Solar stocks continue to be out of favor. The relative strength of the Invesco Solar ETF (TAN) is near its lowest level since March of 2022. That comes as a semiconductor boom takes off amid AI mania. Perhaps playing a bigger role in soft performances among solar energy-related names is the downright dreadful 1-year returns in the oil patch. WTI crude oil is typically seen as a substitute for solar energy, so lower oil can drag down TAN’s constituents.

I have a buy rating on Enphase Energy (NASDAQ:ENPH), the biggest holding in the TAN ETF. The valuation is not all that stretched following a nearly 50% current drawdown while technicals suggest a continued downtrend could linger as we venture closer to its July earnings date. The long-term growth trajectory for both Enphase and the industry remains decent.

Solar Stocks Losing Their Luster Versus the S&P 500

Stockcharts.com

According to Bank of America Global Research, ENPH sells micro-inverters, energy storage, and software solutions catered to residential (rooftop) solar applications. The company offers a semiconductor-based microinverter, which converts energy at the individual solar module level and combines with its proprietary networking and software technologies to provide energy monitoring and control services.

The California-based $24.9 billion market cap Semiconductor Materials & Equipment industry company within the Information Technology sector trades at a high 53.5 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

Enphase plunged following its Q1 earnings report and, more importantly, its outlook. There certainly wasn’t any sunshine amid its sales warning – the forecast brought down much of the industry. Contrasting that dour prognostication, the broader space reportedly had its biggest first-quarter growth ever, according to a report issued by Wood Mackenzie and the Solar Energy Industries Association. The Wood Mack report noted that utility-scale project demand surged 66% on an annual basis as a relaxed supply chain situation benefits the solar equipment firms.

As the Inflation Reduction Act’s impact makes headway, the total domestic solar market is seen as doubling in the five years. But getting back to the bleak guidance offered by ENPH in April, a key risk is clearly the ‘higher for longer’ interest rate environment. Indebted firms that have to refinance at higher borrowing levels is problematic should near-term revenue growth ease. I assert much of the pessimism is baked in considering the solid long-term industry expansion trend. Today’s 16x 2024 EBITDA forecast is a more reasonable valuation compared to where the stock sold for in late 2022.

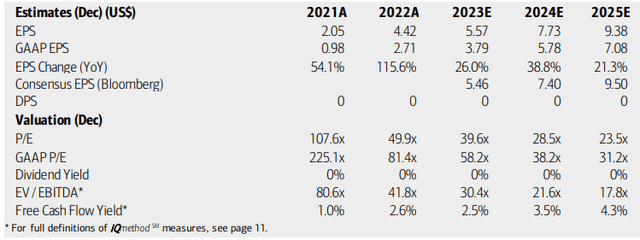

On valuation, analysts at BofA see earnings climbing sharply this year as per-share profits are expected to top $5 while out-year EPS could threaten $8 in a bullish scenario. Continued 20%-plus bottom-line growth is then seen in 2025. This growth stock is not expected to have dividends any time soon. While the firm is free cash flow positive and the firm has shown itself to be a FCF machine in the face of industry volatility, both its earnings multiples and the EV/EBITDA ratio are high, on the surface, compared to the broad market.

Enphase: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

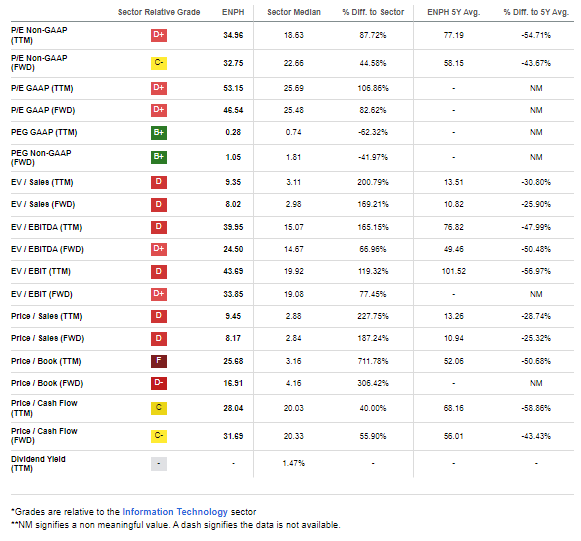

Amid an uncertain fundamental backdrop but earnings that are still expected to hold up, I see value in the stock. Consider that Enphase’s forward PEG is just 1.05. That growth-adjusted valuation figure is exceptional now that shares have fallen so hard from the $340 peak. Even if we discount the fair forward operating P/E to just 35 and assume next-12-month EPS of $6, then the stock should be near $210. That valuation could be conservative if robust profit outlooks verify over the ensuing quarters.

