Investment Overview

Cass Information Systems (NASDAQ:CASS) is a proven high-quality company that consistently grows revenue and has maintained net margins above 17% for over a decade. The company has built a solid moat in the areas of payment processing and auditing of freight/cargo. Although exponential returns are not likely, new data service offerings are likely to generate continued growth for CASS in the coming years.

Company Overview

Cass Information Systems specializes in providing payment and information management solutions to businesses in a variety of industries. The company provides a variety of services to assist businesses in streamlining their payment processes, managing their expenses, and enhancing their financial visibility.

CASS focuses predominantly on three key areas: freight invoice payment and auditing, utility invoice payment and information management, and telecom expense management.

In the freight invoice payment and audit segment, CASS assists businesses in accurately and efficiently processing and paying their freight invoices. They use advanced technology and automated systems to verify the veracity of invoices, identify discrepancies or errors, and ensure carriers are paid on time.

In the sector of utility invoice payment and information administration, CASS offers solutions to simplify and centralize the utility bill payment process. They assist businesses in consolidating and validating utility bills, tracking energy consumption, and generating comprehensive reports and analytics.

CASS also offers telecom expense management services, which include invoice consolidation and analysis. They aid businesses in managing telecom costs, identifying invoicing errors or unauthorized charges, optimizing service plans, and enhancing telecom cost management overall.

Through its comprehensive payment and information management solutions, Cass Information Systems seeks to enhance the financial operations of businesses, increase their efficacy, and reduce their expenses. Their services assist businesses in gaining greater control over their payment processes, ensuring accurate and timely payments, and gaining valuable insights from their financial data.

Overview of Key Product & Service Lines

The primary service offerings of CASS include the following areas.

Payment and Audit of Freight Invoices: CASS offers solutions to expedite the payment process for freight invoices. This includes invoice validation, auditing, and processing, ensuring that carriers are paid accurately and on time. They use dedicated technology and automated systems to detect errors, discrepancies, and overcharges, thereby assisting businesses in lowering costs and enhancing transportation management.

Payment and Information Management for Utility Invoices: CASS assists businesses in effectively administering their utility invoices. They provide solutions for consolidating, validating, and processing utility bills, as well as monitoring, reporting, and analytics for energy consumption. This assists organizations in gaining greater control over utility expenses, identifying opportunities for cost savings, and streamlining payment processes.

Telecom Expense Management: CASS provides services to optimize telecom expense management. They provide solutions for consolidating and analyzing telecom invoices, identifying billing errors and discrepancies, administering service plans, and optimizing telecom costs. This facilitates cost control, the elimination of unauthorized charges, and efficient administration of telecom services for businesses.

Healthcare Payment Solutions: is a service provided by CASS for the healthcare industry. They offer comprehensive payment processing services, including solutions for medical invoices and reimbursement, revenue cycle management, and electronic payment options. These solutions aid in streamlining payment processes, enhancing cash flow, and enhancing overall financial management for healthcare providers.

Information Management and Reporting: CASS provides tools and platforms for centralizing and managing information pertaining to payments. Their reporting and analytics capabilities provide businesses with valuable insights into payment data, enabling them to make informed decisions, recognize trends, and monitor key performance indicators.

Finally, CASS also provides managed services to handle diverse payment-related duties on behalf of businesses. This includes the processing of invoices, payment reconciliation, vendor administration, and handling of exceptions. By outsourcing these functions to CASS, businesses can reduce administrative burdens and concentrate on their essential operations.

Strategic Investment Case & Competitive Advantages

CASS is one of those classic boring businesses that is providing a ton of value to its customers. While services like freight invoicing, auditing and information management for utilities may not be the hottest growth areas, they are a necessary evil for companies with global supply chain and customer exposure. CASS has carved out a niche by doing the “dirty work” for its customers.

In recent years, CASS has ramped up its effort as a data gatherer and data manager. In many cases, CASS is collecting hard-to-obtain data and then processing the information for customers to recommend actionable savings and efficiencies opportunities. This is a winning combination. CASS’s customers benefit from the savings, while CASS’s own database grows more robust with unique data points that can lead to further recommendations down the road.

With CASS having operated in this space for over 100, the company has built long-standing customer relationships which are difficult for competitors to penetrate. CASS has detailed knowledge of some of the most complex areas of its customers’ operations. This level of trust and insight would not be easy for competitors to replicate. Additionally, CASS has built thorough domain expertise in the processing and information management spaces, particularly as it relates to the transportation, energy, healthcare and utilities sectors. Having a deep understanding of industry specific challenges allows CASS to develop customized solutions its clients.

CASS’ focus on passing along efficiencies to its customers is another source of competitive advantage. By leveraging CASS’s solutions, customers can identify billing errors, reduce overcharges, eliminate duplicate payment and streamline workflows. All of this results in less administrative burdens and significant cost savings.

The company has also committed to moving toward more advanced technologies, systems and software in the coming years. Based on its operating history, we believe this will result in further upside for both CASS and the company’s customers. Additional automation and more advanced data collection should result in higher revenue/profits for CASS.

Investment Risks & Watch Areas

In this writer’s view, there are 2 core areas of risk for potential investors to consider. From a competitive standpoint, potential investors need to consider the possibility the new competitors could come along with significantly more advanced technologies including leveraging AI, Blockchain or Internet of Things based solutions to greatly automate and simplify many of the functions provided by CASS. As discussed above, CASS is moving towards implementing more advanced technologies, but many of its processes still included manual components. If new competitors arise with more advanced systems, this could be highly disruptive to CASS’ business model and result in a significant loss of revenue. Nothing appears to be imminent here, but potential investors need to keep this as a watch area given the disruption it could cause to CASS.

