Whiplash

Most retailers reporting in May easily beat earnings estimates yet sharply guided down current quarter earnings. The change was sudden but part of a trend of declining growth. Despite consumer spending being the majority of the economy, the market has dismissed this and has continued to rally. Is there a disconnect? This article details what happened and what it means for the economy.

Background

In this article 21 retailers, with annual sales of over $5 billion each, were analyzed for earnings last quarter versus analysts’ estimates. They were also analyzed for changes in analyst’s estimates for this quarter and this year. The retailers in this sample were chosen because all had a quarter ended in April, making them the most recent to report earnings. Many retailers use an April, July, October, and January quarter end.

The change in their earnings estimates for the current quarter in May, 2023 was sudden, and massive. In fact, I do not recall a drop off this fast ever. More astonishing is it happened after a strong earnings season.

These retailers account for about 15% of all retail sales in the U.S. However, on June 15th the government’s retail sales report showed retail sales growing by 0.2% (core sales) to 0.4% (all sales). That is still at or just below the level of inflation but nowhere as bad as the large earnings estimates drops indicate. This discrepancy is analyzed and explained.

In addition to analyzing the discrepancy, 14 headwinds facing retailers going forward are summarized. These headwinds make it likely things will get worse.

Finally, what this means as far as timing of a recession is discussed.

Analysis of 21 Large Retailers

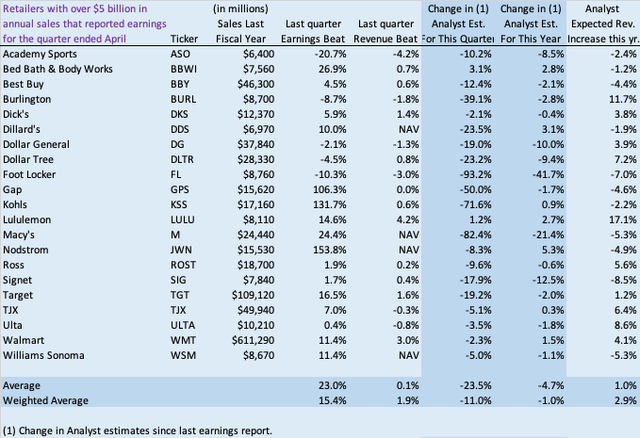

The chart below shows all 21 retailers with annual revenues over $5 billion (found in Value Line) which reported earnings for the quarter ended April 2023 during May 2023. There are a number of other retailers who don’t report using an April ending quarter. These were chosen to get the latest data from the industry and analysts.

Seeking Alpha, Yahoo Finance

Two averages were shown above, a simple average and a weighted average. The weighted average shows the importance of Walmart which accounts for 57% of all sales in this group. Walmart appears to be holding up better than most other retailers but still has had its earnings estimates reduced for next quarter and analysts now only expect a 4.1% revenue growth this fiscal year.

As shown above, the retailers did very well last quarter, beating analyst’s estimates by 23% on average. That is a very large average beat. All but 3 of the 21 beat estimates, also a high number. They beat revenue estimates by much less, just 0.1% on average. The big difference in earnings beats to revenue beats indicates strong pricing power. Retailers were able to raise prices well beyond their inventory costs. However, consumers are showing increasing resistance to higher prices.

Earnings call after call mentioned a sudden drop off in sales in April or May (5 quotes by executives are below).

The following quotes are from the earnings calls transcripts in May.

“we definitely saw deceleration in the business as we got into that April time period. That certainly continued into May and that’s reflected in the guidance”

Academy Sports CEO Stephen Lawrence

“We achieved retail gross margin of 45.6% on a sales decrease of 4% as customer activity declined in the back half of the quarter.”

Dillard’s CEO William Dillard

“Our sales have since softened meaningfully given the tough macroeconomic backdrop, causing us to reduce our guidance for the year as we take more aggressive markdowns to both drive demand and manage inventory,”

Foot Locker CEO Mary Dillon

“As a result of the deteriorating macro environment and impact on consumer spending patterns we saw late in Q1 and throughout May, we are revising guidance to reflect continuation of these trends for the balance of the year.”

