It was back in October of 2022 when Verastem (NASDAQ:VSTM) updated investors on their RAMP clinical trials, which included their recurrent low-grade serous ovarian cancer “LGSOC”, KRAS G12V-Mutant non-small cell lung cancer “NSCLC”, KRAS G12C-mutant NSCLC, and frontline metastatic pancreatic cancer. That update revealed that the combination of Avutometinib and Defactinib “did not meet the pre-defined criteria to continue in the RAMP 202 trial.” The market crushed VSTM’s share price in what seemed to be due to the fear that Avutometinib might be an ineffective oncology agent despite having the prospects to be a unique compound for KRAS cancers. I agreed with the market, and decided to mothball my VSTM while waiting for additional data that could “revitalize my thesis.” Well, Verastem delivered with their AMP 201 study data from the combination of Avutometinib and Fefactinib in LGSOC. The data revealed that the combination yielded an “objective response rate “ORR” of 45% and tumor shrinkage in 86% of evaluable patients.” In response, the market shot VSTM up over 200% as investors digested the data and its implications for the company. For me, the positive data was exactly what I was looking for, and I am now ready to take my VSTM position out of mothballs and revamp my strategy after the ticker’s recent 1-for-12 reverse stock split.

I intend to review the recent data updates and provide my opinion on how it will impact Verastem and its other pipeline programs. In addition, I will discuss why I am taking my VSTM position out of mothballs and how will attempt to navigate some of the looming downside risks. Finally, I will take a look at the post-reverse split chart to formulate a fresh strategy for VSTM as we head into the second half of 2023.

RAMP 201 Data

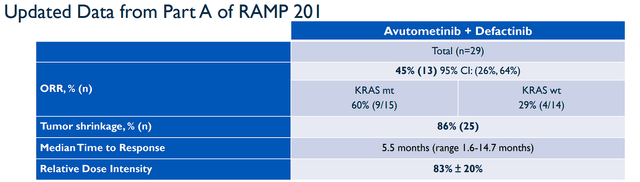

Verastem recently publicized updated data from the Part A portion of their registration-directed RAMP 201 Phase II trial of Avutometinib “VS-6766” as a monotherapy or in combination with Defactinib for LGSOC. The combination generated a 45% ORR and 86% of evaluable patients experienced tumor shrinkage with a median time to response was 5.5 months. It is important to note that study patients were “heavily pretreated with a median of 4 prior systemic regimens,” with some having 11 prior treatments counting platinum-based chemo, endocrine therapy, and bevacizumab. What is more, roughly 13% of patients had experienced MEK inhibitor therapy with 3 out of 4 of these patients responding to the study’s combination therapy. The KRAS mutant LGSOC patients had a 60% ORR for the combination arm. Meanwhile, the KRAS wild-type LGSOC ORR was 29%. Verastem reported that the “median duration of response and median progression-free survival have not been reached.”

RAMP 201 PART A-Data (Verastem)

What is more, the company reported that the study’s safety and tolerability were “favorable and consistent with previously reported data” with the most common treatment-related adverse events being mild to moderate nausea, vomiting, diarrhea, elevated CPK levels, peripheral edema, vision blurred, dermatitis acneiform rash, fatigue, and dry skin. This contributed to a 12% discontinuation rate in the trial overall to date.

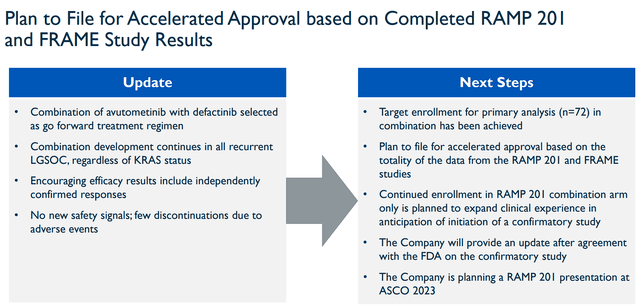

The company believes that this data supports the combination’s FDA Breakthrough Therapy Designation for recurrent LGSOC. In addition, the company is looking to file for Accelerated Approval.

