Both the shareholders of Hudbay Minerals (NYSE:HBM) and Copper Mountain Mining (OTCPK:CPPMF) overwhelmingly voted in favor of the acquisition of the latter by the former. The all-stock transaction seems like a good deal for both companies, given Hudbay’s already leveraged balance sheet and the upside that CPPMF’s shareholders retain. It remains to be seen to what extent Hudbay’s management will be able to realize the indicated $30M worth of operational efficiencies and synergies. Overall, I think that the transaction is a good step towards positioning Hudbay as a mid-tier Americas focused copper producer and remain bullish on the company.

The Copper Mountain Mining deal

M&A activity in the copper space has been on the rise these days. Probably the most notable deal is the acquisition of OZ Minerals by BHP (BHP) as the two companies are amongst the largest in the sector. However, M&A deals are happening on a smaller scale as well. Such is the acquisition of Copper Mountain Mining by Hudbay Minerals, which was approved by the shareholders of both companies recently.

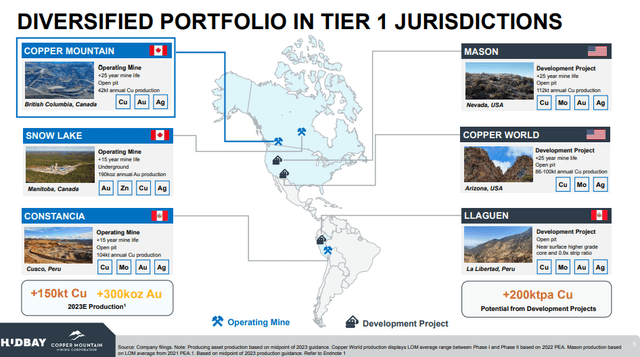

Combined asset portfolio (Hudbay Minerals)

The deal will be all-stock, which is understandable, given Hudbay’s already pretty leveraged balance sheet. This will also allow existing shareholders of Copper Mountain to be fully exposed to the development of the future combined entity.

Is Copper Mountain a good fit for Hudbay?

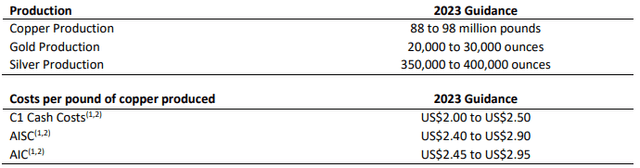

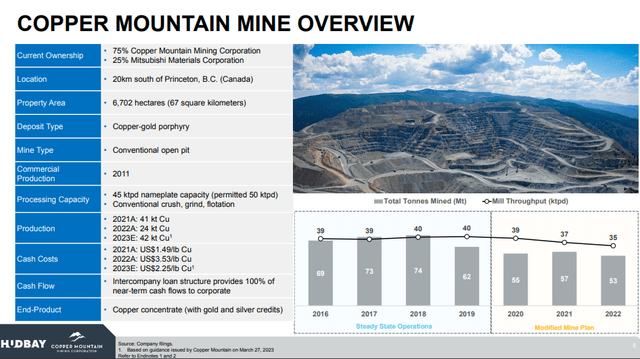

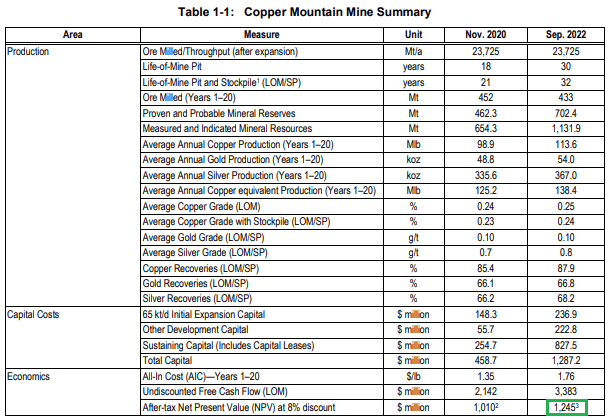

Copper Mountain Mining is a single-asset company – the Copper Mountain mine, where the entity has 75% equity interest. The mine itself is expected to produce around 42k tonnes of copper (guidance midpoint) in 2023 as well as 20-30koz of gold and 350-400koz of silver. In terms of quality, the mine is inferior to Hudbay’s operating assets, as grades are lower and costs are higher. It has been underperforming lately, as cost inflation and various technical challenges have affected operations.

Copper Mountain mine production guidance (Copper Mountain Mining)

On the other hand, the Copper Mountain mine is in Canada, which is a pretty safe mining jurisdiction, especially if the mine is already built. Not the same could be said about Peru, where roughly half of Hudbay’s revenue comes from. So in terms of political risk, the merger is an improvement for Hudbay.

