When measured on a price to sales basis, the US Information Technology sector is now more overvalued relative to the broader US market than at any time since the very last few months of the tech bubble that ended in March 2000. Euphoria over the potential for Artificial Intelligence is driving the bubble, the same way the arrival of the internet drove the 1990s bubble. While there is potential for the tech sector to spike further if its December 2021 highs are taken out, note that the MSCI Information Technology index is still underwater relative to US bonds since its 2000 peak, despite seeing strong sales and earnings growth seen since then. I am short the Vanguard Information Technology ETF (NYSEARCA:VGT) as I see deeply negative long-term returns.

The VGT ETF

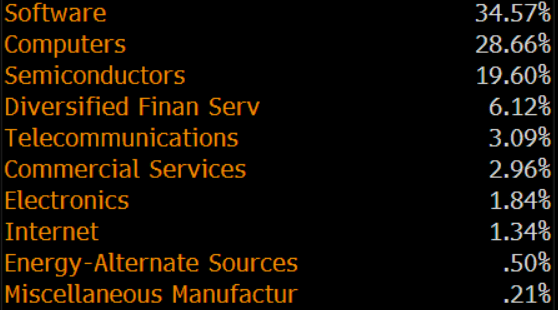

Vanguard Information Technology ETF seeks to track the investment performance of the MSCI US Investable Market Information Technology 25/50 Index, an index of stocks of large, medium-size, and small U.S. companies in the information technology sector, as classified under the Global Industry Classification Standard (GICS). This GICS sector is made up of companies in the following three general areas: internet services and infrastructure companies, including data centers and cloud networking and storage infrastructure; companies that provide information technology consulting and services, technology hardware and equipment, including manufacturers and distributors of communications equipment, computers and peripherals, electronic equipment, and related instruments; and semiconductors and semiconductor equipment manufacturers. The sector breakdown is shown below.

VGT Sector Exposure (Bloomberg)

In terms of company exposure, the fund is heavily concentrated towards Apple (AAPL) and Microsoft (MSFT), which have a combined share of 43% of the index. Nvidia (NVDA) is the third-largest holding, with a 6% weighting. The fund charges a fee of 0.1% and pays a dividend yield of just 0.7%.

VGT Company Exposure (Bloomberg)

The Valuation Premium Has Reached New Extremes

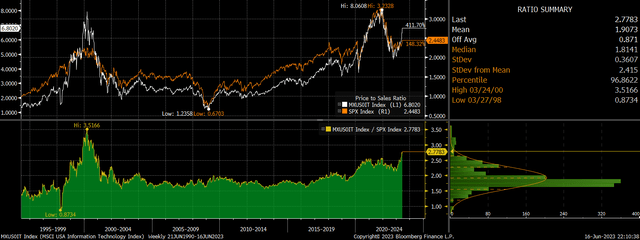

The price-to-sales ratio for the MSCI IT index is currently 6.8x, which is in the top 5% of valuations seen going back to 1995, double its long-term average. The extent of overvaluation is even more significant when measured relative to the S&P500. The MSCI IT’s price-to-sales premium is in the top 3% of all observations going back to 1995 and is 2.4 standard deviations from its long-term average. The only time the tech sector has traded at a higher premium was in the last few months of the 2000 dot com bubble.

MSCI USA IT Vs S&P500 Price To Sales Ratios (Chart)

This extreme valuation premium on a price-to-sales basis does not take into account the improvement in profit margins seen in the tech sector over the past two decades. However, even on a price-to-earnings basis, the tech sector still trades at 67% above the S&P500 at 35.4x.

Looking into the breakdown of the change in profit margins between the MSCI IT index and the S&P00, the single biggest driver of the relative improvement in tech margins has been the decline in interest and tax expenses. In 2000 interest and tax expenses reduced net income by around 35%, and this figure is now a 5% positive contribution. If we strip out the interest and tax and focus on price-to-operating income, the MSCI IT index trades at a 75% premium to the S&P500. If we further strip out depreciation and amortization, the valuation premium rises to 85%.