Signet CEO Gina Drosos

“we began the quarter with positive comp growth in the month of February and then saw the trends soften into low single digit declines by the end of April and so far into May.”

Target CFO Michael Fiddelke

The result was an across the board, sharp and instant lowering of earnings guidance. Whiplash is a good way to describe it. The stock analysts immediately incorporated this guidance and lowered earnings estimates for this quarter by a whopping 23.5% on average. All but 2 of the 21 have seen this quarter’s earnings estimates dropped since reporting last quarter in May. What is also surprising is that estimates for the full year only dropped 4.7%. This indicates most analysts and retailers expect the drop off to be temporary. So far it hasn’t been temporary. The earnings reports were about a month ago and estimates have stayed down with little change.

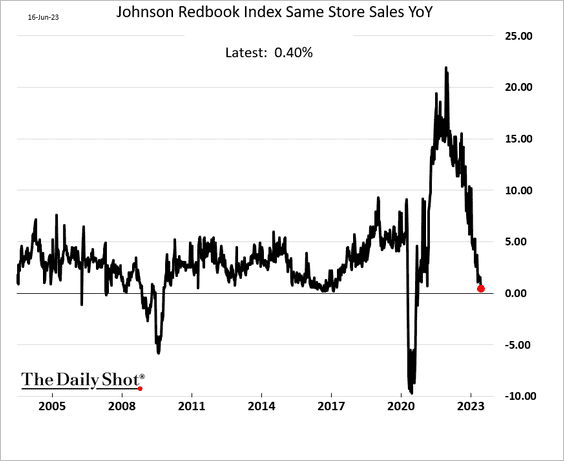

The analysts also expect little revenue growth this fiscal year (for most ending January 2024). The average revenue expectation is up 1.0%, or up 2.9% if using a weighted average. Both numbers are below the current rate of inflation by most measures. Keep in mind these numbers are after store additions so same store sales growth is even less. The chart below shows current same store sales growth at only 0.4% (annual) and dropping fast.

The Daily Shot

It is important to note which segments the earnings estimates dropped the most. It was concentrated with the following three:

1. Big box retailers – These include Macy’s (M) -82.4%, Dillard’s (DDS) -23.5%, Kohl’s (KSS) -71.6% and Nordstrom (JWN) -8.3%. As a group they are getting hammered. This should be no surprise as this has been a weak category for some time. Generally going into a recession, the weakest usually get hit first.

2. Discounters – A bit of a surprise is the discounters including Burlington (BURL) -39.1%, Dollar General (DG) -19.0%, Dollar Tree (DLTR) -23.2%, Ross (ROST) -9.6% and TJX (TJX) -5.1%. This indicates that lower income shoppers are getting hit harder. That is also normal at the beginning of a recession.

3. Apparel Stores – Apparel is often discretionary. These include Foot Locker (FL) -92.3%, Gap (GPS) -50.0%, and Lululemon (LULU) 1.2%. LULU appears to have been spared as it has been such a strong performer in recent years its powering through so far. The other two were clobbered. Also, most big box retailers have heavy apparel sales.

Other categories such as beauty (ULTA -3.5% and BBWI 3.1%) are doing relatively well.

The strength of Walmart indicates the picture isn’t as bleak as the individual company numbers since Walmart represents 57% of all sales of the 21 retailers shown. However, even including Walmart, the drop off was sudden and historically large.

But Overall Retail Sales Expanded in May, What Gives?

