Investment Thesis

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services, and technology solutions through an integrated omnichannel B2B distribution platform offering a wide range of office solutions through its ~950+ retail stores. It serves a wide range of small, medium, and enterprise-level companies including within education and public sectors. Work from home during the pandemic threatened its core business, however, sales quickly recovered on its low-cost value proposition and customer-centric approach boosting its consumer division driven by sale of furniture, technology, PPE, and cleaning supplies. It embarked on a transformational journey amidst the pandemic cutting costs, closing several underperforming stores (closed 400 stores, a third of the total, in the last 3 years) and lowering its cost base by $500 mn, sold off service-based CompuCom division for $305 mn to focus on its core business, completing sale and leaseback of its HQ for $104 mn and rebuffing spinoff after a long drained evaluation as the board eventually concluded in having value under a common ownership.

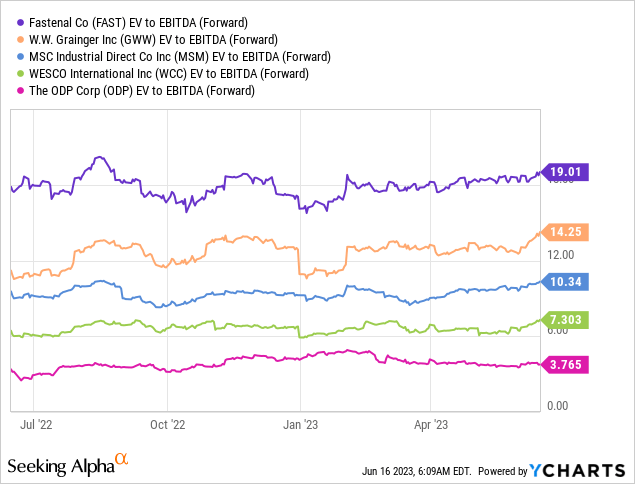

We believe ODP has shown strong resilience in the tough macroeconomic environment and has drivers to drive long-term shareholder value. At 3.7x EV/ 2023E EBITDA, we believe the risk-reward is favorable. Initiate this as Buy on Dips opportunity.

Earnings Momentum Intact

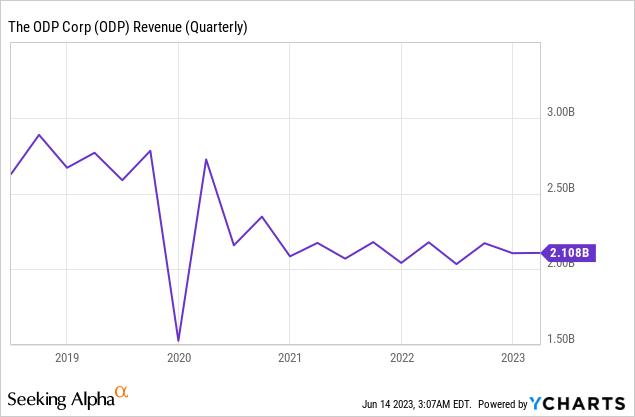

ODP reported Q1 revenue decline of 3% YoY, primarily driven by fewer locations in its consumer division as well as lower traffic, partially offset by stronger sales in its B2B division which grew 3% YoY as flexible pricing strategies and return to the office trends led to a fillip to sales driven by its core categories of breakroom, furniture, technology, copy and print. This also is impressive as a result of tough lapping in Q1 last year due to higher COVID-related supply sales. The supply chain business, Veyer, saw strong growth in Q1 with sales to third-party customers growing 50% YoY to $7 mn and operating income doubling to $2 mn. Veyer’s existing distribution footprint with its ability to serve about 99% of the US the next day perfectly positions it to grow its external customer base and achieve its long-term target of $30 mn+ EBITDA by FY25. Varis is a B2B procurement tool which is looking to grow in a sizeable addressable market which is gaining traction, having launched in Nov 2022.

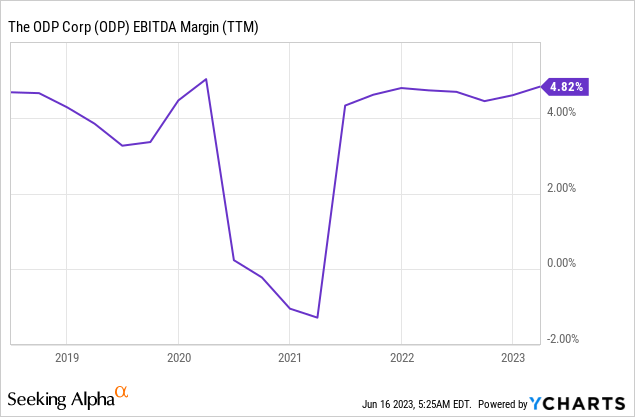

Gross margins received a boost, improving 60 bps YoY, driven by freight tailwinds and lower fuel prices. Operating margin improved 66 bps YoY to 4.7% driven by SG&A leverage and improved gross margins demonstrating a significant improvement post-COVID (pre-pandemic operating margin average of ~4.0%).