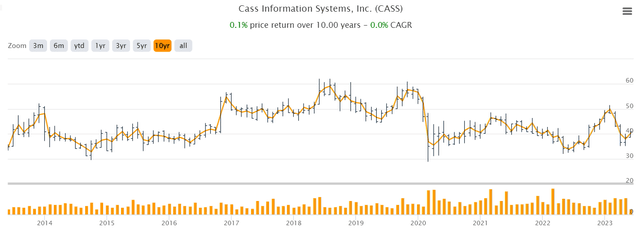

The other major consideration for potential investors is the lack of attention the company has historically received from both Wall Street and Main Street investors, despite the consistent growth the company has achieved. As evidenced by the company’s price chart below, CASS has largely traded within a range of $40 – $65 per share over the last 10 years. The company does not get a lot of attention from the street or the buy-side investment community. Although this is not necessarily a bad thing, it also does not appear that the company is getting credit for its consistent revenue and profit growth, as well as its strong margins. Potential investors need to be prepared to wait to see upside in the stock price. CASS likely will not be a quick grower with “pops” that spike the stock price. Luckily, the company currently pays a nearly 3% dividend and hasn’t missed a dividend payment in over 100 years.

TIKR

Financial Overview

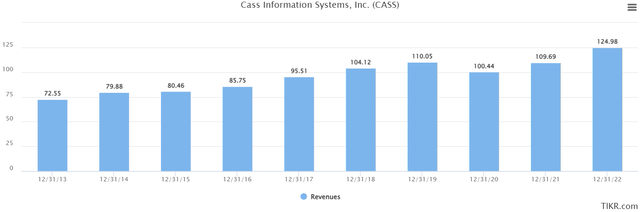

If you’re a fan of consistent growth and profitability, then CASS is a stock you’ll likely want to consider. As shown in the chart below, CASS’ revenue has been on a steady upward trend over the last 10 years.

TIKR

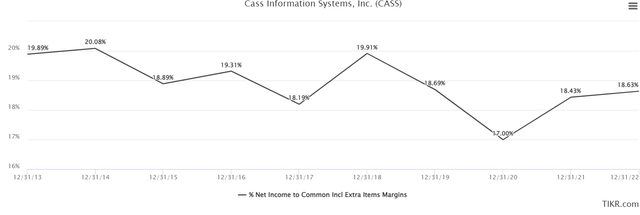

Meanwhile, net margins have also been remarkably consistent over the last decade, coming in at the 18-20% range in any given year. Although it’s tough to beat a 20% net margin, it will be interesting to see if CASS can pick up a few percentage points over the next 3-5 years if the company is successful at automating more of its solutions and further building out and selling its data sets. Over time, the company should achieve operating leverage in both areas.

TIKR

CASS is also a very shareholder-friendly company. Over the past decade, diluted share counts have decreased from 15.4M to 13.8M today. During this same time, dividends have increased from $0.56 per share to $1.13 per share in 2022, all while the payout ratio has consistently stayed below 55%.

On the balance sheet, CASS holds $201M of cash and has no debt. CASS is a company that operates leanly and seeks to maintain its financial health.

Meanwhile, we see further evidence of CASS’s operating strength thru its consistently strong performance in the Return on Capital metric. In fact, RoC hit its highest level over the past decade in 2022 at 21.5%.

TIKR

Although we view CASS primarily as a play for long-term investors, Q1 results support the overall investment thesis. Quarterly revenue clocked in at an all-time high of $52.2M, while overall share counts outstanding remained at 13.6M. If there’s a knock on the company’s performance, it’s that net margins dropped to 14% in the quarter. The primary driver of this increase was increased personnel costs due to annual merit increases, general wage inflation, other benefit increases and higher total employee counts from the Touchpoint acquisition. Management expects to absorb these higher costs over time, but we would note this as a watch area for potential investors.

Outlook

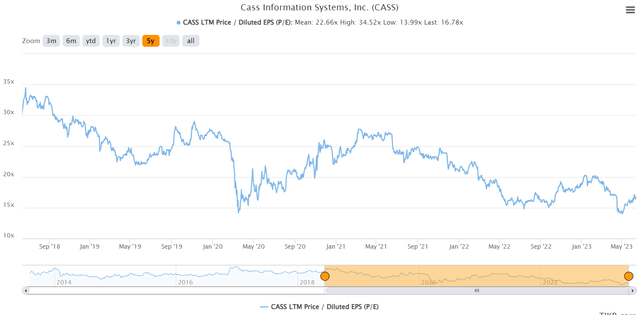

CASS does not have any coverage from Wall Street analysts. That said, CASS has weathered a lot of storms over the past 100 years and continues to consistently grow. Over the next 2 years, potential investors can conservatively model in 8% revenue growth and 18.5% net margins. If the company hits these targets, CASS would have $218M of revenue and $40M of net profit in 2024. At these levels, CASS today is trading at just 14.0x 2024 earnings. CASS appears to be well into value territory, considering the company’s historical P/E as shown below.

TIKR

The bear case for CASS would likely be the onset of either a US or global recession, despite the fact that several of the company’s lines of business are relatively recession resistant. Given the lack of publicity around CASS, during a recession, the company will likely experience similar selling pressure to the overall market. However, given CASS’s consistent historical performance, this scenario would ultimately be a buying opportunity for long-term investors.

Overall, CASS exhibits many of the hallmarks of a high-quality company – including a focus on long-term performance, a commitment to shareholder returns, a dedicated focus on its customers, strong financials and a demonstrated ability to execute operationally. For investors with a 3+ year time horizon, we’re assigning CASS a buy rating.

Read the full article here