Enphase: Favorable Valuation Relative to High Earnings Growth

Seeking Alpha

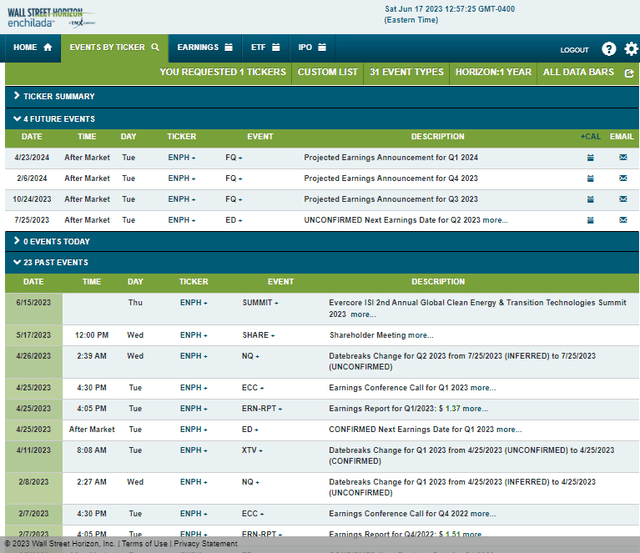

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Tuesday, July 25 AMC. The calendar is light on volatility catalysts aside from next month’s quarterly report.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

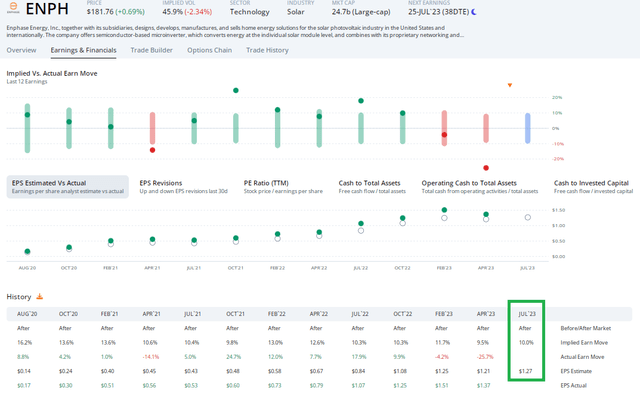

Looking forward to the July earnings release, data from Option Research & Technology Service (ORATS) show a consensus EPS forecast of $1.27 which would be a 19% rise from $1.07 of per-share profits from the same quarter a year ago. After the 26% post-earnings plunge in April, a 10% earnings-related stock price swing is currently priced in when analyzing the at-the-money straddle expiring soonest after the reporting date.

With a stellar bottom-line beat rate, Enphase has a lot to live up to. Another dire revenue outlook could be the death knell for bulls left standing. Overall, the options actually appear somewhat cheap to me given that the stock’s implied volatility is more than three times that of the S&P 500.

ENPH: Options Not All That Expensive Considering Its Long-Run High-Volatility Trend

ENPH: Options Not All That Expensive Considering Its Long-Run Volatility Trend

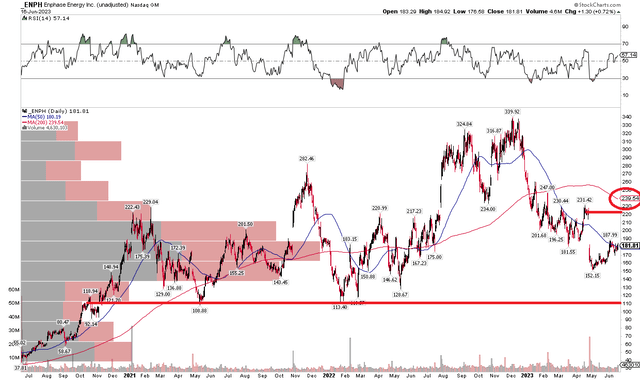

The Technical Take

While I like the valuation landscape following the stock price decline in the last 6 months, the chart is concerning. The bulls must pay attention to a clear downtrend. I see support near $120 should the April low of $152 fail to hold. On the upside, I spot a gap that may be filled near the $220 mark. Furthermore, before long, the declining 200-day moving average should come into play around that same level.

A downwardly sloped 200-day also implied that the bears are in charge, so stepping in with a long position here should be done with prudence. I suggest buying in increments should bearish momentum persist. Purchasing the stock with a long-term holding period under $150 should prove to be a solid investment.

Overall, the technicals underscore the need for prudent risk management right now.

ENPH: Eyeing An Upside Gap To Fill, But Risk To Near $120 Is In Play

ENPH: Eyeing An Upside Gap To Fill, But Risk To Near $120 Is In Play

The Bottom Line

I have a buy rating on Enphase Energy but acknowledge that the situation with momentum is precarious. Long-term investors should consider purchasing lots slowly assuming the bearish technical trend continues, but I am bullish on ENPH’s long-term growth prospects.

Read the full article here