Copper Mountain mine highlights (Copper Mountain Mining)

At the end of the day, the opportunities for Hudbay were not unlimited, so Copper Mountain Mining was one of the few possibilities, given Hudbay’s size and emphasis on the Americas. One company of similar size to Copper Mountain Mining, which comes to mind, is Taseko mines (TGB), which I wrote about. However, given that Taseko is one permit away from constructing its second producing asset, the price that a potential acquirer must’ve paid would’ve likely been north of US$1B.

Was the price fair?

The all-stock structure of the deal, at the moment it was announced, put equity value on Copper Mountain Mining of $439M – a 23% premium over the 10-day VWAP. However, the net debt of approximately $135M has also to be taken into account, which puts the EV at which the deal was struck at $574M.

Copper Mountain mine economic profile (Copper Mountain Mining)

For comparison, according to the September 2022 Technical report, the Copper Mountain mine has an after-tax estimated NPV of $1,245M on a 100% basis or $934M on a 75% basis. The report used a long-term copper price of $3.60/lbs, gold of $1,650/oz and silver of $21.35/oz. These assumptions seem quite conservative and are below today’s market prices, which is off-set to an extent by the higher operating costs due to inflation. So it appears that Hudbay is acquiring Copper Mountain at around 0.615x NAV, which seems reasonable.

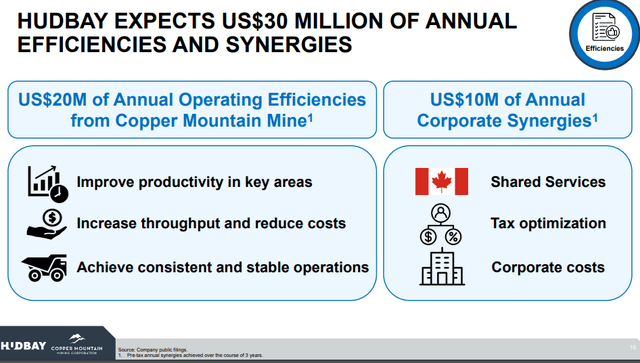

Cost savings and synergies

Hudbay claims that it could use its expertise and realize around $20M of annual operational cost savings. The logic behind this is that Hudbay’s Constancia mine in Peru is similar to the Copper Mountain mine, and it uses similar equipment. Another $10M of annual corporate synergies are identified.

Identified cost savings (Hudbay Minerals)

The big question remains: to what extent will Hudbay be able to realize those cost savings, given that the Copper Mountain mine is quite low-grade, thus especially prone to cost increases?

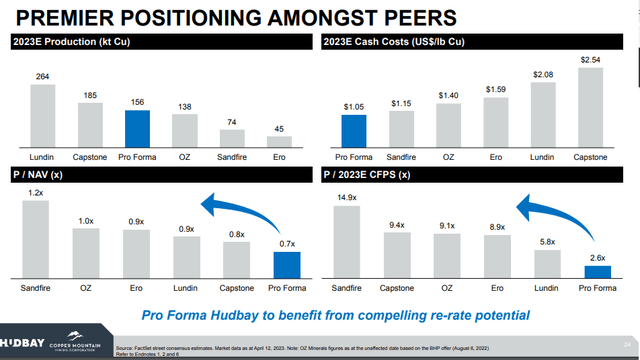

Attractive valuation

Peers comparison (Hudbay Minerals)

The combined entity has an attractive profile when compared to some of the leading companies in the copper space. That said, in the small and mid-cap subsector, there are other attractively priced companies like Taseko mines, which is my top pick for copper exposure. Still, Hudbay also appears to have upside as it trades considerably below its NAV, and I’m overall bullish on the company.

Risks

Execution risk

With every merger or acquisition, the implementation of the identified cost savings/synergies bears risk. If Hudbay’s management is unable to optimize operations in the Copper Mountain mine, the asset may end up being a drag on the combined entity.

Interest rates risk

The combined entity is quite leveraged. As of 31 March 2023, Hudbay has net debt of a bit over $1B, the bulk of which matures in 2026 and 2028. The majority of Copper Mountain’s debt also matures in 2026. So the combined entity will have to face around $750M of debt coming due in 2026. While it’s unlikely that the company will pay all of it, the portion that will be rolled over will be quite sensitive to interest rates.

Political risk

Roughly half of Hudbay’s revenue comes from its Peruvian operations, which are a source of political risk. The situation there was especially tense in the beginning of the year, when the country was rocked by violent protests. Now things have calmed down, but still the risk remains elevated.

Conclusion

While the Copper Mountain mine was not the ideal fit for Hudbay, it’s likely the best that was available on the market. Realizing the identified cost savings and synergies of $30M annually will be the key for making the deal worth it for the shareholders of both companies. Overall, I remain bullish on Hudbay, as it continues to trade at lower multiples than peers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here