Recovering Well

Oxford Industries, Inc. (NYSE:OXM) is a clothing and accessories company built on the market power of its name brands. Oxford’s revenue and earnings are growing. Margins and cash flows are excellent. Success follows a tumble of the share price in 2021 when the impact of the pandemic inspired lockdowns and supply chain problems. The company’s slow but steady growth was stymied.

We join the chorus of analysts bullish on OXM; this extends our favorable opinion of the apparel industry for retail investors.

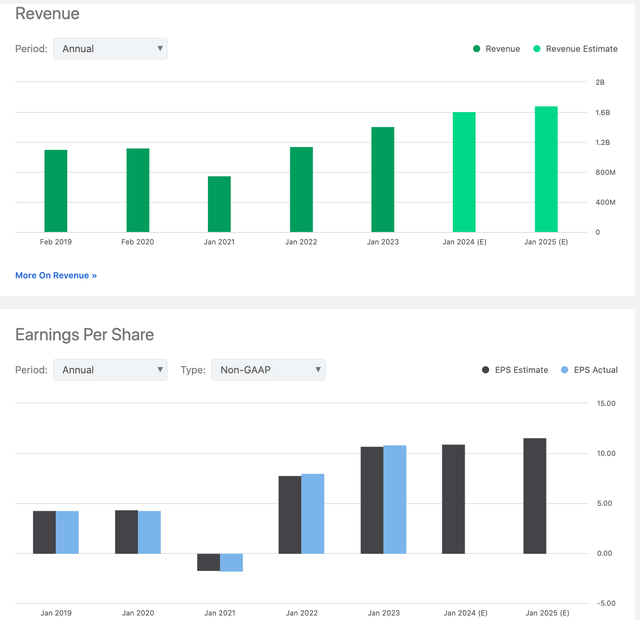

Revenue & Earnings OXM (seekingalpha.com/symbol/OXM)

The share price moved up to +$101 in mid-June, ’23. That is a mid-range between the 52-week low of $82 and the high of $123. The shares are up about 10% over 5 years including the last 12 months and YTD. The company’s revenue path follows that of the apparel industry; it grew 47% Y/Y in 2021 (see Oxford 2022) but 1.5% in 2019 (see Oxford 2020).

The 1.14 Levered Beta means retail value investors have to be patient and not sweat the frequent ups and downs, as the company follows a natural path to ROI.

M&A has not dominated financial growth. Oxford acquired just one business in the last 5 years, Johnny Was for $270M. The CEO attributes 14% of the company’s 19% growth in sales Y/Y to the acquisition of Johnny Was. The other 5 brands had 5% organic growth.

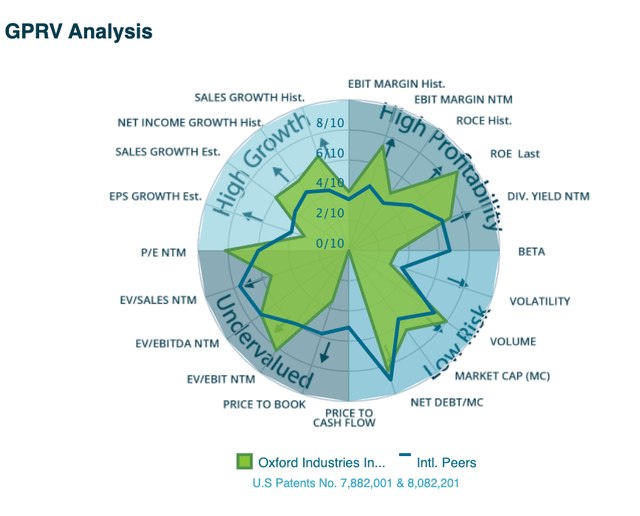

Risk Reward Assessment for Oxford (infrontanalytics.com/fe-en/US6914973093/Oxford-Industries-Inc-/market-valuation)

The Company

Oxford Industries, Inc., designs, sources, markets, and distributes clothing, shoes, and accessories by name brands worldwide. Manufacturing is outsourced.

The Tommy Bahama brand company offers men’s and women’s sportswear and related products. Oxford products include women’s and girl’s dresses and sportswear, scarves, bags, jewelry, and belts, as well as footwear and children’s apparel and swimwear under the Lilly Pulitzer brand. Wearables for men, women, and youth sell under the Southern Tide brand.

Oxford Industries Brands (oxfordinc.com/)

The company generates revenue from sales and licensing of Tommy Bahama and other brands. Products include indoor and outdoor furniture, beach chairs, bedding and bath linens, fabrics, leather goods and gifts, headwear, hosiery, sleepwear, shampoo, toiletries, fragrances, cigar accessories, distilled spirits, stationery and gift products, home furnishing products, and eyewear.

Oxford Industries, Inc. products sells through its retail stores, multi-branded e-commerce retailers, off-price retailers, and e-commerce sites. As of January 29, 2022, it operated 186 brand-specific full-price retail stores; 21 Tommy Bahama food and beverage locations; and 35 Tommy Bahama outlet stores.

Oxford Industries, Inc. was founded in 1942 and is headquartered in Atlanta, Georgia. Its market cap tops $1.6B.