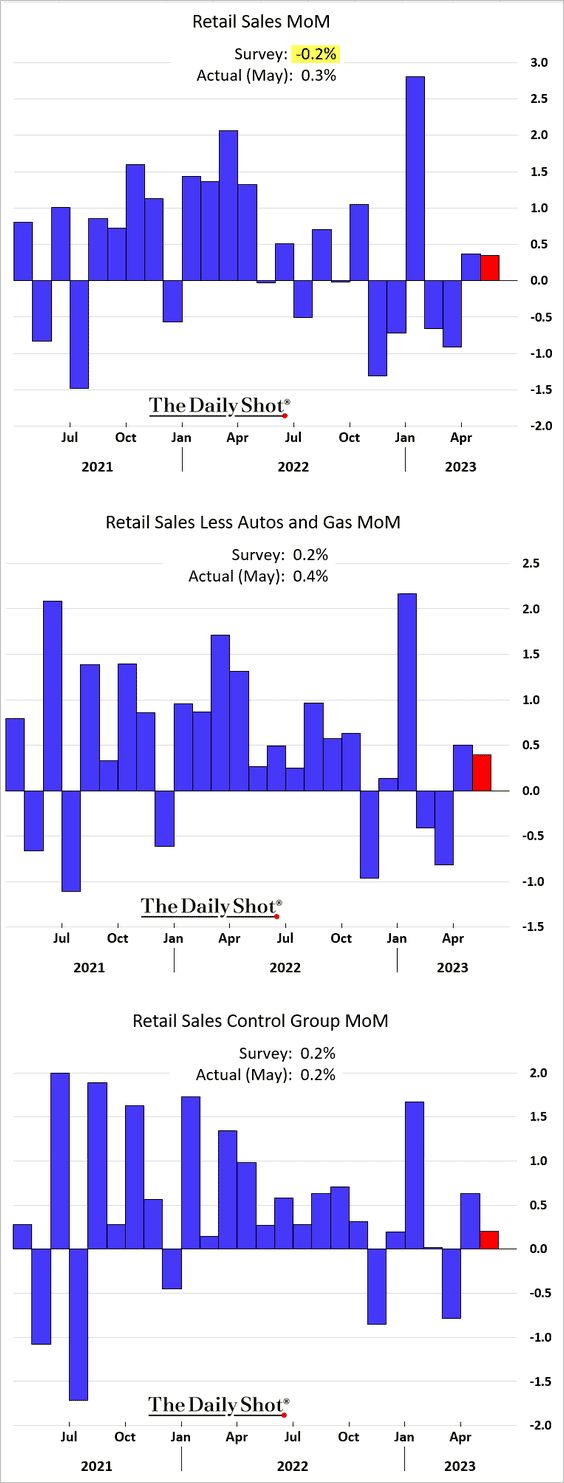

Retail sales in May rose 0.2% to 0.4% month over month depending on the specific report used.. The charts below show retail sales over the past two years.

The Daily Shot

The third category above is a core sales number and excludes volatile segments such as automobiles, gasoline, building materials and food. The charts above show retail sales have been generally weak since November, 2022 with a huge exception in January when they surged. Digging deeper, Trading Economics had the following to say.

“The biggest increases were seen in sales of building materials and garden equipment (2.2%) and motor vehicles and parts (1.4%). The purchases were also higher at food services and drinking places (0.4%); general merchandise stores (0.4%); furniture stores (0.4%); food and beverages stores (0.3%); sporting goods, hobby, musical instrument, & book stores (0.3%); and electronics and appliances (0.2%). On the other hand, sales were flat at health, personal care, and clothing stores and fell 2.6% at gasoline stations and 1% at miscellaneous store retailers.”

The two segments that went up the most were building materials and motor vehicles. Both are excluded in the core retail sales number, which was up 0.2%. Neither of those were covered in the 21 retailers I highlighted as their quarters don’t end in April. Motor vehicles is a volatile category, which is why the second and third categories above exclude it.

The number I go with is the core which showed sales up 0.2%. That is below the current rate of inflation. I use it because it excludes categories that swing quite a bit month to month.

Despite being slightly below the rate of inflation the reports still showed much stronger sales than the 21 retailers I highlighted indicated. So, let’s look at why that may be. The following reasons appear to be a part of it.

1. The monthly numbers are volatile – The charts above show the monthly retail sales numbers jump around. They also get adjusted next month. But the overall trend is down and now below the rate of inflation.