Verastem Accelerated Approval Plan (Verastem)

RAMP 201 Implications

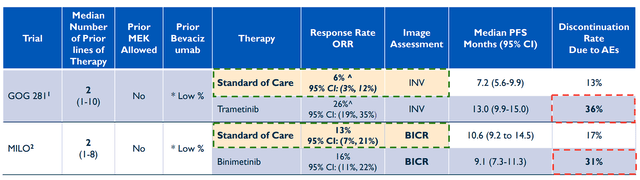

The RAMP 201 data is a significant event for Verastem and VSTM investors for a few reasons. The primary reason is obvious… the data revealed the combination elicited extensive tumor shrinkage in patients who had already tried and failed several treatment lines, with some trying failing MEK inhibitors. In addition, the company reported high response rates in patients with and without KRAS mutations. So, not only are we looking for a potential new treatment opportunity for this hard-to-treat cancer, but it is possible we are dealing with a new standard of care. In fact, the current treatment options in this cancer population have only yielded responses stretching from 0% to 26%.

Recent LGSOC Trials with Standard of Care (Verastem)

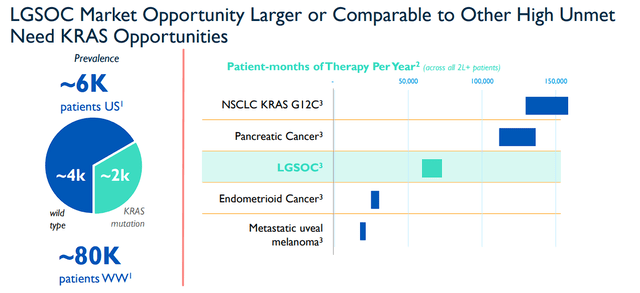

Meanwhile, current trials with of Avutometinib and Defactinib combo have consistently produced ORRs of ~45%. Moreover, it is important to note, there are no FDA-approved treatments for LGSOC, thus, making Verastem a potential leader and trailblazer in a sizeable market.

Verastem LGSOC Opportunity (Verastem)

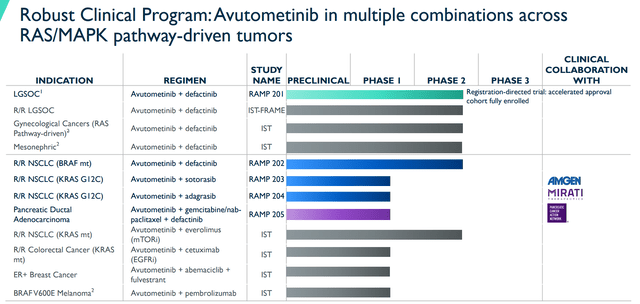

The RAMP 201 data also revitalized the outlook for the remaining RAMP pipeline programs. Remember, the company had disappointing data from their Part A data from the RAMP 202 trial with the combination of Avutometinib and Defactinib for KRAS G12V NSCLC. Verastem reported an 11% ORR with a disease control rate of 37% in KRAS mutations. In addition, the ORR with non-G12V KRAS mutations was only 5% with a disease control rate of 54%. As a result, the company determined the data “did not meet the pre-defined criteria to continue in the RAMP 202 trial.” This data put a dark cloud over the rest of Verastem’s pipeline programs, especially the RAMP programs that were targeting KRAS. Well, the 201 data bolstered my conviction around its prospects, as well RAMP 203, RAMP 204, and RAMP 205.

Verastem Avutometinib Combinations RAS/MAPK Tumors (Verastem)

Indeed, I am not going to claim that all of these studies are going to be successful and will lead to multiple FDA approvals. Then again, if Verastem can get Avutometinib across the finish line for LGSOC, the company would be in a position to quickly expand its label to other indications and lines of therapy.

Taking VSTM Out Of Mothballs… Again

As I already mentioned, I decided to mothball my VSTM position following the October sell-off because of my apprehensions that Avutometinib may well be a dud because it failed to show better results in the KRAS population in RAMP 202. Typically, I would have attempted a contrarian approach and looked for a trading opportunity following the sell-off, but the market conditions were less than ideal for this approach. So, I decided to put VSTM on the shelf and wait for another data readout to vindicate Avutometinib… RAMP 201 did that.

