While I would love it if every investment prospect that I looked upon favorably immediately increased in price, that’s unfortunately not how the world works. Sometimes, it can take a long time in order for a prospect to really pay off. And in that time frame, shares can do everything from remain flat, to rise by underperforming the market, or even to drop some. One company that has definitely underperformed my expectations over the past several months has been ACCO Brands (NYSE:ACCO). The enterprise owns a variety of school and office material brands such as Five Star and Mead. Recently, revenue, profits, and cash flows for the company have shown weakness on a year over year basis. This has sent the stock dropping at a time when the broader market has moved higher. But even with these declines, shares of the company look fundamentally cheap and likely offer attractive upside from here. It’s because of this that I have decided to keep the ‘buy’ rating I had on the stock previously.

Weakness continues

Back when I last wrote about ACCO Brands in a bullish article that I published in September of 2022, I acknowledged that profits for the company were on the decline. Overall financial performance, in fact, had been rather mixed leading up to that point. But despite this and despite concerns about the economy more broadly, shares of the company looked too cheap to ignore. Although I never bought shares of the business, I did keep it rated a ‘buy’ to reflect my view at that time that the stock should outperform the broader market over a long enough period of time. Unfortunately, that is not what has happened so far. While the S&P 500 has jumped 17.3% since the publication of that article, shares of ACCO Brands have seen a downside of 0.5%.

Author – SEC EDGAR Data

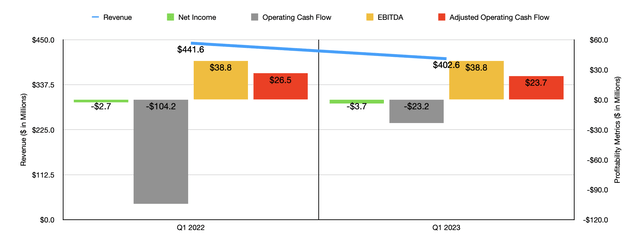

This pain, in my opinion, can really be chalked up to continued fundamental weakness for the company. Consider the most recent data that covers the first quarter of the firm’s 2023 fiscal year. Sales for this time came in at $402.6 million. That’s 8.8% below the $441.6 million reported one year earlier. Two of the company’s three operating segments were entirely responsible for this pain. The ACCO Brands North America segment, for instance, saw revenue plummet 15.3% despite a 4.2% contribution from price increases on the company’s products. However, a weak macroeconomic environment, as well as reduced back to school purchases by retailers and lower demand for technology accessories, all more than offset this in the form of volume declines. The same factors, combined with a 5.7% hit associated with foreign currency fluctuations, pushed sales down for the ACCO Brands EMEA (Europe, Middle East, and Africa) segment by 13% year over year. The only bright spot for the company was the rather small ACCO Brands International segment. Revenue there spiked 17% from $77 million to $90.1 million, with price increases accounting for 12.6% of the move higher and volume growth adding 4.7% thanks to strong demand from both Mexico and Brazil.

This drop in revenue brought with it a decline in profitability. The firm’s net loss, for instance, went from $2.7 million in the first quarter of 2022 to $3.7 million the same time this year. It is true that operating cash flow improved from negative $104.2 million to negative $23.2 million. But if we adjust for changes in working capital, we would actually see this number decline from $26.5 million to $23.7 million. And finally, we have EBITDA. It’s the only profitability metric that remained stable during this time, flatlining at $38.8 million to match the company reported for the same time last year.

Author – SEC EDGAR Data

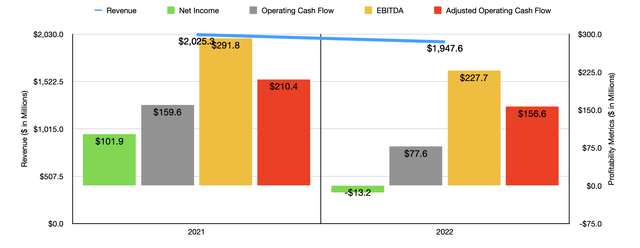

As you can see in the chart above, the first quarter of the 2023 fiscal year was not the only time the company experienced weakness. 2022 was worse than 2021 in every respect as price increases were not enough to offset reduced volumes shipped. For the current fiscal year, management does expect a little bit of improvement on the bottom line. Comparable sales are expected to be flat at best and down 3% at worst. However, adjusted earnings per share should come in at between $1.08 and $1.12. At the midpoint, that would translate to net income, on an adjusted basis, of $104.4 million. That would compare favorably to the $101 million reported for 2022. If we assume that other profitability metrics will rise at the same rate that adjusted earnings should, we would anticipate adjusted operating cash flow of $161.9 million and EBITDA of $235.4 million for the current fiscal year.

Author – SEC EDGAR Data

Based on these forward estimates, shares of the company look incredibly cheap. As you can see in the chart above, the firm is trading at a forward price to earnings multiple of 4.6. The forward price to adjusted operating cash flow multiple is even lower at 3, while the EV to EBITDA multiple comes in at 6.1. Even if we assume that financial performance were to match with the company saw in 2022, shares would still be very cheap as the chart illustrates. One thing that investors do have a legitimate complaint about and that could justify some discount on the stock is the fact that the business does have a good deal of leverage. It has net debt of $964.3 million. That translates to a net leverage ratio of 4.23 if we use the data from 2022. Ideally, management will use cash flow to pay this down this year. But for as long as it is elevated, it does deserve to trade at some discount relative to similar firms. However, the discount to me seems to be too extreme. In the table below, you can see how shares are priced relative to five companies that have some similarities to it. On both the price to earnings basis and the price to operating cash flow basis, ACCO Brands ended up being the cheapest of the group. And when it comes to the EV to EBITDA approach, only one of the five companies was cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| ACCO Brands | 4.8 | 3.1 | 6.3 |

| NL Industries (NL) | 35.1 | 9.3 | 9.4 |

| MSA Safety (MSA) | 29.0 | 33.1 | 32.7 |

| HNI Corporation (HNI) | 9.9 | 8.0 | 5.8 |

| Interface (TILE) | 90.6 | 5.3 | 9.0 |

| Steelcase (SCS) | 25.0 | 9.6 | 7.2 |

Takeaway

I don’t like seeing a company report declining sales, profits, and cash flows. I especially don’t like to see this when the company has a good deal of leverage. But at some point, shares become too cheap to ignore. In my view, that’s the kind of situation we are dealing with today. Management is already forecasting some degree of stability for the current fiscal year, with the worst case scenario being a modest decline in revenue relative to what was seen in 2022. So long as the pain does not worsen from that point, I have no reason to be anything other than optimistic about the company’s potential. Given this, I’ve decided to keep the ‘buy’ rating I had on the stock previously.

Read the full article here