remain at the forefront of innovative research and education services, bridging the gap between knowledge seekers and knowledge providers worldwide.

Expectations

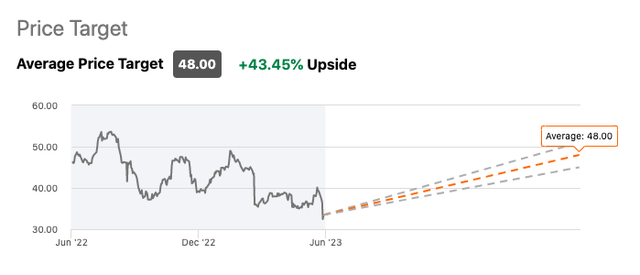

Overall, Wall Street projects a rather robust upside projection of over 40% with an overall “buy” consensus for the stock.

Seeking Alpha

Performance

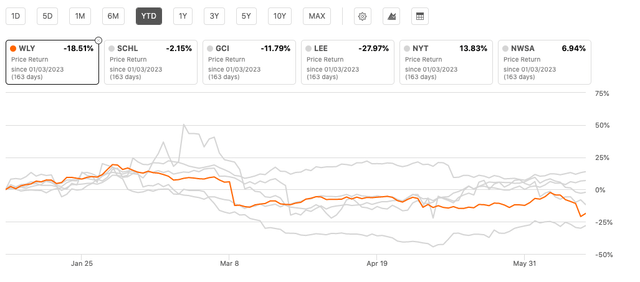

However, WLY is almost in last place with a -18.51% price return when comparing its YTD performance against its peers.

Seeking Alpha

Valuation

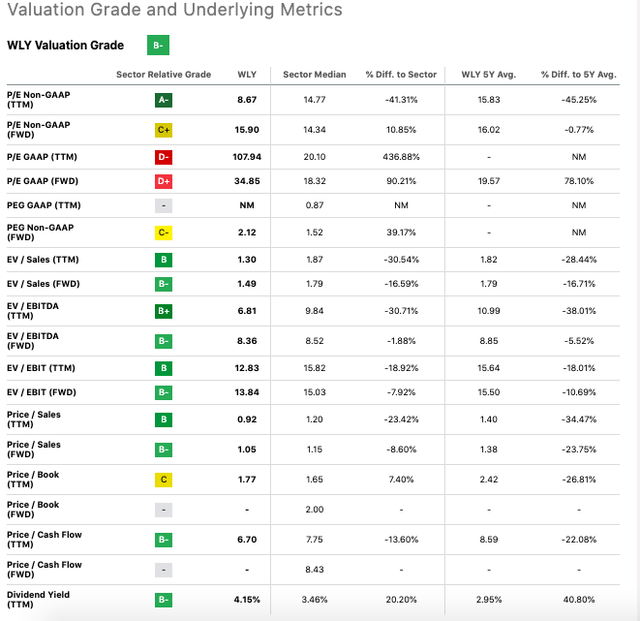

John Wiley & Sons presents a mixed bag when evaluated against key valuation metrics and its sector median. Although some caution may be warranted based on specific measures, I believe there are strong indicators suggesting potential opportunity for the astute investor.

First, it’s imperative to acknowledge the ‘B-‘ grade (see below) assigned to WLY, a reflection of its valuation relative to the Communication Services sector/Publishing industry. Although not a top-tier ranking, it nonetheless suggests a modest level of relative value.

One standout attribute is the Non-GAAP P/E ratio on a trailing twelve months (TTM) basis, which, at 8.67, stands significantly below the sector median of 14.77 and WLY’s 5-year average of 15.83, indicating a substantial discount of 41.31% and 45.25%, respectively. The Forward P/E, although marginally lower than the five-year average, still indicates a premium to the sector median.

Seeking Alpha

However, there are some areas for concern. The GAAP P/E ratio (both TTM and Forward) presents a less rosy picture, far exceeding both the sector median and the 5-year average, indicating the company might be overvalued from a GAAP earnings perspective.

In the case of EV/Sales and EV/EBITDA, Wiley’s figures are significantly lower than the sector median, indicative of potential undervaluation. Similar trends are observed in the EV/EBIT and Price/Sales metrics.

The Price/Book TTM value, though slightly higher than the sector median, is substantially lower than Wiley’s five-year average, implying that the company’s assets are undervalued.

Another encouraging aspect is Wiley’s dividend yield, which at 4.15% TTM, provides an attractive income stream, exceeding both the sector median and its own five-year average by 20.20% and 40.80% respectively. This indicates a generous reward for shareholders even in challenging times.

Seeking Alpha

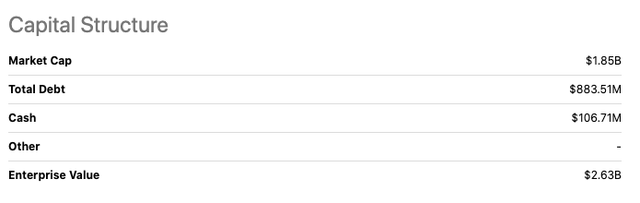

And finally, turning to the capital structure, Wiley possesses a market cap of $1.85B and carries a substantial debt load of $883.51M. However, the firm maintains cash reserves of $106.71M, culminating in an enterprise value of $2.63B.

