The latest stock market buzzword making the rounds is the vaunted “melt-up”. The term has a long history in finance, generally describing an excessive outperformance of a security or entire asset class that appears to have become disconnected from fundamentals.

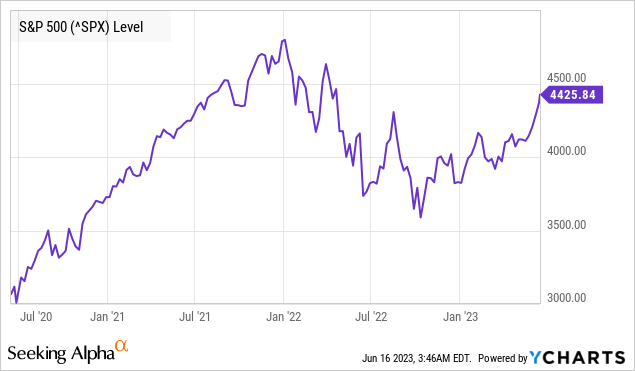

The implication is that the rally is unjustified, reminiscent of a bubble with investors chasing, and marks the final stage before a big selloff. Anyone calling the ongoing rally in the S&P 500 (SP500) a melt-up, following its 16% in 2023 thus far, can be described as at least skeptical of the trend or bearish at the current level, but also leaving the door open for more upside before a deeper melt-down.

Famed economist and market strategist Ed Yardeni has gone on record suggesting the current momentum in AI stocks may be setting up the “Mother of All Melt Ups”, a term he coined nearly a decade ago in 2013. Bank of America (BAC) strategist Michael Hartnett shares a similar forecast, looking for a “big collapse” eventually.

We respect the opinions, but don’t agree and can point to several holes in that assessment. In our view, the stock market remains on firm footing and investors should expect more positive returns from here with no crash in sight. As it relates to the S&P 500, we see a path into a new all-time high leading into a longer multi-year bull market.

The Melt Up Narrative is Smoke and Mirrors

The main problem we have with the melt up angle is that it says nothing about the upside potential or downside target. The NASDAQ 100 (QQQ), for example, could “crash” by -10% tomorrow, and it would just go back to a level it traded at two weeks ago and still be up over the past month. Anyone that has been bearish for longer is going to need an even bigger move lower to have their prophecy fulfilled.

Another issue is that a melt up sounds a lot like playing both sides of the same coin. What we mean by this is that strategists suggesting a melt up as central to an investment outlook are going to be right regardless of what transpires going forward.

If the S&P 500 runs to $4,999 through the year-end, the melt up camp will point to it being a continuation of the same “irrationality”. Inversely, if the market sells off from here, the group can claim they told you so. Start planning that victory parade, but we don’t see the alpha in that narrative.

A blanket statement that “the market is set to crumble; just not yet!” is a thin argument in our opinion. An improvement to that would be to set a clear price target with a plan to trim exposure, rotate defensively or into a different sectors etc. As wrong as perma-bears have been over the past year, we can at least admire their commitment to calling for a selloff at every turn as a actionable idea. A melt up is more hype than anything.

Don’t Hold Your Breath Looking For “The Top”

The bigger point is that there is nothing to suggest the current rally in stocks will end with a major market turning point that will be in place for several years. Stocks go up and down, and there are ranges of expected volatility and downside risk that are completely normal over any timeframe.

Our sense is that most investors would be content riding out a -5% selloff, with an understanding that such a move could simply be a healthy consolidation of recent gains. That’s not the melt down which is supposed to follow a real melt up.

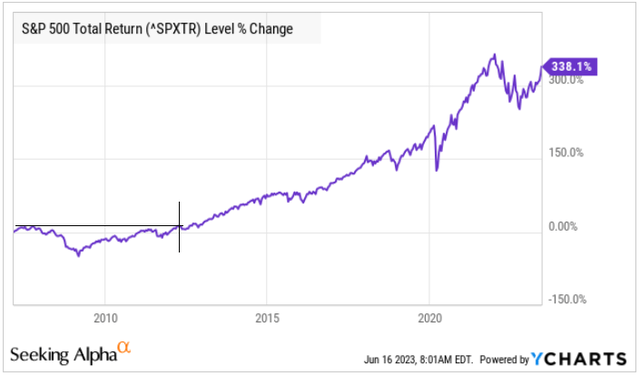

As a historical proxy, we see parallels to the current market backdrop to the action in 2013, when the S&P 500 finally emerged from the great financial crisis collapse to approach its first new high in more than five years.

There was widespread skepticism at the time that the global economy had regained a firm footing, and many felt the rally was unsustainable. Coincidently, the trading environment was also described as a melt up at the time, although the allusive crash never materialized. We’ll note the S&P 500 has gone on to return more than 330% in the period since.

source: yCharts

Improved Macro Fundamentals

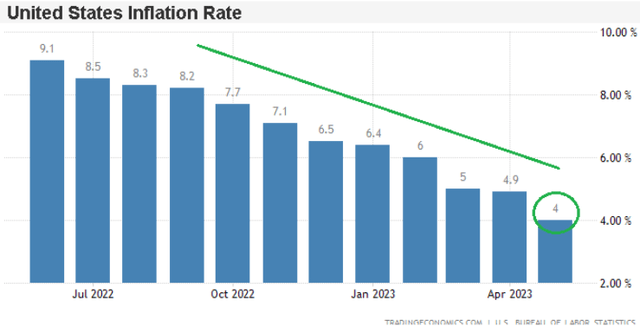

The connection to now is that the global economy is also on the verge of a rebound from what had been a post-pandemic hangover. Looking back, the majority of headwinds that defined 2022 being record inflation, supply chain disruptions, an energy shortage, and an aggressively hawkish Fed are all now dissipating.

