Investment Thesis

Dufry (OTCPK:DUFRY) is a leading travel retailer that operates shops located in airports, cruise lines and tourist locations across Europe, North America, South America, Africa, and Eurasia. It had been thrown into an existential crisis during COVID as global travel came to a grinding halt. It raised CHF 1.9 bn in funds through rights issue and convertible instruments and sought refinancing of its debt in order to fend off the crisis. However, post reopening and strong recovery in travel demand, we believe Dufry is at an inflection point with a play on long term passenger growth along with rising passenger spends. Its recent acquisition of Autogrill would provide them solutions within the F&B market and bring in more synergies and cross selling opportunities. We initiate this as a Buy rating.

Strong Recovery in Global Travel

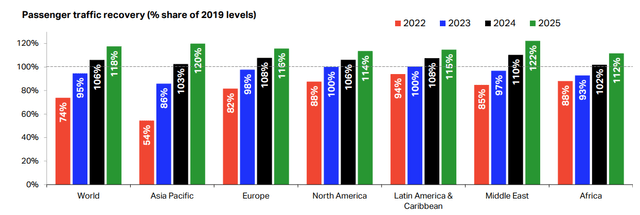

According to IATA, Passenger travel recovery is expected to be 95% of the 2019 levels primarily driven by reopening of China and recovery in air travel along with continued momentum seen in North America and European markets.

IATA

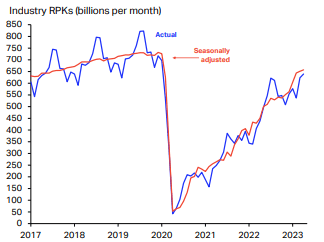

In addition, industry wide revenue passenger kilometers (RPK), maintained its upward trajectory, in line with passenger demand recovery, although it still remains a shade lower than 2019 levels. The recovery in traffic is primarily driven by domestic traffic growth which has fully recovered as domestic traffic in China showed an astounding progress with a 6x+ traffic growth YoY, albeit on a low base.

IATA IATA

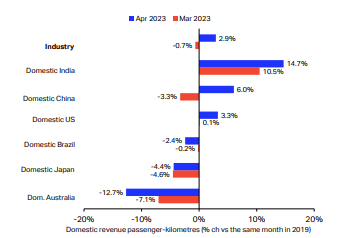

While domestic travel has recovered from COVID blows, international travel still remains below pre-pandemic levels by ~16%.

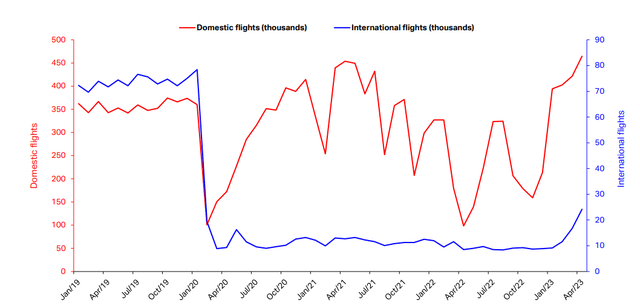

China Domestic and International Monthly Flights

IATA

This is despite the fact that China being one of the major contributors to international travel has seen only ~30% recovery in international flights. However, robust growth has been seen in international RPKs between Asia and the Rest of the World with traffic seen coming back to China and outbound. According to UNWTO, Chinese tourists spent an estimated $250 bn+ in 2019 putting themselves number 1 globally in tourist spends, even more than US and UK combined. We believe reopening of China and its rising demand of international travel along with sustained growth in domestic traffic would drive strong growth in passenger air traffic in the near term.

Strong Earnings and Guidance

Dufry reported a strong beat on revenues and earnings with Q1 sales up 111%, on a lower base, driven by 51.5% growth in organic sales. This still remained 2-3% below 2019 levels which we think is primarily driven by pricing as passenger recovery is about 90% of the pre-pandemic levels. However, management noted that April was even stronger with organic sales 2-3% above the 2019 levels on robust consumer demand. Autogrill is likely the biggest driver as a result of improved pricing and rising demand for convenience products. EBITDA margins improved 190 bps YoY and it posted an EBITDA of CHF 134 mn, higher than much of the previous years, despite Q1 being a seasonally weak quarter. Further, cash conversion continued to improve on normalizing inventory despite seasonality and is expected to further improve in the mid-term on the back of improving operating cash flows and normalizing working capital requirements along with a rapidly deleveraging balance sheet (it expects leverage to be around 3x at the end of the year).

