This article was first posted in Outperforming the Market on June 2, 2023.

This article will provide a deep dive fundamental analysis of a leading LiDAR player, Innoviz (NASDAQ:INVZ).

With valuations for unprofitable companies down drastically from one to two years ago, I think that it is time to scoop up some beaten down LiDAR names.

Of interest to me is Innoviz, which along with Luminar (LAZR), has been one of the leading LiDAR players gaining most of the market share in the industry.

I have completed a two-part deep dive research into Innoviz for members of Outperforming the Market that can be found here, and I will also be publishing my Luminar deep dive next week, so watch out for that one as well.

But first, here is a brief introduction into Innoviz.

Brief introduction to Innoviz

Innoviz is a leading provider of LiDAR and perception solutions that enable autonomous driving.

Its products and solutions can be used in the automotive sectors like robotaxis, shuttles, delivery vehicles, buses and trucks, and in other industries that require autonomy like in logistics, drones, robotics, construction and other industrial applications.

Innoviz was founded by veterans of Unit 81, which is the elite technology unit of Israel’s Intelligence Corps, in 2016. The founding team created a new type of LiDAR sensor, from the chip-level up, and also developed software applications to allow for superior perception.

As early as in 2017, Tier-1 companies like Magna and Aptiv were interested in Innoviz’s LiDAR prototype. In 2018, Innoviz achieved a design win with BMW and in 2022, it was selected to be Volkswagen’s direct LiDAR supplier. Also in 2022, Innoviz was again chosen as a direct LiDAR supplier for an Asian EV-focused automotive OEM selected us to serve as its direct LiDAR supplier for series production passenger vehicles. Innoviz has LiDAR solutions that meet the requirements for Level 2+ through Level 5 autonomous vehicles and its solutions are offered at price points suitable for mass produced passenger vehicles. In addition, its software suite enables Innoviz’s 905nm wavelength laser-based LiDAR architecture to be easily leveraged to provide compelling solutions for Level 2+ through Level 5.

The company uses contract manufacturers for manufacturing and has been increasing its manufacturing capacity through third party contract manufacturers to meet the steep demand in its products in the next few years.

I will highlight my investment thesis for Innoviz below.

Investment thesis

Innoviz is well positioned in the LiDAR space as it has the largest order book in the industry to date. With the majority of global OEMs looking to make their LiDAR decisions in the next 12 to 18 months, this implies that Innoviz is one of the few players in the market that will operate at a future scale large enough to confer scale and cost leadership advantages.

In addition, I expect the LiDAR industry to consolidate meaningfully amongst two to three players with significant scale while other competitors are unlikely to compete meaningfully.

On top of that, Innoviz has a structural advantage as it has integrations with the top three autonomy platform players.

Software presents a huge opportunity for Innoviz as its unique perception software is able to work with its LiDAR products to bring about software revenues that are not only higher margin but also brings in recurring revenues. On top of that, there are opportunities for cross selling with the recently launched software product.

The commercial traction it has made comes from its strong product portfolio with a focus on technology and continued innovation, relationships with leading OEMs, and solid intellectual property portfolio and software solutions. This will differentiate Innoviz from its other competitors as it looks to win market share in the space.

Next, let us look at the company’s product portfolio.

Innoviz product portfolio

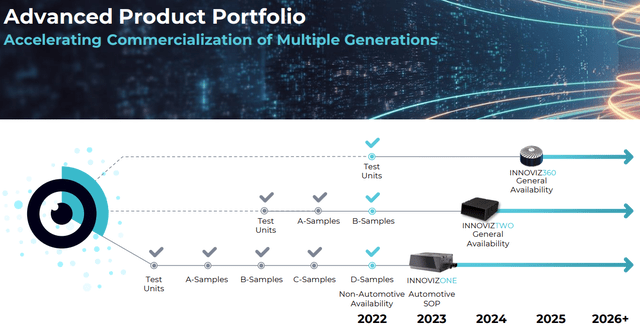

I will elaborate more on each product in its portfolio in the next section. This picture shows how Innoviz has progressed over the years from the initial test units of InnovizOne to its first automotive SOP in the second half of 2023. In addition to that, we see that InnovizTwo and Innoviz360 has their own timeline, and with each new product, Innoviz improves on its previous generation and is also looking to target different market segments.

Innoviz product portfolio (Innoviz IR)

Strong focus on technology in its product portfolio

Innoviz recognized since its inception the limitations of the use of 1,550nm lasers in the automotive market and thus, brought its efforts to develop a LiDAR solution that uses 905nm based lasers designed to outperform 1550nm based LiDARs that are more expensive.

Innoviz started work on its LiDAR ground up to overcome the limitations of 905nm lasers through the use of unique scanning mechanisms, silicon detectors to improve optical-electrical conversion of the received signal, and the ASIC chip to optimize the detection capabilities for a given optical link budget.

