Investment Thesis

The global markets for agriculture, gas, and fertilizers are complex and notoriously difficult to predict accurately. In the short term, it depends on weather and European production; in the long term, it depends on the demand for corn, which has risen steadily over the long term, but it is not a given that this will continue. Demand could decline, especially if ethanol demand falls, which has tended to be the case for several years. Still, CVR Partners, LP (NYSE:UAN) should remain an attractive dividend stock for several years. For me, the stock is not attractive due to a tax disadvantage for foreigners. Moreover, the stock is still in an intact downtrend.

About Predictions

First of all, I would like to say thanks to Publius, who probably holds the record for the article with the most comments on Seeking Alpha and who was crucial in bringing the company to the attention of a large audience. The entire community has done a great job of regularly posting the news in the comments and what it might mean for the stock.

It is Difficult to Make Predictions, Especially About the Future

By Unknown

But it is also an example of the difficulty of predictions. I don´t mean this disrespectful at all. I just want to say that certain developments turned out quite differently than expected. The units’ performance and dividend payouts tended to be overestimated. The natural gas price has developed differently than many had anticipated.

I also made similar mistakes with another investment that competes with Potash. With the Brazilian company Verde AgriTech. In 2022 the market was turbulent, but ultimately there was oversupply instead of undersupply:

At the onset of the Ukrainian war, in February 2022, concerns that geopolitical sanctions against Russia would cause significant shortage of potash fertilizers resulted in a 154% surge in the average price of potash between March and July, compared to 2021. However, this fear proved unfounded, as there was actually a glut of potash in the market due to increased availability, resulting in a 45% surge in potash imports by Brazil over the same period, compared to 2021. This oversupply, combined with a 15% drop in potash consumption in Brazil in 2022, contributed to a challenging market for fertilizer producers.

Verde AgriTech Slumps Due To Weaker Than Expected Outlook

Over time, you could also notice more and more articles being written about CVR Partners, which were extremely bullish at the beginning and got many comments. Towards the end of 2022, when it became clear that the extremely bullish scenario would not materialize after all, the articles moved more towards a hold rating, and the comments per article became fewer.

I believe this is a valuable lesson. Even with such massive combined forces of hundreds of contributors over months, it was still impossible to predict the future, especially with such complex global markets as the interplay of agriculture, gas market, and fertilizer. In addition, there are impossible to predict things such as weather, how much gas will be converted to electricity, etc. One or the other may contradict in this statement, but I was also invested here for several months and a silent reader in the famous article with 25k comments. As I said, no one should feel attacked, and numerous people have made a lot of money with this stock. However, I remember very clearly that the further performance and the dividend payout tended to be overestimated, which also means some people jumped too late on the train. Why are crash prophets wrong again and again? Why are the basic assumptions of the alleged climate catastrophe so fuzzy? Why are the sanctions against Russia such a failure? We tend to project the current situation into the future. It is very difficult for the human mind to take into account the behavioral changes that will occur as a result of certain problems. In fact, this is impossible.

Some examples of the difficulty of prediction

An example of the difficulty of prediction is how Germany easily got through the winter. After the Nord Stream pipelines were blown up and the first cold days in November, many people (myself included) assumed that the reserves would not last through the winter. Empty gas reserves would have been a disaster for the power supply and the heating market. I followed this development very closely because my whole family lives in Germany.

In the end, however, everything was no problem at all. On the contrary: it was an example of the adaptability of markets and people. Where possible, people have reduced consumption, saved, or switched to other methods. In addition, LNG was purchased, and the worst could be averted with ease. Now we are at a point where again similar things are predicted for the following winter, especially after the gas price has shot up recently, including the news of the closure of the largest European gas field In the Netherlands.

Of course, expressing assumptions with probabilities and identifying the most likely scenarios is a great strategy. What we generally underestimate is, as I said, the adaptability of the markets, and the more connected the world is, the faster such mechanisms work.