2. Walmart – Walmart is 57% of the sales of the retailers shown. While slowing and facing declining estimates it has held up better. Walmart has a history of holding up relatively well during recessions as consumers trade down to it.

3. Volatile categories – The two categories up the most were motor vehicles and building supplies. Both are excluded from the core retail sales due to volatility.

4. Pent up demand for vehicles – Vehicles have significant pent up demand from supply chain issues in 2021 and 2022. You may recall the dealers couldn’t keep cars on their lots and were often charging above list price. That is something I have never seen before at that scale.

5. Smallish sample – The retailers analyzed in this report are only about 15% of total retail spending in the U.S. Whole sectors such as online (Amazon, Chewy, Shopify), gas stations and auto parts are not included. Fifteen percent is large enough to be a good indicator but is far from complete.

Retail sales are still growing, though now below the rate of inflation. That means retail volume is declining slightly. Retail sales are dropping more in certain areas such as apparel, big box, and discounters and less in building supplies, autos, and beauty. Also, retail sales have a history of holding up in non-discretionary categories such as food and gasoline. Neither of those were included in the 21 retailer sample.

Why May’s Earnings Estimates Decline Probably Isn’t A Blip

There are a number of headwinds coming together indicating this retail slowdown is not temporary. These are listed below.

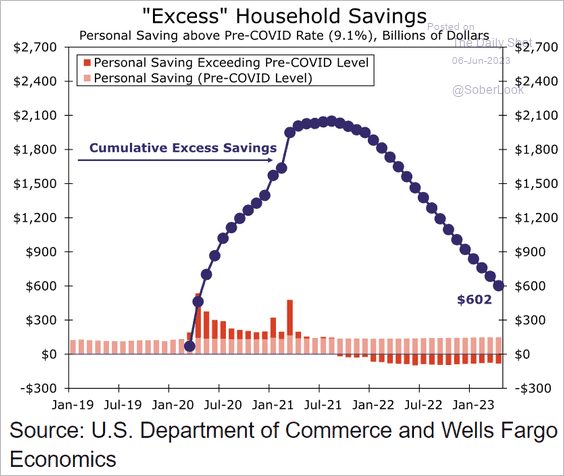

1. Excess Household Savings Draining Away

Retail sales have been supported by 4 huge stimulus packages in 2020 and 2021 totaling $5 trillion that left consumers with unprecedented excess cash to spend. The chart below is one of many that shows the surplus is mostly gone. This stimulus also pulled forward demand. Pulled forward demand is the opposite of pent up demand and both are very powerful. Pent up demand is so powerful it has been the primary factor getting us out of almost every recession. Consumer spending has remained relatively strong and even spiked in January of this year. But people need only so many pools and pizza ovens and mom jeans and are rapidly depleting the free money they got from the government.

U.S. Department of Commerce and Wells Fargo

2. Student loan repayment

According to studentaid.gov “Student loan interest will resume starting on September 1, 2023, and payments will be due starting in October.” This will significantly reduce money available to spend for tens of millions of people. These tend to be younger people who need the money more.

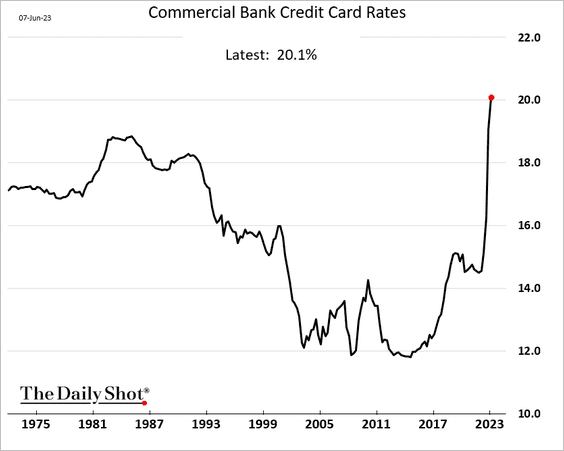

3. Interest Rates are Still Climbing

This is particularly the case with short term adjustable rates such as for credit cards. Credit cards are the largest payment method for consumers at retailers.

