This is a follow-up to my previous coverage of ProPhase Labs (NASDAQ:PRPH); so I suggest new readers begin with my May 2022 article for more background.

As shown in the slide below (from the latest corporate presentation), PRPH has multiple business segments, two of which I’ll be focusing on in this article.

Corporate Presentation

Nebula Genomics

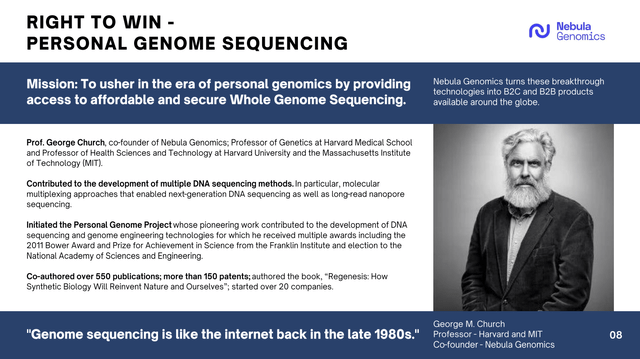

Nebula genomics is a division that was purchased by the company in 2021 with the aspiration of turning it into a low cost leader in genomic sequencing. The co-founder of Nebula is a highly decorated industry leader as outlined in the next slide.

Corporate Presentation

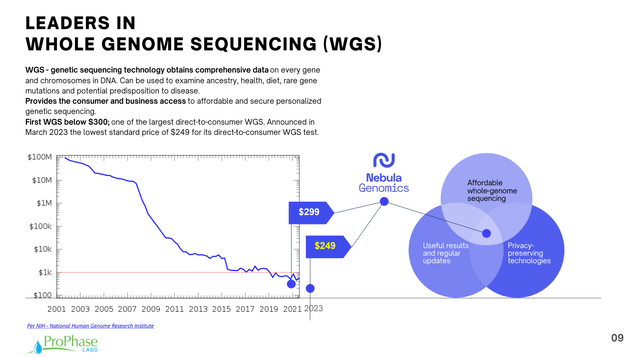

As with all thing technological, the price of genome sequencing has been declining rapidly over time, and Nebula is on the forefront of that movement. In particular, it recently announced a new low price of $249 for its direct-to-consumer whole genome sequencing test.

Corporate Presentation

And here’s what the CEO had to say about the future prospects of Nebula (recognize though that he’s very bombastic, so you have to temper most of his statements somewhat), with my emphasis:

[W}e anticipate building a very nice Nebula Genomics business the second half of this year, particularly in the fourth quarter. In the meantime, our revenues are running up more than 100% year over year anyway. So Nebula Genomics, understand there are similar businesses that are far behind us. We’re probably three to five years ahead of some of these other businesses. And yet, they have $50 million and $100 million market caps for these startup genomics businesses. And we believe that we are situated, well situated, to be the low cost provider of whole genome sequencing in the United States and potentially globally. So our Nebula Genomics business, again, right now, we’re only selling direct to consumers. We’re looking to leverage this business in the second half of this year. I don’t know when, but all of the — several of the major drug retailers are doing tests right now. The tests are going very well. And at some point I believe that we will get our whole genome sequencing test on store shelves like Walgreens and CVS and so forth.

[…]

[W]e expect to be the low cost provider of whole genome sequencing in this country. I believe that, that business is going to grow rapidly. So we are already growing 100% year-over-year. Just imagine the hockey stick acceleration of that growth when our B2B business starts. And of course, that’s in addition to retail stores. I’m happy in the Q&A, if you have specific questions about Nebula Genomics. It is a very valuable business and I’m looking forward to building it further. Again, we have world renowned experts, George Church and Russ Altman from Stanford University, George Church, of course is world renowned in genomics. They are on our advisory board. We talk to them regularly. We just had a call with them a couple of days ago, and they are really involved in helping us build this business, introducing us to global players in the genomics field. There is just enormous potential. This is where the Internet was 20, 25 years ago.

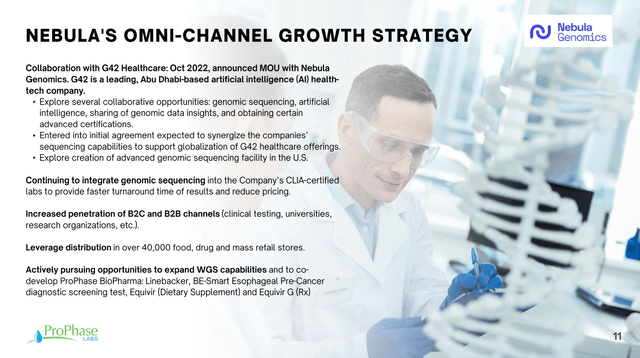

The details of moving beyond just direct to consumer are summarized in the following slide. The biggest company-specific advantage PRPH has in the expansion of target markets is its pre-existing relationship with 40,000 retail stores (by virtue of its earliest business line, TK Supplements). This should greatly accelerate a rollout of its whole genome testing capabilities.