EBITDA margins continue to demonstrate improvement and resilience post the slump during COVID maintaining its strength in core categories, low-cost model, disciplined pricing and expanding to high-growth adjacency products. EPS grew 40% YoY, driven by stronger margins and cash conversion remained high as a result of prudent inventory management.

Balance sheet continued to remain strong with total liquidity of $1.1bn ($345 mn in cash and $800 mn in available credit line). Gross debt remained negligible at $222 mn with Debt/ EBITDA at just ~0.5x. ODP continues to aggressively buy back stock, having bought back $200 mn of stock in the current quarter and $350 mn since the announcement, with $650 mn still left within the buyback program. It maintained its guidance of sales of $8.0-$8.1 bn and EBITDA margins of upwards of 5% with EPS of $4.8 at mid-point maintaining a cautionary stance amidst the current challenging macro environment.

Return to Office

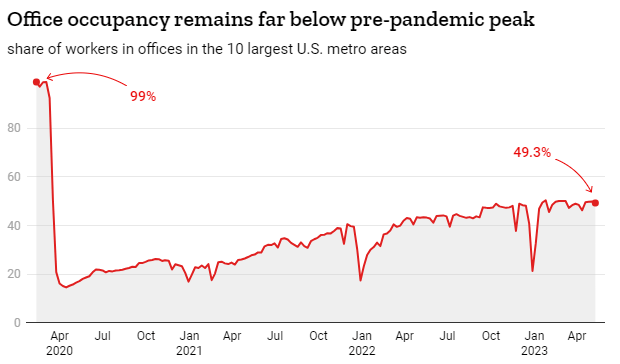

According to The Flex Report, Return to Office trends continue to remain steady with the proportion of Hybrid + Fully Office model at 72% vs 69% in the last quarter. Hybrid has gained most traction with people turning up for about 2.5 days in a week, with Tuesday and Wednesday being the most popular for the employees to swipe their cards into their offices. As a result, office occupancy remains far below its pre-pandemic peak, however, it has steadily increased and continues to improve.

TIME

We believe while structured hybrid is the future of the workplace, workers’ occupancy at a long-term average above 50% would bode well for ODP along with continued growth in its high-value adjacency products including technology and supplies which would continue to be in demand as workers would be working from home for the remaining half of the week.

Valuation

ODP trades cheaply at just 3.7x 1Y Fwd EV/ EBITDA, significantly lower than its peers (although it operates at a relatively smaller scale and lower margins compared to others).

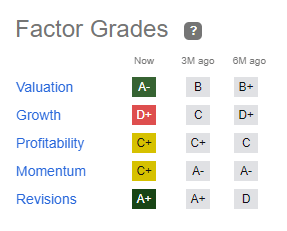

As per Seeking Alpha, valuation grade remains attractive with a rating of A-, while the stock largely remained flat during the past 3-6 months driven by improve in earnings momentum. We initiate this as a Buy on Dips opportunity.

Seeking Alpha

Risks to Rating

Risks to the rating include 1) significant deterioration in the labor market on the back of macroeconomic headwinds which would significantly pressure its core as well as adjacency sales 2) While management highlighted that 2022 was the peak year of investment in Varis, a slower ramp-up and adoption would lead them to continually reinvent leading to higher investments and continued losses 3) retail business may continue to face pressure as consumers turn online leading to declining sales and 4) margins may have peaked out as SG&A deleverage while sales continue to remain under pressure

Final Thoughts

ODP has shown strong resilience amidst a declining traditional core business with its low-cost offering and growing focus on adjacency products. While the trends in the traditional office supplies remain a headwind, we believe the downturn within its retail business may have bottomed out as the sales continue to improve sequentially (excluding the impact of store closures). We believe at 3.7x 2023E EV/ EBITDA, ODP offers favorable risk-reward with return to office trends remaining steady. A healthy balance sheet and strong cash conversion would lead to continued momentum in its buyback program, which would further drive earnings. We initiate with a buy on dips opportunity.

Read the full article here