Another example is the complex assessment of the oil markets. For months I have wondered how low the oil market remains despite production cuts by OPEC+, the Chinese economic opening, more demand from India, etc. And again comes a point with which no one would have expected; suddenly, Iran reached a five-year high in its production And now stands for 3% of world production.

I have heard a lot about possible food shortages in the past two years. One of the underlying assumptions was elevated fertilizer prices, which in turn could lead to lower food production, the rich countries buying everything away from the poor, and so on. I am not saying this is out of the question; maybe it will happen in the next few years. However, it has almost always been the case that the greatest catastrophe is averted in the end. Then, when natural gas and fertilizer prices are at their highest, millions of small mechanisms begin to emerge that work together to secure the food base.

Q1 Financial results

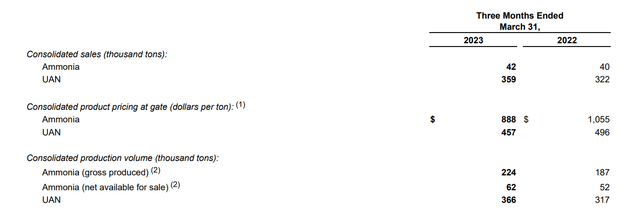

The company reported net income of $102M for the first quarter of 2023, compared to $94M in the same period last year. EBITDA was $124M for the first quarter of 2023. Despite the decrease in prices, the company has managed to increase net income, which is also due to the record production with a combined ammonia utilization rate of 105 percent.

CVR Partners’ average realized gate prices for UAN showed a reduction over the prior year, down 8 percent to $457 per ton, and ammonia was down 16 percent over the prior year to $888 per ton. Average realized gate prices for UAN and ammonia were $496 and $1,055 per ton, respectively, for the first quarter of 2022.

Q1 results

Investor presentation

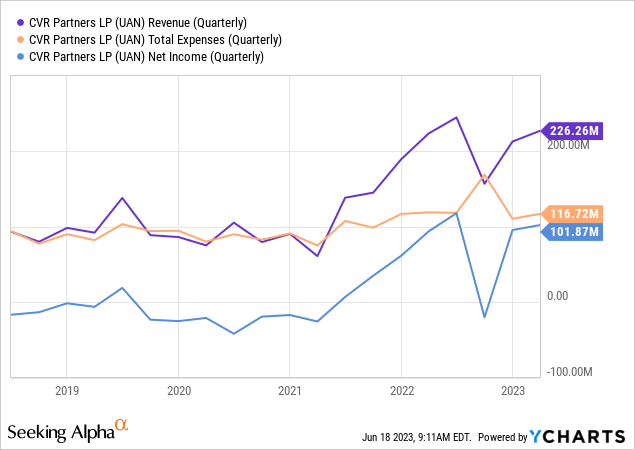

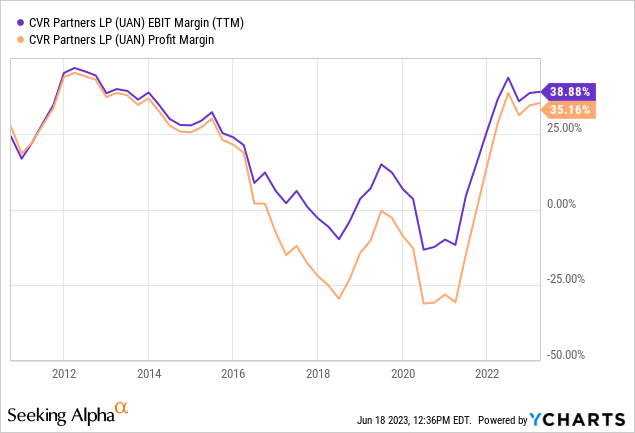

When zoomed out and viewed over a somewhat more extended period, the development of revenue, expenses, and net income looks like this.

At current revenues and margins, the company is a true cash cow.