Corporate Presentation

Prophase Diagnostics

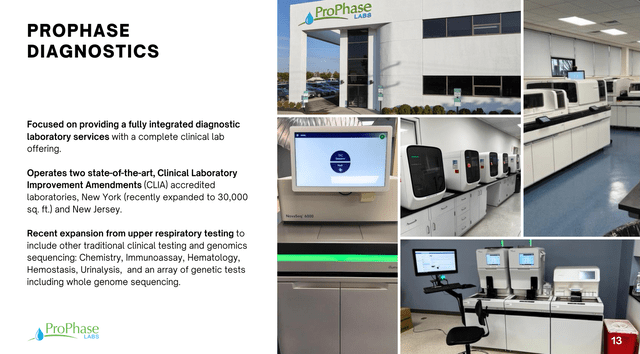

The second segment of PRPH’s business that I’m excited about is its diagnostic services. As readers of my previous articles know, it was the company’s entry into this realm during Covid that initially garnered my attention.

Corporate Presentation

But now that the company has built out its laboratory testing capabilities, and Covid is no longer a live issue, the focus of this division has changed.

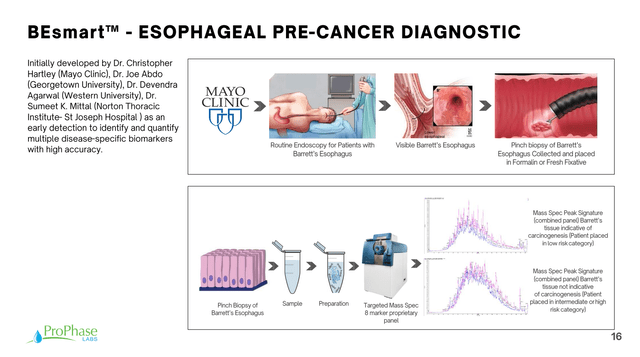

Now it’s on offering new tests, processed by the company’s built-out backend. In particular, there’s an emphasis on a new diagnostic test the company has developed to screen for esophageal cancer in pre-cancerous patients.

Corporate Presentation

There was a good discussion about this in the Q&A of the most recent earnings call, explaining how tissue specimens already collected during standard of care endoscopies could be used as specimens for this additional diagnostic test, and hence how it doesn’t become an extra burden to either patient or practitioner (with my emphasis and the same caveat as previously):

And with our test, understand our initial target market is just on people that are already getting the endoscopies. So we don’t have to sell them on getting an endoscopy, we don’t have to recommend it, we don’t need an institute recommending, we’re targeting patients who are already getting the endoscopies. All we’re doing is targeting the physicians to say, hey, you’re already doing this endoscopy. You already have seven, eight, nine specimens that you’re studying under a microscope, we need a sliver of one of those specimens, one of those tissue specimens is to study with our tests to give you much more accurate readings on whether or not your patient is developing esophageal cancer.

So we don’t necessarily need a huge sales force. What we need are the cancer institutions and key opinion leaders to get behind us and to make it well known to the community of physicians and GIs that they need this test. And that’s why we’re presenting at the major cancer conferences right now, and a lot of these conferences are very difficult to get into. But because our results are so fantastic, we’re being accepted to present. So we’re continually presenting at the cancer conferences. And so we’re just working on key opinion leaders and major cancer institutes get behind us. We’re working with world renowned institutes in this regard. We’re building up the recognition within the community and we’re going to continue to do that, while we hired an expert that’s going to get us a CPT code. So we’re doing all the right things in terms of the sales force, those are logistics that we’ll be developing throughout the course of the year. But understand the business is a little different, because we’re dealing with physicians, GIs, who are clearly going to hear about our test. I would say every GI in the country a year from now is going to know about our test.