It is important to note that Innoviz products were created from ground up, where the hardware was created from the chip-level up and its software applications were also created for superior perception.

Innoviz currently has three key products in its product portfolio. The InnovizOne, InnovizTwo and Innoviz360.

Both InnovizTwo and Innoviz360 have a technology that is distinct from InnovizOne. InnovizTwo is meant for automotive customers that enables better price at a solid performance when compared to InnovizOne. Innoviz360 uses a similar architecture to InnovizTwo but it further enables scaling a further enables scaling across non-automotive applications while also featuring Level 4 and Level 5 autonomy capabilities.

Innoviz product portfolio (Innoviz IR)

On top of its leading hardware products, Innoviz also provides a unique perception software solution that converts the raw data collected from Innoviz LiDARs.

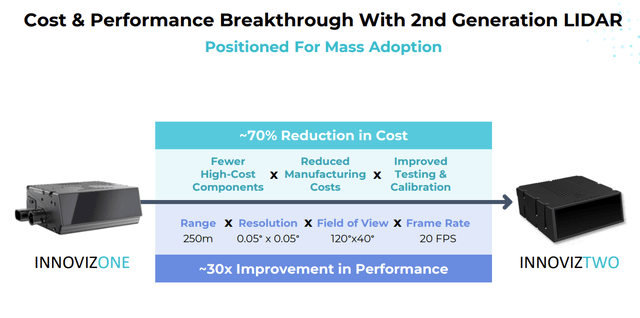

InnovizTwo presents a breakthrough compared to InnovizOne given its 70% reduction in costs, and at the same time, an increase in performance by 30 times. InnovizTwo will allow OEMs to offer L2+ while the hardware supports L3 and L4 with just a software upgrade.

Benefits of second generation LiDAR (Innoviz IR)

Last but not least, Innoviz has its unique perception software to work with its hardware solutions mentioned above to turn raw point cloud data into perception outputs. Innoviz’s software also uses the data from its hardware as well as using proprietary AI algorithm to bring about superior scene perception. This perception software has been validated with the highest automotive standards to ensure it meets the high standards of the automotive industry. From a financial point of view, software revenue is also key because it is a higher margin business that will result in recurring revenues and high switching costs.

Integration with all top three autonomy platform players brings structural advantage

When thinking of Innoviz as a LiDAR player, I think it’s also important to realize that OEMs need to have a seamless integration their hardware with their software, like the inputs from sensing and perception derived from components like LiDAR.

In this regard, I think Innoviz has a structural advantage over peers.

The top three compute platform players today are Qualcomm (QCOM), NVIDIA (NVDA) and Mobileye (MBLY). Innoviz currently is integrated with two of them, Qualcomm and Mobileye, and is looking to integrate with all major players in the space. The company also believes that through working and integrations with these top autonomy platform partners will lead to faster time to market, speed up the customer evaluation process and make it much easier for the customer to decide to use Innoviz’s products and solutions. As such, the integration with all top three compute platform players should lead to more wins in the future.

Innoviz is currently working with NVIDIA, which will be the last of the three autonomy compute platform players that the company has not yet worked with. Currently, Innoviz is discussing with NVIDIA about being integrated into series production programs leveraging the Hyperion platform. The current discussion with NVIDIA will involve several large OEMs and can also potentially bring in more RFI and RFQ activity and bring in more NVIDIA-based programs into Innoviz’s pipeline.

To understand why it is important to have all three of the top three autonomous platform players, you first need to understand the decision process of OEMs.

Some OEMs source for their compute platform and LiDAR supplier in parallel and the decisions are made independently of each other

Other OEMs start to pick the compute platform first, and then make decisions about the sensor suite after having chosen the compute platform. As such, in this scenario, for a player like Innoviz which has already been integrated with the top three compute platform players, this results in OEMs being more likely to choose Innoviz as a solution given the lower risks and reduced time and cost needed to use Innoviz’s solutions with the compute platform it has already chosen.

I am of the view that we will see Innoviz integrate with all the top compute platforms in the near-term as it is currently in discussions with the last of the top three compute platform players. I see this as a clear structural advantage for Innoviz, which will bring incremental benefits to the company over time. I think that having strong relationships and integration with the top autonomy compute platform players will also form a barrier of entry for smaller competitors of Innoviz given that they may not have such relationships and integration with all three players.

Introducing a new software solution

In its 1Q23 quarter, Innoviz announced a new software product offering.

As part of its discussion with a global OEM, the scope of the RFQ was expanded to the industry’s first LiDAR-based minimum risk maneuver (“MRM”) system.

The global OEM was impressed by what Innoviz’s LiDAR and perception software could deliver and thus, expanded the scope of its RFQ.

What is an MRM system?