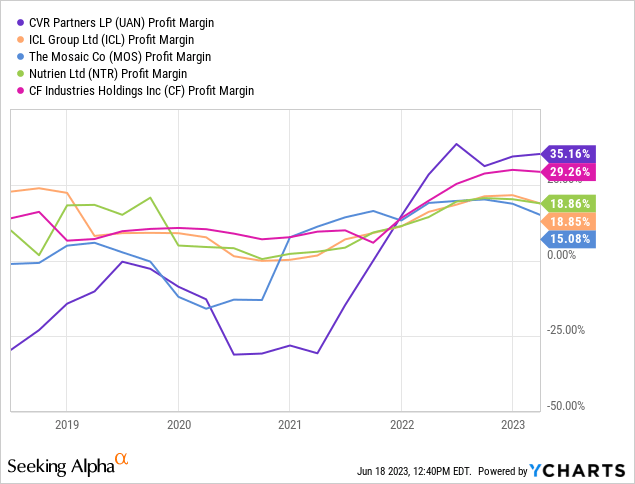

It also looks excellent in comparison with a peer group.

Outlook & Risks

One reason for falling prices was returning production in Europe. Given the figure of 80%, there is further potential for increases.

With sustained lower natural gas prices in Europe in the first quarter, we have seen some of the off-line European nitrogen production capacity come back online. Recent estimates indicate European nitrogen production operating at around 80% of capacity, up from 60% in the fall of 2022.

Q1 earnings call

However, management remains pessimistic about Europe.

While the extreme pressure on natural gas inventories have subsided for now, we do not believe that the structural market issues in Europe have been resolved and should remain in effect over the next 2 to 3 years. We believe there is likely more upside than downside to European natural gas prices from here.

Q1 earnings call

Corn & Ethanol

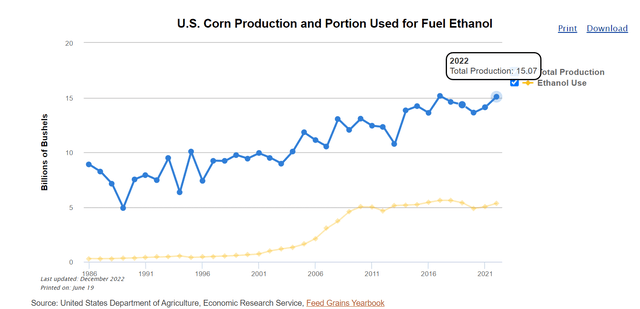

Long-term, I can think of mixed arguments about the development of the corn price and production: Over a more extended period, U.S. corn production has risen steadily, nearly catching up with the 2017 peak in 2022. About one-third of U.S. corn production is processed into ethanol; Here is recent news about the world’s largest ethanol fuel production plant. That could lead to even more corn production in the future.

afdc.energy.gov

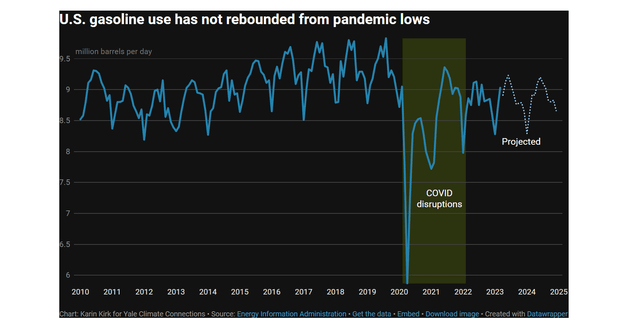

However, it is also the case that ethanol production has been stagnating or even declining for several years. Ethanol demand is directly linked to gasoline demand. What about gasoline demand? Again, pre-pandemic levels have not yet been reached. Will it even be reached again, given the growing share of EVs? Again, hard to say. Will there be an oversupply of ethanol, leading to falling demand for corn? Ammonia prices crash? That is one possible route, but as I said, the central message of this article is these complex correlations are not predictable.