Deeply Negative Long-Term Returns Likely

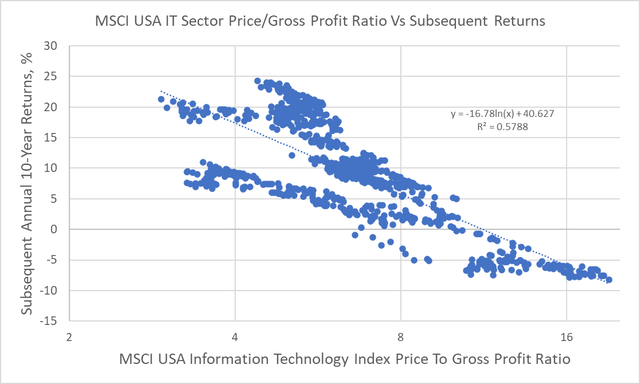

The reason I prefer to strip out the impact of non-core expenses is that they tend to be highly volatile and mean reverting. As a result, earnings metrics that strip out non-core expenses tend to be more closely correlated with actual subsequent returns. It turns out that the earnings metric most closely related to subsequent long-term returns is the price-to-gross profit ratio as this captures structural rather than cyclical changes in profit margins. The MSCI IT’s current price to gross profit ratio sits at 13x. The chart below shows the correlation between the relationship between the MSCI IT’s price-to-gross profit ratio and subsequent 10-year total returns. The current ratio is consistent with annual returns of -2% over the next decade.

Bloomberg, Author’s calculations

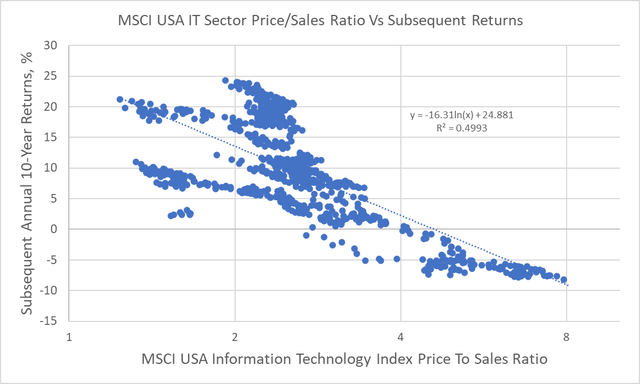

Even this weak outlook may prove too optimistic, as embedded in those implied returns is the gradual expansion in gross profit margins, which is not something we should expect to continue. If we strip out profit margins all together and focus on the price-to-sales ratio, the current figure of 6.8x is consistent with 10-year annual returns of around -6% based on data over the past 30 years. This would mark the worst period of long-term tech sector underperformance since the very peak of the 2000 bubble and leave the VGT around 50% lower than current levels in total return terms.

Bloomberg, Author’s calculations

This may seem overly pessimistic, but all it would take is for investors to require slightly higher long-term returns than historical sales growth and the current dividend yield imply. Over the past two decades, sales growth has averaged 6% annually. Even if we assume that this growth rate continues and profit margins remain at current elevated levels, with a dividend yield of just 0.7%, this would result in 6.7% annual returns assuming no change in valuations. If investors were to require returns of 10% annually in line with the post-War S&P500 average, this would require the dividend yield to rise to 4%, which in turn would require an 83% decline in valuations.

Unlikely To Be Different This Time

While extreme valuations make negative long-term returns highly likely, we cannot rule out the possibility that Artificial Intelligence is successful in addressing the long-term decline in US productivity and allowing the economy to grow fast enough to allow earnings to catch up with current valuations. However, the resources that will be required to build the hardware, train the machines and the people using them, and the resources that will be required to regulate and (hopefully) ensure that bad actors do not use the technology for nefarious purposes, must be taken into consideration. Also note that the creation of the internet itself was unable to make a dent in the US’s long-term productivity growth decline.

Read the full article here