An MRM system operates as a backup system, where if a vehicle’s primary system has issues, the MRM system offers a transition period for the driver to repossess control of the vehicle as the MRM system is able to take over control of the vehicle during this transition period. As a result, the MRM system offers improved safety to the vehicle. It sits on a dedicated compute box within a vehicle.

Innoviz offers a LiDAR-based MRM system, compared to the traditional camera-based ones that have been around for some time. The advantages of a LiDAR-based system includes a true 3-D image, reduced risk in low light and extreme sun situations as well as environmental considerations like rain or snow.

I think this is positive on three fronts.

Firstly, the ability to offer software is incremental to Innoviz’s margin profile given the higher gross margins of software compared to hardware. As a result, the higher margin profile of software can help improve the overall margin profile for Innoviz as a whole, creating a more profitable organization.

Secondly, the move into selling software allows for cross sell opportunities. Given that Innoviz has the largest order book today, I believe that the millions of unit volume that Innoviz is shipping in the future will translate to significant cross sell opportunities for Innoviz from hardware to software.

Lastly, the ability to offer a LiDAR-based MRM system will enable incremental wins from other OEMs looking for a similar complementary offering, on top of the usual LiDAR and perception software that Innoviz offers.

Leading customer order book

Innoviz’s customer strategy is to first penetrate and win businesses with major OEMs on one platform and then over time, become their LiDAR vendor of choice for future programs that they wish to deploy LiDAR.

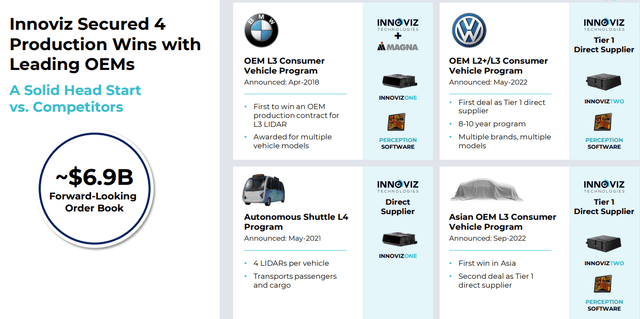

Innoviz currently has the lead in the industry in terms of its order book, which adds up to $6.9 billion and will be once again updated in its 4Q23 earnings call.

Prior to 1Q23, Innoviz announced four series production awards. They include the series production awards with BMW, Volkswagen, the shuttle program and the Asian EV-focused OEM.

The BMW and shuttle program is on target to SOP in the second half of 2023, while the program with the Asian EV-focused OEM is expected to SOP late 2024 or 2025, while the Volkswagen series production award is targeting a mid-decade SOP.

Innoviz Order Book (Innoviz IR)

New light commercial vehicle program

On top of those mentioned earlier, Innoviz announced a new light commercial vehicle program which it was in late stage discussions with in the prior quarter.

This newest Level-4 light commercial vehicle relates to a commercial van, where Innoviz expects to have three to four LiDARs per vehicle.

The important thing is that this program has a “very accelerated timeline”, with a mid-decade SOP target.

As a result, management expects that this new light commercial vehicle program to contribute to revenues in the second half of 2023 as a result of Non-recuring Engineering (“NRE”) coming from this program.

In addition, I also appreciate the fact that the fact that this program is moving this rapidly is due to Innoviz being able to displace a development stage competitor, according to the 1Q23 Innoviz earnings call.

I think that this program announcement highlights the strength and quality of Innoviz’s technology, its leadership in the space compared to other peers and the key moment this next 12 to 18 months will be for decisions in relation to LiDAR sourcing and selection by major OEMs.

Largest customer

Volkswagen is Innoviz’s largest customer.

In late 2022, Innoviz announced a $4 billion contract with Volkswagen for 5 million to 8 million LiDAR units.

Innoviz is targeting a mid-decade SOP for its existing series production with Volkswagen and the company will be supplying LiDAR units to Volkswagen for eight years.

It continues to work with both Volkswagen and CARIAD, its internal software company, on more programs, some of which are in advanced stages of discussion.

Management believes that they are continuing to make solid progress with Volkswagen and continue to see opportunities for growth with Volkswagen.

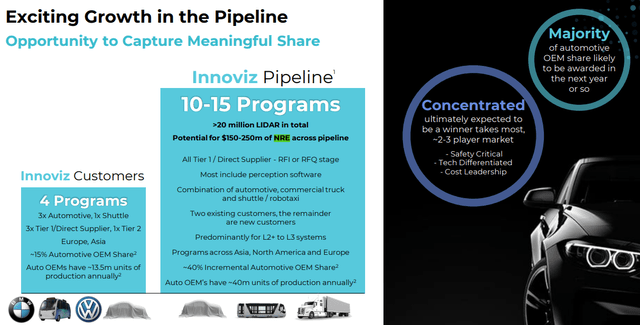

Solid pipeline

In its pipeline, Innoviz currently has 10 to 15 programs in the RFQ and RFI stage.