The Daily Shot

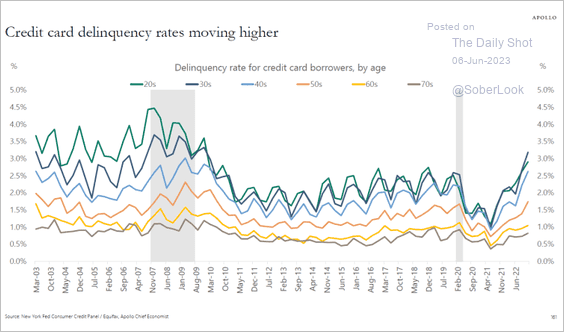

4. Credit Card Delinquencies Rapidly Rising

This has a negative impact on consumer spending at retailers in two ways. First it causes lenders to tighten credit, resulting in less new credit cards and lower limits. It also results in less people able to use their cards once they become delinquent.

Torsten Slok, Apollo

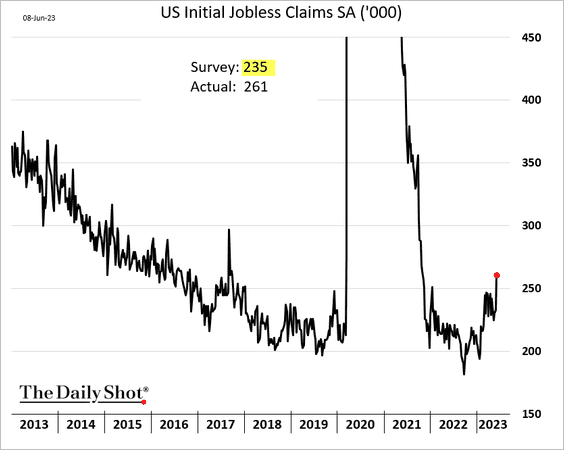

5. Layoffs are Picking Up

The strong labor market along with the massive stimulus have been the two factors most responsible for retail strength the past 2 years. However, the Fed’s interest rate increases are starting to have an impact on labor. It is still early but the trend shows increased jobless claims and less jobs available.

The Daily Shot

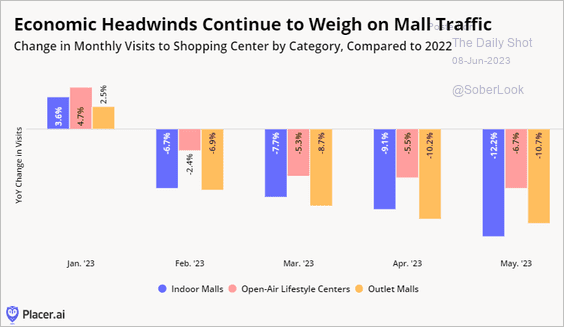

6. Mall Visits Are down

Malls still account for a large portion of retail spending. After years of slow decline, they had a resurgence in 2021 and 2022 due to the stimulus and pent up demand. But that appears to have ended.

Placer.ai

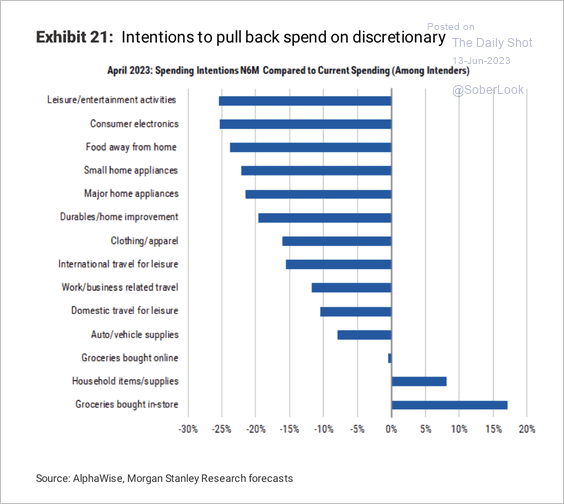

7. Consumers Expect To Spend Less

This recent Morgan Stanley survey shows a significant drop in spending intentions by consumers.