Q4 2023 Earnings Bullish Takeaways

Even though there has been a slight contraction in revenues, it’s evident that John Wiley & Sons have masterfully weathered this storm by delivering a marked upswing in both the adjusted EPS and adjusted EBITDA, posting gains of 32% and 23% respectively. What this tells me is that the firm has been able to wield its scalpel effectively in paring down expenses and executing on its restructuring plan. This agility under pressure not only underscores the management’s dexterity in navigating through rough patches, but also keeps the bottom-line robust, even in the face of top-line shrinkage.

Persistence in the Research Sector

The Research Publishing arm of the company has encountered some turbulence, as evident from a 5% contraction in the last quarter. However, by no means does this signify an alarming downtrend. Rather, the company’s management projects a strong rebound by fiscal ’25. On the earnings conference call, EVP & CFO Christina Van Tassell noted:

Research Publishing revenue declined 5% this quarter and 1% for the year. Results were impacted by the Hindawi disruption and lower article volume, as Brian [CEO] discussed. Absent Hindawi publishing revenue for the quarter was essentially flat and up modestly for the year. As a reminder, we expect the Hindawi pause to continue to weigh on our results in fiscal ’24 but largely recover in fiscal ’25.

This optimism hinges on their potent strategy of transitioning from legacy read-only subscriptions to more innovative and revenue-generating transformational read and publish models.

With 79 new transformational agreements inked, encompassing a massive consortium of nearly 3000 institutions, the company’s footprint in this domain seems to be expanding. Moreover, the company’s astute leveraging of AI for document classification points towards an intent to streamline operations, which should add another layer of efficiency to their business model.

The company’s financial footing remains rock-solid, as reflected by the $107 million of available cash and a substantial $749 million in untapped revolving credit. The net debt to EBITDA ratio stands at a healthy 1.5, reinforcing the notion that the company has a tight rein on its leverage. This combination of liquidity and well-managed debt puts the firm in a comfortable position to counter unexpected economic headwinds and capitalize on promising investment opportunities.

Impressive Cost Savings and Streamlined Operations

In a commendable strategic move, the company is in the process of rolling out a comprehensive business optimization program. This innovative initiative seeks to reduce corporate overheads and introduce greater operational efficiencies into the operating mechanism, according to company estimates, this program should generate run-rate savings of at least $100 million over three years, not only enhancing short-term bottom line performance but also setting the foundation for long-term operational excellence and profitability.

Risks & Headwinds

We’re seeing a challenging landscape for Wiley & Sons as revenue declines echo across all business segments. As mentioned above, the Research Publishing division, a cornerstone of the company, has taken a significant hit this quarter with a 5% downturn, and a 1% dip for the year. The headwinds for this segment seem to stem largely from disruption caused by competitive entry Hindawi and the downtick in article volumes. Although management is optimistic, this decline poses a serious concern for Wiley’s future growth prospects in this segment.

Academic Segment Falters

In another blow to the company’s financials, both publishing revenue and university services have seen a contraction, chiefly impacted by restrained consumer spending, inventory cutbacks at a major online retailer, and enrollment hurdles. The ripple effects of these challenges forecast a continued compression in the near-term, painting a somewhat grim picture for this sector of Wiley’s operations.

Wiley’s bold strategy of shedding certain businesses and executing significant strategic and structural overhauls does not come without its perils. Indeed, such radical transitions can create waves in operational performance, potentially leading to short-term disruptions and inefficiencies. The implications are clear – the company needs to navigate this transitional phase with careful deliberation and effective change management to mitigate any operational disturbances.

Bearish Guidance for Fiscal ’24

Looking ahead, the projections for fiscal ’24 are not particularly promising. Expectations point towards stagnant Research revenue and a modest dip in the Learning segment. Further exacerbating these concerns is the anticipated decrease in adjusted EBITDA, which would inevitably squeeze the EPS. This narrative signals a challenging fiscal year on the horizon for Wiley & Sons.

And finally, a prominent red flag in Wiley’s fiscal landscape is the upward trajectory of employment costs, driven by a reset in incentive compensation and mounting wage inflation. If these escalating costs are not reined in effectively, it could seriously threaten the company’s margins. Wiley’s management will need to exercise vigilant cost control measures to counteract this potential profitability erosion.

Final Takeaway

Despite the evident challenges in revenue growth and cost escalation, the robustness of Wiley’s financials, coupled with the company’s strategic transitions and effective cost management strategies, signal potential opportunities for future growth. While fiscal ’24 might be rough, long-term prospects, underscored by the company’s unwavering commitment to innovation and operational efficiency, provide a compelling argument to hold onto WLY shares in anticipation of a bounce back in the subsequent years.

Read the full article here