Global Payments Inc. (NYSE:GPN) is well positioned to benefit from the growth in the digital payments volumes and the secular trends in the e-commerce industry. The company is making the right moves towards realizing its strategic goals and during the first quarter, GPN completed an expected acquisition, aimed to strengthen its B2B presence, and disposed of the lower-margin consumer part of the business. With this, GPN’s prospects are becoming increasingly positive, but it will take time for the real strategic effects to manifest. I would recommend staying on Hold with GPN stock, while supervising some points mentioned in the article for a potential rating upgrade.

Outlook and financials

Digital transformation continues to gain momentum in the world’s economy and the payment solutions/software industry is one that can be automated and transferred to a cloud environment quite easily. Probably, everyone could identify in themselves a tendency to use a digital wallet for purchases more often than a physical one. This trend is increasingly positive for businesses as well, due to the convenient possibility to optimize internal processes and for cost management reasons. The unification of payment solutions; gradual displacement of bank cards in favor of virtual cards and accounts; integration of payment systems into cloud solutions/software; development of the existing payment methods – are factors that provide significant opportunities for Global Payments to drive future growth and expand its global payment footprint, as the company offers cloud payment solutions and software, and operates on a SaaS model.

The financial prosperity of GPN is closely tied to the development of the e-commerce industry, as the revenue from merchant solutions shapes a major part of the company’s top-line. As a result, the increase in the volume of online purchases and spread of BNPL services, along with the expansion of e-commerce, which is strongly related to the aforementioned trends of payments development, is playing into the hands of GPN.

Since the company entered the B2B payment segment, it gains a huge opportunity to earn revenue from processing transactions in the new addressable market. Moreover, the company strengthens its positions with the acquisition of EVO Payments, which could be even more beneficial in the long run after exploring the full synergies potential from the deal. Regarding the latter, the management expects to reinforce the company’s operating leverage notably by achieving a $125 million cost savings. In addition, the newcomer complements GPN’s business in terms of presence in international markets and countries with a great potential for growth, like Mexico, Poland, Greece, the Czech Republic, etc.

Financial results (company reports)

According to the results of the 1st quarter of 2023, the company increased its consolidated revenue by 6.3% YoY to $2.29 billion thanks to the growing volume of transactions and utilization of digital payments solutions. The Merchant Solutions segment registered a 9% YoY growth led by the ongoing strength of the company’s technology-enabled distribution channel.

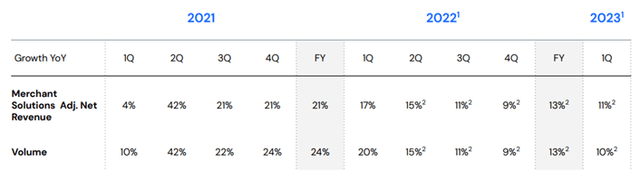

Merchant Solutions trends (company presentation)

Although the result of the main segment exhibited resilient growth, we should notice the slowdown in the transaction volume growth in the above table. Excluding the discontinued consumer part of the business and contribution from EVO, the segment’s revenue growth is estimated at 11% YoY. However, the deceleration pattern shouldn’t be much of a concern, in my view, amid changing consumer behavior post-pandemic and the recovery of the offline shopping, where businesses are exerting a high demand for POS solutions. In the Issuer Solutions segment, revenue grew by 6.2% YoY thanks to strong double-digit growth from commercial and consumer card transactions, as well as decent account growth.

Quarterly adjusted operating profit increased about 10% YoY to $882 million on a margin of 43.9% (+80bps YoY), as the company managed to control rising transaction costs and keep profitability resilient. Going down the P&L statement, the company reported an adjusted EPS of $2.40, compared to $2.07 in the corresponding period last year, and delivered a strong financial performance during the quarter on top of expectations.

Going further, the Global Payments business model is looking more attractive following the business combination activities closed in the first quarter. All these actions were up for concentration on providing services to corporations and work on a B2B business model, while completely moving away from the lower margin B2C business. In addition, the company updated its forecasts for FY2023, with the target range of adjusted revenue around $8.7 billion and up to 8% growth, which should come along with operating profitability gain of up to 120bps.

Risk factors

The result of an active M&A policy and external financing turned to a rather high debt load to Global Payments. However, the management provided for normalization of the debt levels following the deal for EVO. In addition, a scenario of recession could lower the transaction volume going through the company’s platform.

Investment takeaways

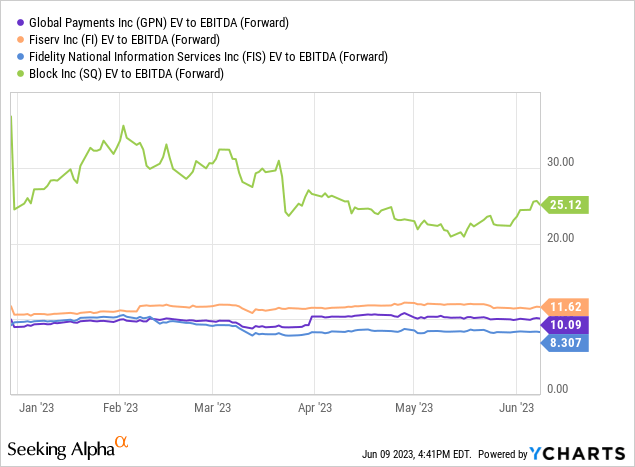

Turning to the valuation, it is reasonable to take a look at the EV/EBITDA multiple, as the company anticipates synergy effects from the EVO acquisition, and related operating efficiencies.

Global Payments is currently trading at a 10x EBITDA forward multiple, which is in line with the company’s close competitors in the face of Fiserv Inc. (FI) and Fidelity National Information Services (FIS). However, it doesn’t seem to me that the valuation is really incorporating the synergy effects, and the consolidation of GPN’s business model around the B2B segment. The reasoning for this could be that the real synergy effect from strategic business combination is quite difficult to estimate, and they also bring temporary integration-related costs. Add to that operating expense from the disposing of the consumer part of the business, which weighed noticeably on GAAP financial rations. As a result, I would recommend staying Hold on GPN stock at this stage, although it is lovely to see real steps in aligning the business model with the company’s strategic focus. Another pleasant point is that GNP is quite successful in resisting the turbulent macro environment, demonstrating a resilient financial performance. The company didn’t experience the effects of the collapse of regional banks thanks to the tie-up with a strong customer base. Moreover, the current “bad times” and elevated interest rates could be beneficial for the Global Payments’ active M&A activity to pick up the next target, since the valuation ratios are feeling the pressure.

But, going further, I would stay tuned on how the integration of EVO and the release of the consumer business are affecting operating profitability. According to executives from the earnings call:

We anticipate this impact to be mitigated by synergy realization as the year progresses. As a result, we are forecasting margin contraction in the second and third quarters and then margin expansion in Q4 as synergies ramped for our merchant business.

Thus, I believe that the potential for the rating upgrade would be the operating profitability surprise during the second and third quarters of 2023.

Read the full article here