Following the RAMP 201 data, I attempted to perform a quick assessment to figure out a game plan to get off the sideline, however, the company decided to perform a reverse split, which often generates a period of elevated volatility. So, I have been hands-off waiting for the volatility to subside before clicking the buy button. However, I am drawing up plans for VSTM’s reactivation and return to the Compounding Healthcare “Bio Boom” Portfolio.

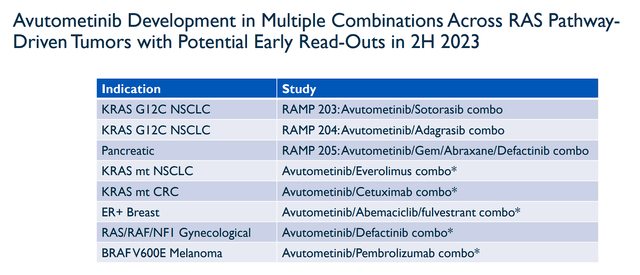

Before we get into the fine details of my reactivation strategy, I would like to go over why I am looking to expedite the process. The primary reason why I am looking to pull the trigger on a buy in the near term is due to some expected upcoming data from RAS-driven tumors in the second half of this year.

Verastem Combo Readouts 2H 2023 (Verastem)

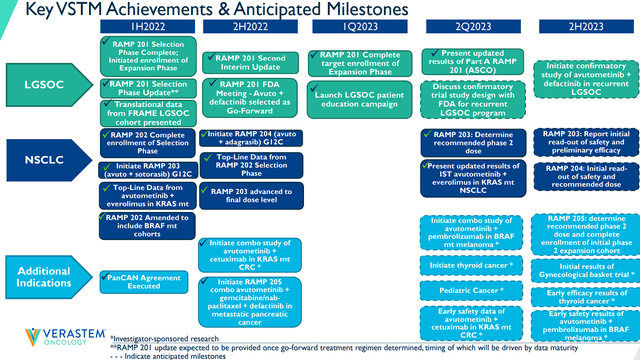

Verastem Achievements & Anticipated Milestones (Verastem)

Most of these expected readouts are investigator-sponsored trials, so, we don’t have a clear timeline for when we could see some data. Still, this is a solid list of potential catalysts that could reveal if Avutometinib has the potential to be operative in NSCLC, pancreatic cancer, CRC, breast cancer, gynecological cancers, and melanoma. Considering some of those are the largest oncology markets, I think we can agree that these data readouts could be potent catalysts that may move the share price to a higher trading range. VSTM’s market cap is only around $187M, so any positive readout might justify a much higher valuation considering all of these indications are multi-billion dollar markets. I think it is appropriate to expect VSTM’s perceived ceiling to rise for every positive readout and that ceiling should be much higher than a $187M market cap.

Now, there is the concern that the upcoming data readouts are lackluster and the company has to bail on those programs, which would bring the ceiling down. However, I believe the LGSOC indication alone is worthy of a higher valuation than $187M.

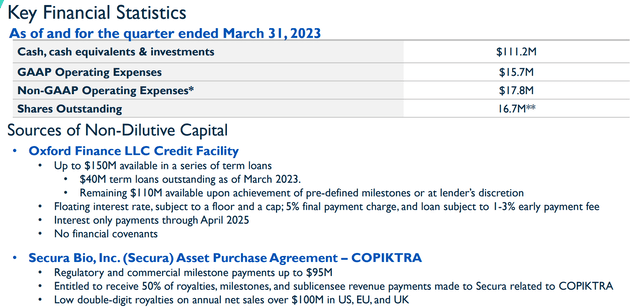

The other reason why I am willing to quickly jump back in on VSTM is the company’s current financial status. At the end of Q1, Verastem had $111.2M in cash, cash equivalents, and investments. In addition, they had up to $150M in term loans from Oxford Finance. Plus, the company has milestone and royalty payments from Secura Bio from the COPIKTRA deal.

Verastem Financial Highlights (Verastem)

What is more, the company’s recent GAAP OpEx was $15.7M, so I believe it is safe to say the company is not going to run out of cash in the immediate term. This should allow the company to hit some of these catalysts to hopefully drive up the share price, thus, allowing them to raise money at a higher valuation.

So at the minimum, Verastem has a promising opportunity to get Avutometinib quickly across the finish line for LGSOC with minimal dilution and start collecting some revenue in a mostly unclaimed market. Best case scenario… Verastem is able to report that Avutometinib is operative in several more cancers, and we are looking at a drug that could come close to hitting blockbuster status.