In the first quarter of 2023, Innoviz saw a record number of programs’ move from the RFI to RFQ stage. About half of the pipeline of 10 to 15 programs are in the RFG stage, which is the first ever time this is the case for Innoviz.

As such, they are working on a record number of more than five RFQs in the pipeline.

Innoviz pipeline (Innoviz IR)

In total, combining the 10 to 15 programs in the pipeline and the customers already announced, Innoviz currently has eight out of the top 10 global automakers as either its customer or in its pipeline.

Outlook for new customers and pipeline

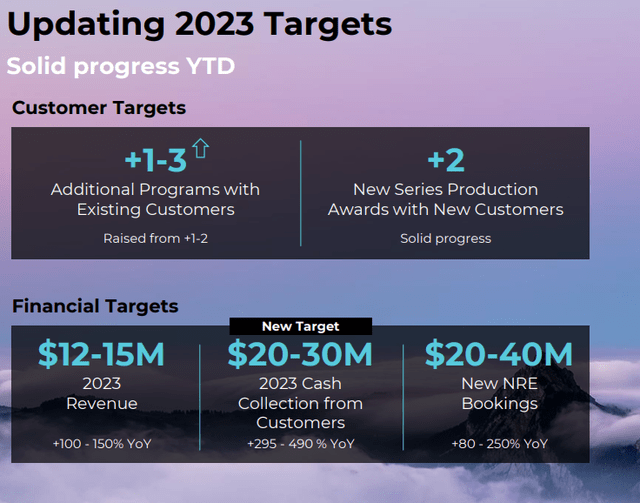

I think that the raise in Innoviz’s guidance for 2023 highlights increased confidence and visibility into its pipeline and potential wins.

Innoviz increased their additional programs with existing customers from the initial 1 to 2 customers to 1 to 3 customers. I am of the view that management has sufficient line of sight on 2 to 3 additional decisions from existing customers and thus, the ability to raise the guidance on this front.

In addition, Innoviz expects to have 2 new series production awards with new customers in 2023. Management believes that there are a few RFQs that have the potential to move towards final commercial negotiations by July and expects to announce something by the end of the year.

In addition, management expects to collect $20 million to $30 million this year from customers, which includes things like NRE.

Innoviz 2023 targets (Innoviz IR)

In terms of its long-term funding strategy, management highlighted that strong growth will serve as its main long-term funding strategy as a result of the significant cash collection that Innoviz will be collecting from customers in this phase. I will elaborate more on pre-production revenues next.

Pre-production revenues

It can take two to three years before production starts. During that period of time, Innoviz has three main sources of cash: sample unit shipments, non-automotive shipments, and NREs.

Sample unit shipments are crucial for Innoviz as they bring higher gross margins than production shipments as they sell in the range of $5,000 to $15,000. This is compared to the production selling price of below $1,000 and sometimes even around $500 at larger volumes. Crucially, these sample unit shipments are priced for Innoviz to recover fixed costs like research and development investments. As a result, each customer program in its pipeline could bring in millions per year for each award as a result of several hundred units per year during the pre-production phase. With 10 to 15 programs in the pipeline, this could mean several tens of millions per year.

Non-automotive shipments started in late 2022 and is starting to ramp in 2023. With non-automotive shipments, the selling price is similar to sample unit sales and thus, there are significant gross margins that can again help with Innoviz’s fixed costs. Management mentioned that the introduction of Innoviz360 could be a catalyst for its non-automotive shipments and expect that the company could be shipping tens of thousands of units each year, translating to significant growth in the near-term.

Lastly, for NRE, or Non-recurring Engineering, this relates to engineering of the product prior to SOP and acts as services revenues. Innoviz receives cash from its customers from NRE and it forms a significant part of its funding strategy. With 10 to 15 programs that are in its pipeline, and with the expectation that each program could bring in $10 million to $50 million, the total NRE to be brough in will be between $150 to $250 million.

As a result of significant cash to be received from NRE, sample unit shipments and non-automotive shipments, Innoviz’s funding strategy will be to use these forms of income to fund its strategy and fixed costs.

Conclusion

All in all, I think that Innoviz has a strong product portfolio focused on technology and innovation that brings the best LiDAR products and solutions to the market. Its software solutions will bring incremental benefit to revenue and margins. Most importantly, the company has an industry leading order book of $6.9 billion, with Volkswagen as its largest customer. In addition, it still has 10 to 15 programs in the RFI and RFQ stage that can translate into wins and revenues in the future. Lastly, the significant pre-production revenues and cash it will be receiving in the next two to three years will be key to providing the company the funding it needs for the next few years.

Read the full article here