Investors can look forward to 2024, which is coming up in just about six months with a backdrop where the CPI is trending toward 3%, while the labor market remains firm, alongside positive economic growth. Those estimates come from the official Fed economic projections. We can argue about the potential for a tick higher in rates from here and recognize ongoing risks, but the setup has clearly evolved better than many expected compared to the depths of last year.

source: tradingeconomics

Companies should be benefiting from the improved operating environment where profit margins can expand going forward, driving new earnings momentum. Separately, the advantage of interests rates sitting above 5% right now is that the Fed has room to support financial conditions with cuts down the line if necessary.

So the biggest weakness we see with the melt up narrative is that it sort of dismisses what has been a real improvement in the macro fundamentals that has helped justified the recovery from the lows of 2022.

Keep in mind that the S&P 500 and even NASDAQ are still well below their all-time highs. The argument we make is that the long-term investing outlook for equities may be stronger than ever, particularly with new tailwinds being the opportunities in AI that are expected to drive business productivity as a secular theme going forward.

If anyone is looking for a “blow off top” (the melt up’s close cousin) as a catalyst for a meaningful correction, we’d expect that to occur with the indexes in uncharted territory, which is not the case.

Valuations Are Attractive

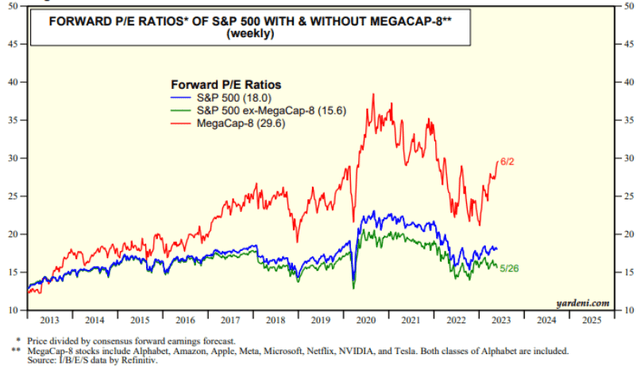

A theme thus far in 2023 that has raised eyebrows is the significant outperformance of mega-cap tech leaders, particularly those connected to artificial intelligence. Stocks like NVIDIA Corp (NVDA), Microsoft Corp (MSFT), Alphabet Inc (GOOGL), and Meta Platforms Inc (META) have represented a large part of the market gains given their overweight influence.

The chart below from Yardeni economics highlights this divergence, where the “megacap-8” as a group are trading at a 30x forward P/E multiple, well above the broader index level premium closer to 18x.

Here we can highlight how investors just focusing on those big stocks, like NVDA up 200% year to date, might miss out on the big picture that the rest of the market actually appears cheap. The same chart below shows that the S&P 500 excluding those particular stocks are at a very attractive 16x, which is below the average over the past decade.

source: Yardeni.com

While some may point to the “poor market breadth” as a sign of weakness, we believe it represents the opportunity, setting the stage for the next leg higher in the market.

The way we see it playing out is that many of the laggards which we can include 100s of small-caps outside the S&P 500 can lead higher going forward based on the improving macro setup with rebounding economic growth into next year.

In other words, even if the mega-cap names simply consolidate their recent gains and trade rangebound, the broader market still has a path to move higher in what could be described as a rotation from tech into more cyclical names across industrials, financials, and even commodity related industries.

A selloff in one of the key tech names for whatever reason could drive some renewed market wide volatility, but there’s nothing to suggest a pending market wide crash.

Final Thoughts

Nothing goes in a straight line, and the proverbial wall of worry will always add to headline risks. The main concern would be for a deterioration in the macro conditions that begins to undermine the outlook for easing inflation and stabilizing interest rates. In the near-term, upcoming CPI updates could introduce some volatility with the risk of a “hot” readout.

While unlikely based on the current data, a scenario where the U.S. and global economy slips into a deeper contraction would force a reassessment of any timetable for the S&P 500 to recover its all-time high. The situation in Eastern Europe is also a question mark.

That being said, there are plenty of reasons for investors to look up and stay the course. We touched on some of the improved macro fundamentals, but other factors including a weaker U.S. Dollar and even firming conditions across emerging markets and Europe are also positive for risk assets.

We can also point to cash on the sidelines and a dynamic where institutions need to rotate into equities for portfolio rebalancing. There is a clear shift in improved investor sentiment.

Overall, we see many opportunities as stock pickers, and it’s a great time to be invested, in our opinion. Our year-end price target for the S&P 500 has been recorded at $4,777, and we can re-affirm that view here today.

Read the full article here