Morgan Stanley, Alphawise

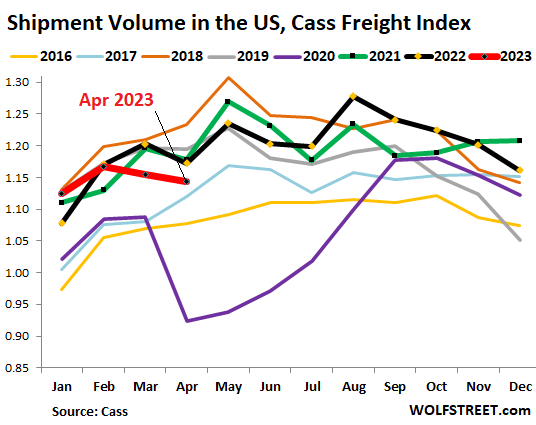

8. Trucking Volumes Are Falling Rapidly

Truck pricing and volumes have been dropping and are now well below that of 2022. Best of breed Old Dominion (ODFL) reported a 15.7% drop in revenue in May on 11.4% less volume. ArcBest (ARCB) reported a 10% drop.

Cass & Wolfstreet.com

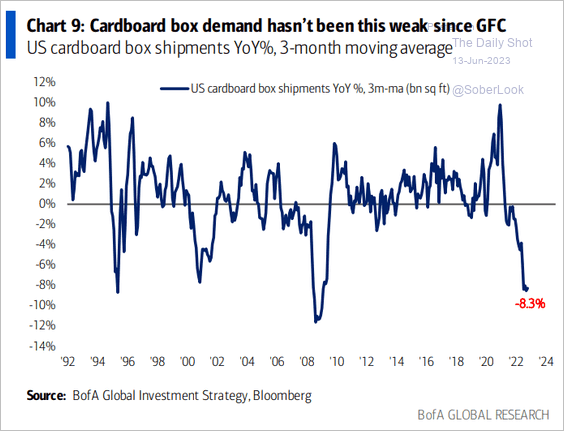

9. Cardboard Box Demand Is Dropping Fast

Outside of shipping and the consumer spending figures themselves, there may be no better indication of consumer spending than cardboard box demand. Most of it is used for consumer goods. The chart below shows it now down close to 2007-2009 recession levels.

Bank of America

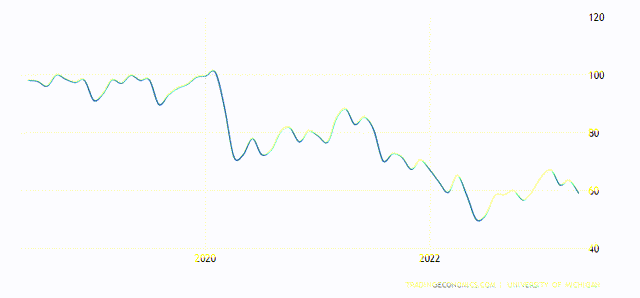

10. Consumer Sentiment is Dropping

Consumer sentiment as measured by the University of Michigan survey is dropping again after rallying late last year.

University of Michigan

11. Chinese Exports Dropped

Chinese exports dropped 7.5% YoY in May versus a 0.4% drop consensus. This was the first decline in 3 months. So, a sudden decline just like U.S. retailers saw. China’s largest export market is still the U.S.