yaleclimateconnections.org

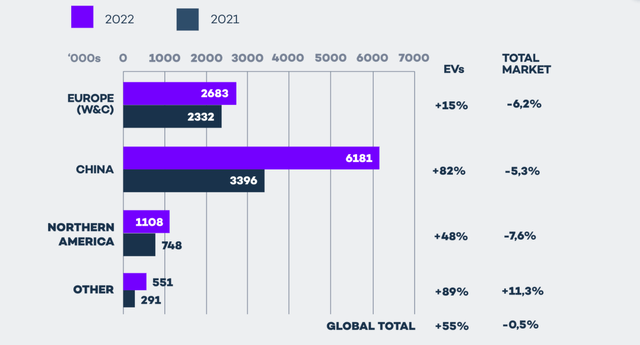

Over the past few weeks, I’ve written several articles about car manufacturers and a long overview article on EV development titled “Power Shift: China’s EV Market, Impact On Western Brands, And Some Trading Ideas”. What could I conclude from this? Rising sales everywhere, falling prices, rapidly improving technology, especially in batteries. In addition, global car sales are lower today than in 2016. It is possible that a high-speed train network will also be built in the U.S. at some point, which would also help to reduce the need for cars. This is a graph from my article.

virta.global

So overall, the risk is that ammonia prices will fall even further. Short-term it depends on the weather, the natural gas market, further European production, and Russian production, which has not disappeared from the world market. In addition, the company states that its utilization rate in Q2 will be more like 95% – 100%, i.e., it will produce less than in Q1. Long-term, it will depend on the general demand for corn, and this is a complex topic.

The dividend yield for this year will also be based on further price development. Several articles and numerous comments have made calculations on this, so it is unnecessary to make any additional forecasts. I’ve seen that most are assuming around $7 dividend in Q2.

One point to consider for foreign investors is the possible different tax treatment due to the LP structure. This was enormously frustrating because the withheld taxes on the dividends was more than twice as high as with other shares, making the share much less attractive to me.

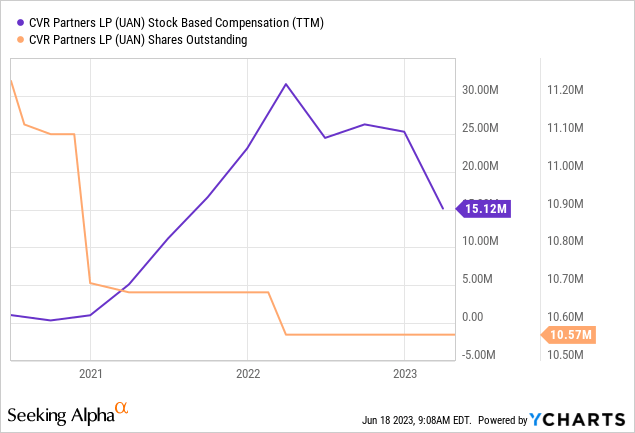

Share dilution, insider trades & SBCs

For me, these three things are standard checks I make in every article, as excessive stock dilution and stock-based compensation can put us, shareholders, at a disadvantage. In addition, insider trades sometimes contain valuable info about the confidence of management itself.

I did not find any information about insider activities. Otherwise, there is nothing significant to report, but I wanted to mention it anyway because it is also info if there is nothing special to see here.

Conclusion

For my taste, this market is influenced by so many factors that it is too difficult to predict. At least at this stage, we are no longer at the beginning of a long-term cycle but somewhere in the middle. However, the aforementioned tax disadvantage on dividends plays a big role, but that is just my case. Most shareholders (at least it seems so) hold the stock for the dividend, so a tax disadvantage takes away part of the biggest argument. If you are a foreign investor, keep that in mind or check the exact agreement of your country concerning American MLPs or LPs.

All in all, the further development of the share and the dividend depend first and foremost on the further fertilizer prices and how much supply comes onto the market overall. For those who want to keep track of all these developments, the regular updates in the corresponding comment columns are enormously helpful.

Read the full article here