Good Numbers

On Jun 7, ’23, the company reported Q1 ’23 revenue and EPS. Revenue of $420M was +19.1% Y/Y. EPS of $3.78 beat estimates. Q2 EPS is forecast to top $4. According to a Seeking Alpha summary, the company expects FY ’23

net sales in a range of $1.59 billion to $1.63 billion vs $1.64B Consensus as compared to net sales of $1.41 billion in fiscal 2022. GAAP EPS is expected to be between $10.18 and $10.58 compared to fiscal 2022 GAAP EPS of $10.19… For the second quarter of fiscal 2023, the Company expects net sales to be between $415 million and $435 million vs $440.60M Consensus compared to net sales of $363 million in the second quarter of fiscal 2022.

Quant & Other Factors

SA’s Quant Rating wavers between a Hold and Buy assessment. For most of the YTD, S A docked the stock a Hold, but since the last week in May ’23, SA’s Quant Rating moved toward a view of Buy to Strong Buy. S A Factor Grades for valuation, growth, and profitability were raised from 3 months before. Momentum weakened from A- to C+.

The PE is 9.22 which is lower than among clothing and accessories peers sporting a PE average of 12.55. Short interest is on the high side, up to +7.6%. The company’s 5-year average PE is 19.7. Based on the PE, Oxford Industries is in our opinion potentially a good value.

The share price is worth watching for timing a trade if the stock dips into the $90s, as it as earlier this year. Based on future revenue and earnings coupled with high employment and a growing economy, we expect the average price target is $115 to 4130 over the next 12 months. The Sector Relative Grades for metrics S A employs to gauge valuation are split between As and Cs.

The metrics include a C+ for the dividend yield of 2.28% when the industry yield average is 1.8%. The company has a low payout ratio of 21.7%, so the dividend is well-covered by earnings and cash flow.

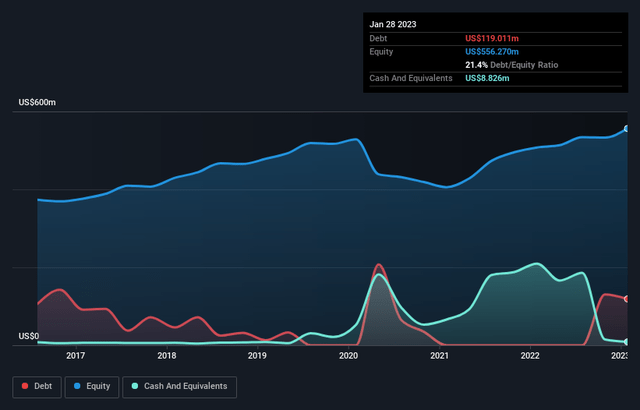

Oxford holds ~$617M in cash and equity; assets are about 2x liabilities. Company debt is $94.31M down from $119M at the end of the previous quarter. On average in recent quarters, the company’s free cash flow is more than 60% of its EBIT.

Debt & Equity (simplywall.st/stocks/us/consumer-durables/nyse-oxm/oxford-industries/news/is-oxford-industries-nyseoxm-using-too-much-debt)

Corporate insiders bought and sold shares over the last 12 months as the price rose and fell. Hedge funds bought shares in the last half of 2022, sold at the end of the year, and increased their holdings by 125.6K shares over the last quarter. Several hedge funds have sold their positions as the share price rose into the $90s. 11 funds held OXM in Q1 ’23 after a slew of funds bought in the $70 and $85 range.

Takeaway

In our more than four decades of retail and e-commerce experience, we know firsthand they are exhausting, expensive, and unpredictable paths to business success. Before deciding whether to invest in this industry and company, ponder the large number of retailers that disappeared over the centuries.

Another macro-risk to the investor is the near-total offshore manufacturing for the company, in order for management to concentrate on brand building and marketing. That leaves Oxford open to vagaries in foreign locations; for example, China’s repeated spot-lockdowns disrupt the supply chain; the spike in freight costs ate at profits or forced product price increases. These risks caused the stock to stumble and tumble in the past and must be assumed to exist in the future.

Oxford Industries, Inc. shares are relatively lightly traded. Only a few analysts follow the stock. However, the media coverage of Oxford is increasing and the sentiment is more positive than negative. Perhaps bullish sentiment for Oxford has to do with management’s commitment to quantifying current trends, consumers’ historical buying patterns, forecasting and replenishing inventories, and communicating with manufacturers to ensure correct manufacturing capacity, raw materials availability, and lead times.

All these factors resulted in 8 consecutive record quarters. Brand building is the essence of the company’s success. “Tommy Hilfiger’s product quality score is a 4.2 out of 5 as rated by its users and customers,” according to comparably.com. “Reviewers from the Consumer Goods industry rated Tommy Hilfiger’s product the highest.”

Brand building, excellent margins, stellar cash flows, and a coordinated collaborative relationship between segments of the company make for success and opportunities for growth. Business people know the value of the quip, dress for success. Dressing a retail value investor’s portfolio with Oxford Industries stock is likely to make for a successful long-term outcome.

Read the full article here