And so we get the CPT codes, which allows reimbursement by insurance. We believe it’s going to be a no-brainer. How are GIs — if you have a test that can save your patient’s life, how is a GI not going to say, oh, let’s add this test on. We’re already doing the endoscopy, let’s add this test on. And what person who has esophageal cancer is scared to death of dying of esophageal cancer? What person isn’t going to want that test? Even if they paid cash for it? What person on the planet isn’t going to pay — I don’t care if you’re on welfare — if you had to, you could pay a $1,000 to $2,000. You could pay a $1,000 for a test to find out if you’re going to die with esophageal cancer. And you find out early enough you can do a simple ablation procedure to destroy the pre-cancer cells before they become cancer. So the dynamics of the business are a little different than Exact Sciences. I simply point out that, look at — the success of Exact Sciences when their sensitivity and specificity, which is the accuracy of — with false positives or false negatives is significantly less than the accuracy of our test. So all I’m simply suggesting is we have enormous potential and this is initial target market is on the patients that are already the GIs, are already recommending that they get the endoscopy. So we don’t need a cancer institute or anyone to recommend the endoscopy that’s already being done. All we’re doing is saying, hey, you’re already doing the endoscopy, why not do this simple test, which will give you much more accurate results.

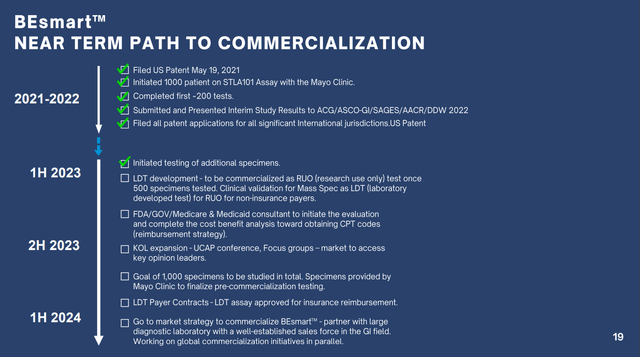

The company hopes to bring this test to market by the end of 2024 on the following development timeline:

Corporate Presentation

Market Opportunity

According to this 2021 study, there are about 7.5M upper endoscopies performed per year in the US. PRPH is targeting a $1K price per test, so even if it got 5% of the market, it would add a very meaningful $375M to the company’s annual topline.

Financial Performance

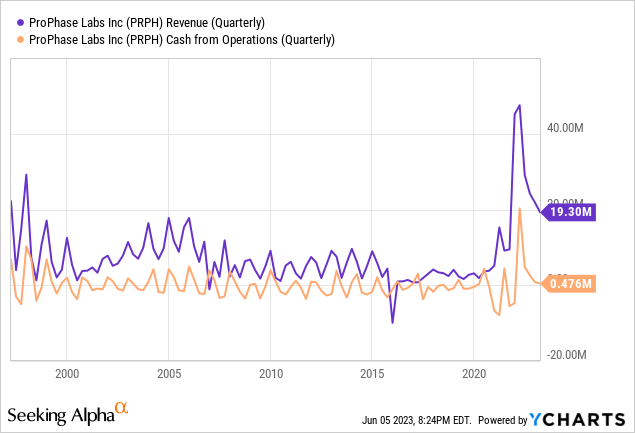

PRPH saw a massive jump in revenues and cash from operations during the Covid era, but revenues have now dropped, though they are still much higher than they were pre-Covid due to the new laboratory facilities and capabilities. The company expects to operate at a slight loss going forward until its esophageal test comes to market or its whole genome sequencing product takes off.

Cash on Hand

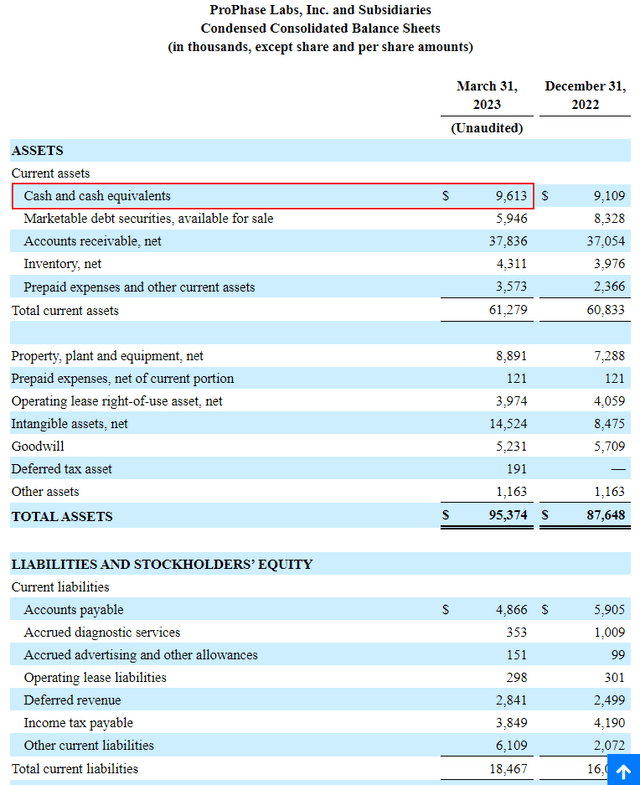

With a cash burn under $0.5M a quarter, PRPH has enough cash on hand to easily see it through the development of its new products and services. Thus the likelihood of a dilutive equity offering is relatively remote.