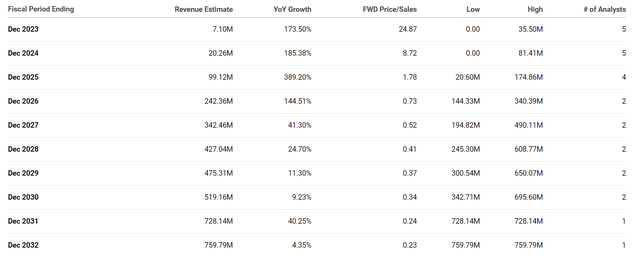

The Street expects Verastem to report strong triple-digit growth over the next several years. Certainly, these estimates clearly rely upon the company getting multiple programs on the market, so these projections are hypothetical.

Verastem Revenue Estimates (Seeking Alpha)

However, these revenue estimates do demonstrate how Verastem could go from pulling in just over $7M to over $700M in less than 10 years, which would be a roughly 0.2x-0.3x forward price-to-sales. The industry’s average price-to-sales is typically 4x-5x, so $700M in revenue would justify VSTM trading at around $200 per share towards the end of the decade. For that reason, we can say VSTM is trading a significant discount for its potential future revenue if everything works out. In addition, we have to expect the company will have to perform some fundraising over the remainder of the decade, so that estimate will drop in the coming years. Still, even if the company was to perform a few more offerings, the potential upside is immense. It is the primary reason why I never sold out of my position, and why I am looking to restart my accumulation.

Getting Off The Sideline

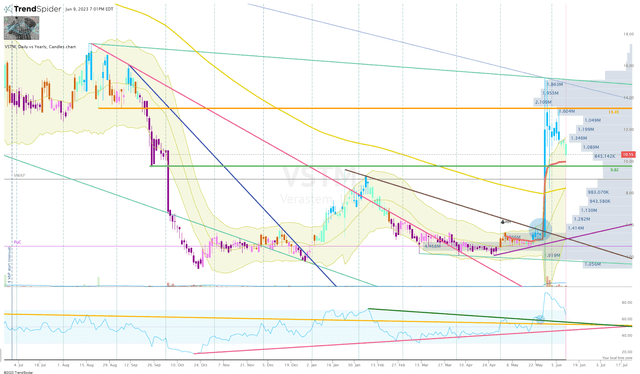

The hard part about getting off the sideline is really timing my first buy. Looking at the Daily Chart, we can see that VSTM has started to revert off the initial spike following the data readout. The chart is showing us a solid “cup-and-handle” and a “double-bottom” setup, which are considered pretty bullish formations. Both of these formations together can be a great multiplier because the double-bottom should provide strong support with the high of the formation being a great bounce target for the handle segment of the cup-and-handle setup.

VSTM Daily Chart (Trendspider)

The share price already tested this and bounced, but we are seeing the share price descend back to the $10 area where we have an anchored VWAP (Red Line) and some light support/resistance to provide as another bounce opportunity. This is where I will be eyeing my first buy, which would be minuscule in size. If the share price drops below the anchored VWAP, I will look for a test of the high of the double-bottom formation or potential bounce off the 200-Day EMA (Yellow Line) before clicking the buy button. Here, I would probably execute a larger buy order, due to the technical support below, plus, a more attractive valuation.

Navigating Downside Risks

Long-term, I am going stick to technical setups to rebuild my VSTM position over the second half of 2023. Although the recent data has reinvigorated my bullish outlook for VSTM, I have to concede this was not Phase III data, and the drug has come up short in another study. Therefore, I am going to remain cautiously optimistic until we see Avutometinib perform well in some other studies.

In addition, I have to point out that VSTM has a lot of risks that are endemic to small-cap biotech tickers that are moving deeper into development such as regulatory risks, increased cash burn, potential competition, etc. Verastem is a long way from the FDA finish line, so being patient and opportunistic in your accumulation is a necessity.

Overall, VSTM is still a very speculative ticker at this time. Therefore, I am moving VSTM back into the Compounding Healthcare Bio Boom portfolio with a conviction level of 2 out of 5.

Read the full article here