It reiterated the guidance for the year of 7-10% sales growth in its core business on passenger volume recovery and China reopening, although taking a prudent approach to reflect the current macro uncertainties elsewhere. It expects an EBITDA margin of 8% with demand for premium products has been rising along with lower requirements of promotions to benefit gross margins along with tighter cost controls. We believe near term momentum continues to look robust on a strong revival in air traffic demand, particularly from China and normalizing inventory and concession would lead to improved operating margins which would further drive cash conversion and help deleverage its balance sheet.

Group’s leverage position improved sequentially to be at 3.1x Net Debt/ EBITDA, in line with its long term goal of 3 – 3.5x Net Debt/ EBITDA. Liquidity position also remains strong at CHF 2.7 bn, including commitments signed in April 2023, to facilitate future needs with no major maturity until 2024. S&P and Moody’s also recently upgraded their credit rating to BB- Creditwatch positive and Ba3 Outlook Positive, respectively on the back of rapid improvement in operating cash flows and deleveraging balance sheet.

AENA Concession

AENA announced a new contract for 86 duty-free stores across 27 airports in 2021, making it the largest global airport tender by value, with the total contract worth c€18bn over 12 years. Dufry bid for a set of 4 lots in the AENA concession at 28% higher than Minimum Annual Guarantee Rent (MAGR) across the packages. Dufry is the current contractor, having held since 2012, which is due to expire in October 2023, with results expected in July 2023, and is competing against Lagardère Travel Retail. However, two key lots at high profile tier 1 locations in Madrid and Barcelona received no bids demonstrating that the concession rates in the tier 1 locations have peaked. It is largely expected that Dufry would continue to be the contractor, however, any potential negative on the development could be a dampener (although not meaningfully on earnings as EBITDA margins remained flat to negative for the AENA concession as of 2019)

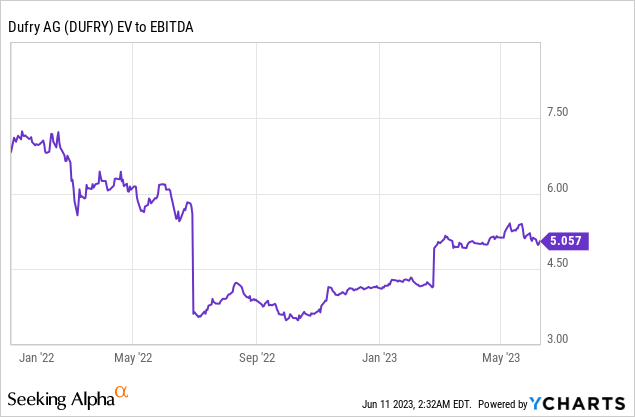

Valuation

Dufry traded at an average EV/ EBITDA of 9x pre-pandemic vs currently at ~5x. Even considering a 20% discount to factor in execution risks and macro uncertainty, we believe it still provides a reasonable upside to the current target price. We initiate this at buy.

Risks to Rating

Risks to rating includes 1) Integration of Autogrill may not materialize the anticipated cost synergies as planned. Autogrill is Dufry’s entry into the F&B travel market and its limited experience with the space could lead to higher execution risks. It expects cost synergies of CHF 85 mn on integration which could be prolonged or not met due to its limited experience within the sector 2) Passenger recovery could slow due to macro economic slowdown, any government restrictions, airline capacity cuts or any emergence of a new strain of COVID-19 as witnessed in recent times where the passenger air traffic was decimated and still have not recovered fully 3) Decrease in retail spending due to consumer led slowdown as a result of current macro economic challenges 4) Operating Margins can be squeezed downwards as a result of inflationary pressure and wage hikes 5) any adverse impact of AENA concession in Spain going to the competition (formed ~6% of Dufry’s revenues in 2019) where in it is competing with Lagardere Travel Retail

Final Thoughts

After facing several quarters of plummeting air traffic, a recovery in passenger traffic, primarily driven by China, is expected to drive further growth for the airlines industry and Dufry, in particular. Its overhang on the Autogrill acquisition with respect to MTO is also behind and we believe the acquisition comes at a right time for it to enter into F&B market offering a broad assortment of solutions leveraging its scale and driving cross selling opportunities to the consumers. We believe the risk reward is favorable as a result of growth in passenger traffic, strong recovery in China, synergies from its Autogrill acquisition and comfortable leverage position. Initiate it at Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here