sec.gov

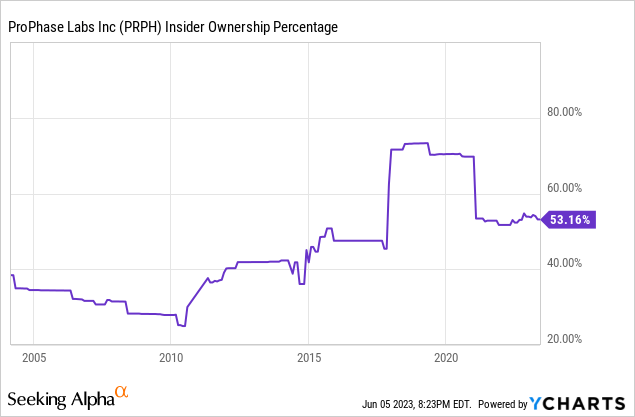

Insider Ownership

I find it reassuring to see such a large percentage of the company owned directly by insiders.

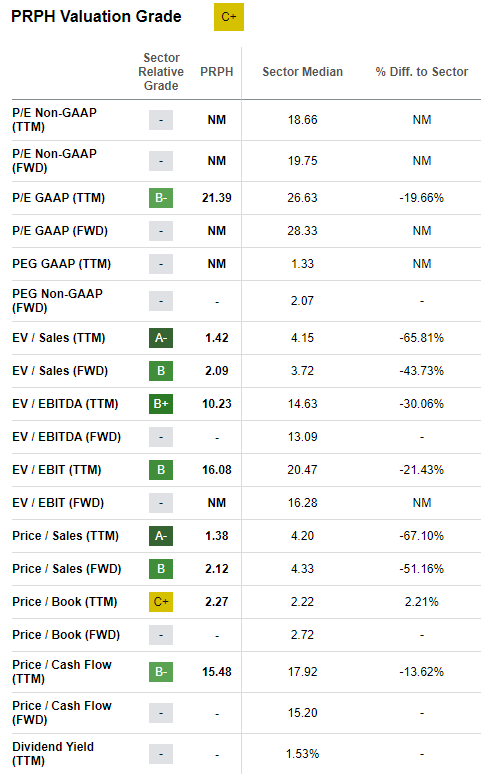

Valuation

With PRPH stock trading at $8.08 per share, the company offers an attractive valuation (despite getting a C+ grade from Seeking Alpha). Of course, once its new products are launched, these metrics should improve markedly.

Seeking Alpha

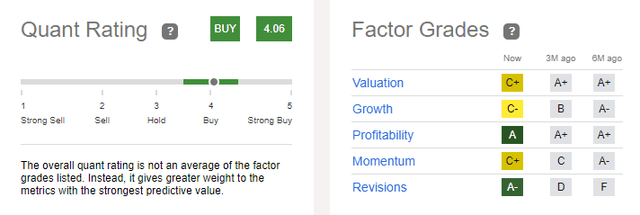

Quant Ratings

Seeking Alpha has the company as a Buy, which is just slightly lower than my rating of Strong Buy:

Seeking Alpha

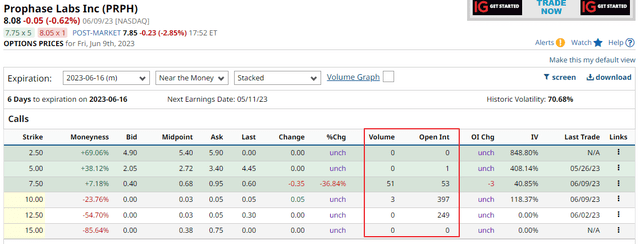

Options

PRPH trades options, and they are moderately liquid, so at times I use them to write OTM covered calls (which in my mind brings a bit of a yield to my holdings).

barchart.com

Risks

PRPH isn’t currently forecast to be profitable this year and for at least the first half of 2024. If progress is slow, or even worse, if validation for the new esophageal test fails and sales of the whole genome sequencing don’t ramp up, then the company will run out of cash by the end of next year. Moreover, as a small cap company (it currently has a market cap of $135M and an EV of $134M), it may find raising additional capital difficult in the new tighter money environment.

Summary

PRPH executed well during the Covid era and used its success to build out laboratory capabilities and to invest in new product lines. I am particularly excited about the whole genome sequencing and the development of a new esophageal test aimed at detecting cancers earlier than the current standard of care allows for. I am long a full position as a result.

Read the full article here