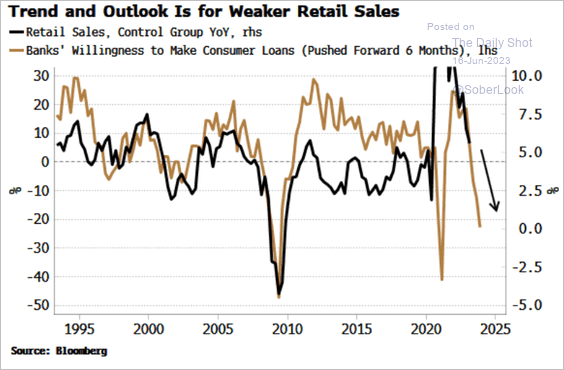

12. Tighter Credit Conditions

The chart below shows there has been a significant correlation between retail sales and banks willingness to lend. The failure of 4 banks earlier this year and expectation of a recession will likely make banks less inclined to lend in the intermediate term.

Bloomberg

13. Peak Pricing Power

This one is somewhat complex but may be the most important headwind along with the depletion of stimulus money. In 2021 and 2022 there were massive supply chain shortages while demand spiked from the stimulus and pent up demand. That led to major inflation. Retailers used the inflation and surge in demand as an opportunity to raise prices above cost increases. They have enjoyed historically high profit margins. However, it is increasingly clear consumers are now resisting price increases by buying less. There is only so long the strong stimulus induced profit margins can last. DICK’S (DKS) is a prime example of this as their profit margins last year were triple their long time historical rate. I wrote an article in January titled Dick’s Margins Are Unsustainable: Air Pocket Ahead. The primary causes of the industry profit margin jump (stimulus, pent up demand, and supply chain disruption) are mostly gone now. That means less pricing power going forward.

14. Labor Costs

Labor inflation is usually the stickiest inflation and this time is no different. As pricing power gets reduced, margins will get further squeezed as labor costs continue to rise faster than retailers can raise prices.

Tailwinds for Retailers

There’s always winds blowing both ways but I am having a hard time finding catalysts for retailers in this environment. One would be the wealth effect from the strong stock market this year. But that is primarily for wealthier people. There are always exciting new products coming out. Freight costs are declining, which should reduce operating expenses. If the Fed were to suddenly start lowering interest rates rapidly it would help, with a lag. There are pockets of strength such as new vehicles which are benefitting from pent up demand.

Takeaway

Retail sales by any measure are slowing and now appear to be below the rate of inflation. That means retail volumes are actually shrinking. I believe there are too many headwinds for retail right now for a sustained rebound and things will get worse. The most important headwinds are pulled forward demand in 2021 and 2022, fading consumer surpluses from the stimulus, and unsustainable margins.

The trend is more important right now than the growth percentages. Certain areas of retail that normally get hit first going into a recession (apparel, and big box) are already taking heavy hits to earnings estimates. The canary in the coal mine is chirping.

In my article titled 20 Reasons A U.S. Recession Is Coming Soon And 10 Reasons It Isn’t dated March 10, 2023, I concluded at that time the economy was primarily being supported by consumer spending.

Considering that consumer spending is 70% of U.S. GDP and retailers get the bulk of that, does this mean a recession is imminent? These numbers do not indicate we are in a recession yet but the cracks are clearly forming. Retail spending is now flat to slightly negative when accounting for inflation. There are other major parts of the economy that have been strong enough to make up for it. The service sector and labor market are still relatively strong though both are fading. They are having more and more difficulty driving the economy with manufacturing already in recession and retail rapidly weakening. It is likely we will enter a recession this summer.

At a minimum, there is a disconnect with the recently rallying stock market, both in retail stocks and the market as a whole.

How to Play it

Recessions almost always cause the Fed to cut interest rates. That means buying long term investment grade bonds should be quite profitable as their values go up.

Consider shorting the SPDR S&P Retail ETF (XRT) and stocks with unsustainable margins such as Dick’s. Dick’s has held up better than most but is unlikely to sustain a profit margin 3X long time historical levels. Another short to consider is trucker Old Dominion. Old Dominion is the best of breed for truckers. But it trades at a trailing PE ratio of 27 despite announcing a 15.7% drop in revenue in May on 11.4% less volume. That means 4.3% of the drop was due to lower prices. Lower prices usually reduce pretax profits almost dollar for dollar. A PE ratio that high with rapidly declining sales makes little sense.

Read the full article here