Thesis

The FlexShares High Yield Value-Scored Bond Index Fund (NYSEARCA:HYGV) is an exchange traded fund. The vehicle focuses on the U.S. high yield space. Just like the iShares High Yield Bond Factor ETF (HYDB) which we covered recently, this fund follows an Index which tries to identify via factoring a subset of high yield bonds with better risk/return profiles. As per its literature:

The Fund seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of the Northern Trust High Yield Value-Scored US Corporate Bond Index® (Underlying Index).

The index optimizes the utilized high yield bond population based on their exposure to quantitative factors such as a value-score, a credit-score, and a liquidity score. These are determined by Index’s quant team based on proprietary scoring models. In addition to that objective, systematic risk is managed during the optimization through the use of several constraints. The end game here is to outperform the wider high yield indices as reflected by widely used ETFs such as the SPDR Bloomberg High Yield Bond ETF (JNK) and the iShares iBoxx $ High Yield Corporate Bond ETF (HYG).

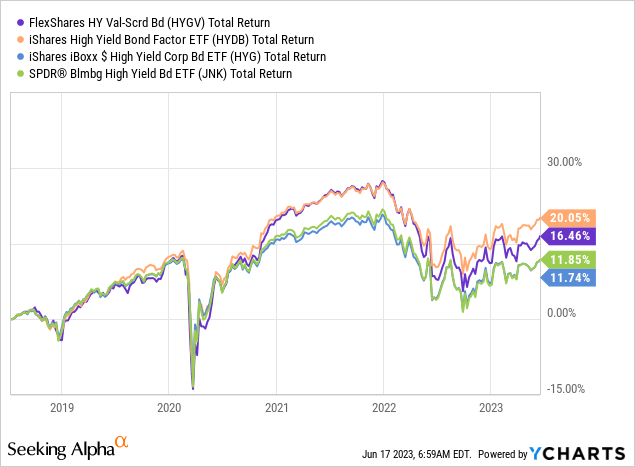

The fund is successful at achieving its goals:

We can see the fund outperforming the wider market in HY as expressed in JNK and HYG, but the vehicle underperforms HYDB, a fund from BlackRock that also tries to identify smart beta names in the space.

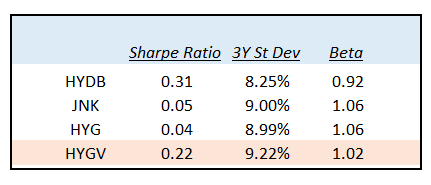

Furthermore, if we look at the holdings and analytics for HYGV we will notice the fund takes more credit risk than its peers and exposes a higher volatility:

Analytics (Author)

HYGV has the highest standard deviation from the analyzed cohort, making it the most volatile name here. Its beta is also high when compared to HYDB as an example. We have established the fund takes additional credit risk (please see details in the Holdings section), but to a certain extent it is well compensated risk – the fund’s Sharpe ratio is still higher than the general JNK and HYG funds. As a reminder, the Sharpe ratio is the correct tool to understand whether risk is well compensated. You might have instances in the high yield universe where credits are rated ‘CCC’ but they have a 100% recovery (some companies with hard assets for example), so even if they default you would get back your full principal. Such an asset is preferable to a ‘CCC’ name with a 40% recovery, for example (all else equal).

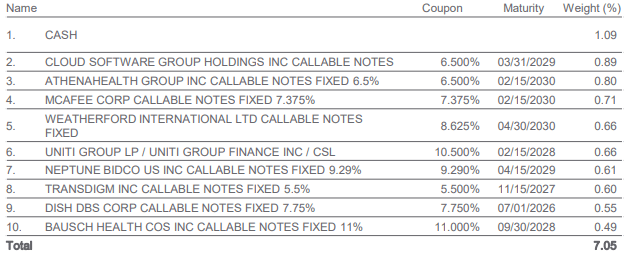

Holdings

The fund has a granular build and holds U.S. high yield credits:

Individual Names (Fund Fact Sheet)

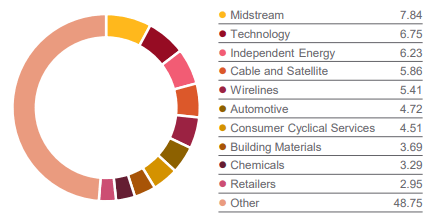

The fund does not take any excessive risk via its sectoral build:

Sectors (Fund Fact Sheet)

We can see the Midstream energy sector being the largest fund holding here, followed by Technology and Independent Energy companies.

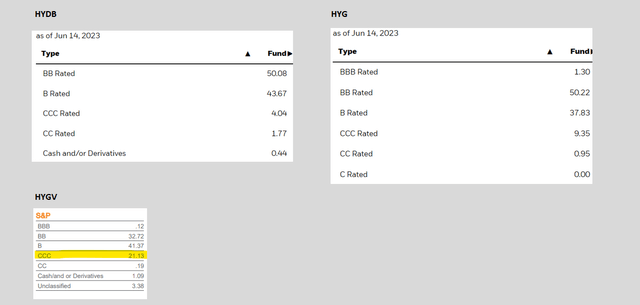

However, when compared to some of its peers in the comparison cohort, the fund does take additional credit risk:

Credit Risk (Author / Fund Websites)

We can see the fund having a very high ‘CCC’ bucket, which sits at over 21% of the fund. That is a very high number and explains the higher standard deviation observed in this name. While it has historically outperformed, the fund is subject to higher risk from an increase in default rates via its ‘CCC’ bucket.

Optimization of the High Yield Universe

The optimization of the utilized high yield population is a valiant concept, and inherently actively managed funds do perform that function (both CEFs and ETFs). The utilization of a constructed Index just puts a systematic framework around this concept, and allows the increase in AUM by attracting investors based on a systematic, transparent methodology, rather than reliance on individuals and their trading acumen.

Conclusion

HYGV is a fixed income exchange traded fund. The vehicle focuses on the U.S. high yield universe, and represents a smart beta play on U.S. high yield. The fund follows an Index which employs proprietary value, credit, and liquidity scores to identify undervalued names. HYGV has been successful at outperforming the wider market (as reflected by JNK and HYG), but has underperformed another smart beta fund, namely HYDB. In addition, as opposed to HYDB, HYGV takes incremental credit risk to achieve its outperformance. The fund has a very large ‘CCC’ bucket, which currently clocks in at over 21% of the fund. This feature is a concern, especially in light of increasing defaults. HYGV is a decent smart beta play when compared to JNK and HYG, but is not the golden standard in the space. We feel the market has been very complacent about risk as of late, with very tight credit spreads, VIX levels and a general feeling of euphoria. We are of the view of Selling this name waiting for a market correction, and then entering into HYDB.

Read the full article here