Okta Inc. (NASDAQ:OKTA) is a leading provider of cloud-based identity and access management solutions for businesses and developers. With a mission to connect people, technology, and community, Okta has established itself as a leader in the industry. At the core of Okta’s offerings is its cloud-based platform that enables users to authenticate, authorize, and secure access to applications, devices, and data from anywhere. By leveraging Okta’s solutions, businesses can ensure a seamless and secure user experience while maintaining control over their digital assets. The platform supports single sign-on, multi-factor authentication, API access management, and identity governance, among other features. Founded in 2009, the company has experienced significant growth and boasts an extensive customer base across various industries including energy, healthcare, retail, and technology.

I am impressed by Okta’s recent financial results and the positive outlook. However, there are concerns regarding the potential impact of current macroeconomic challenges on Okta’s business operations. These concerns have tempered the overall optimism and offset the positive momentum from recent earnings, and Wall Street downgrades have not helped the cause either. In a year that has so far been characterized by the comeback of tech stocks, Okta stock has disappointed investors with a gain of just 2.7% YTD. I believe a reversal of fortunes is on the cards based on recent earnings revision trends, but I remain wary of the company’s profitability profile.

The Impressive Financial Performance

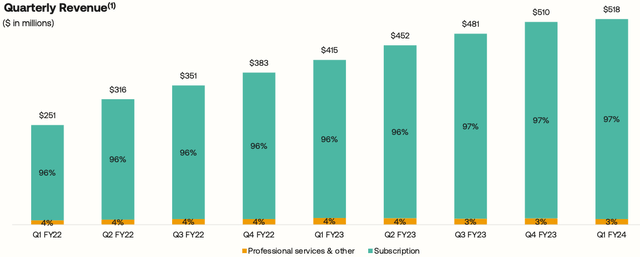

Okta’s recent financial results have exceeded market expectations, underscoring its strong position in the identity solutions industry. In the first quarter of fiscal year 2024, the company generated revenue of $518 million, representing year-over-year growth of 25%. This growth was primarily driven by a 26% increase in subscription revenue, which accounted for 97% of Okta’s total revenue. Additionally, international revenue saw 23% growth and contributed 21% to the total revenue. One key metric that demonstrates Okta’s strength is its subscription backlog, also known as RPO (Revenue Performance Obligation). RPO grew by 9% to reach $2.94 billion. Furthermore, the current RPO, which represents the subscription backlog expected to be recognized as revenue within the next 12 months, witnessed a substantial 20% increase to $1.7 billion. It is worth noting that the general shortening of term lengths in recently signed contracts impacted the overall RPO growth. Okta’s average term length for contracts is slightly over two and a half years. Okta’s improving financial performance is reflected in its improved net income figures. The company achieved a non-GAAP net income of $38 million, a significant improvement from the non-GAAP net loss of $43 million in the previous year.

Exhibit 1: Quarterly revenue

Earnings presentation

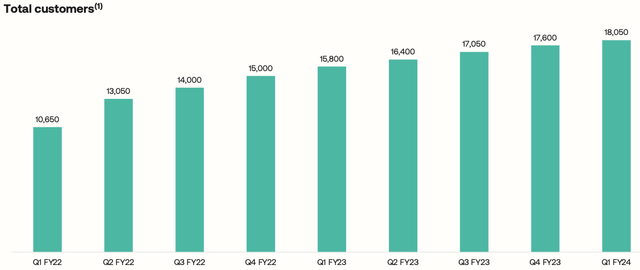

Customer acquisition and growth remain key focus areas for Okta. In the reported quarter, the company added 450 new customers, bringing the total customer base to over 18,000, representing growth of 14%. Although the challenging macro environment had its impact on new customer acquisitions, Okta experienced growth with large customers in both the Workforce and Customer Identity segments. Consequently, the company maintained healthy gross retention rates in the mid-90% range. The dollar-based net retention rate for the trailing 12-month period remained strong at 117%. However, there was a slight decline in the net retention rate sequentially, primarily due to a decrease in the upsell rate with both enterprise and SMB customers. Okta attributed this trend to customers refraining from expanding their seats at the same pace as in recent years, influenced by the current macro environment.

Exhibit 2: Total customers

Earnings presentation

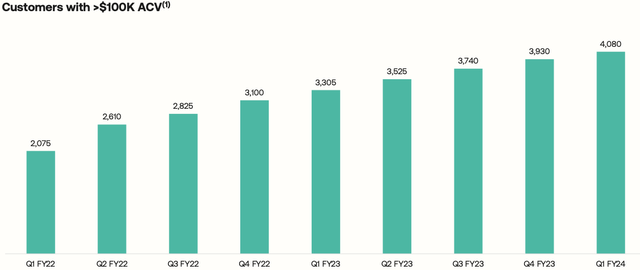

The company observed growth in customers with significant annual contract value (ACV). In Q1, the company added 150 customers with an ACV of $100,000 or more. Okta’s total base of customers with $100,000+ ACV now exceeds 4,080, reflecting growth of 23%. The fastest-growing customer cohort consists of over 300 customers with $1 million+ ACV, which has achieved growth of over 40%. The company’s balance sheet remains strong with Okta achieving a record free cash flow of $124 million in Q1 and a free cash flow margin of 24%.

Exhibit 3: Customers with $100k+ ACV

Earnings presentation

Despite the encouraging results in Q1, the company anticipates the impact of ongoing macroeconomic headwinds on its business operations to make the next few quarters a challenging period. In the areas of new business acquisitions across small and medium-sized businesses (SMBs) and the enterprise sector, Okta is experiencing increased macro headwinds. Similar to the previous quarter, customers are requesting shorter contract terms, leading to a higher proportion of upsells compared to new business acquisitions. As a result, the average deal sizes have become smaller. Additionally, customers are not expanding their seat capacities at the same rate as in previous years and this trend is expected to persist in the next few quarters. However, the company remains optimistic about its long-term growth potential, and Okta’s CEO, Todd McKinnon said:

A lot of macro uncertainty, but long-term, identity is going to be an important thing and we’re going to be there to serve the market.

For the second quarter, the company expects revenue between $533 million and $535 million, ahead of initial analyst expectations. Additionally, Okta raised its revenue guidance for the fiscal year 2024 to a range of $2.175 billion to $2.185 billion, indicating strong growth prospects even in a year where the company is facing macro headwinds.

Customer Wins

Okta already boasts an impressive roster of notable customers, including industry leaders like OpenAI. Okta’s Customer Identity Cloud serves as the authentication solution for ChatGPT, demonstrating the platform’s reliability and trustworthiness in handling user logins and ensuring a secure user experience. In Q1, the company secured additional notable customers including a business line of a Fortune 500 semiconductor company which acknowledged the limitations of its legacy technology that lacked adequate security measures. To address these issues, this semiconductor company chose Okta’s Workforce Identity Cloud to modernize its technology stack and handle multiple identity use cases. Additionally, Okta Identity Governance was selected to manage partner access to critical collaboration applications.

The seamless cross-selling between Okta’s Workforce Identity Cloud and Customer Identity Cloud was also evident through successful upsells with companies like Indeed and NerdWallet. Indeed, the world’s most visited job site initially used Okta’s Customer Identity Cloud for self-service customers and expanded its partnership to include Okta Workforce Identity Cloud including Okta Identity Governance, bolstering security and improving the user experience for its 13,000 employees. NerdWallet, one of the most popular personal finance websites in the world, began leveraging Okta’s Workforce Identity Cloud in 2017 and added Okta Identity Governance for compliance processes last year. In Q1, NerdWallet replaced its homegrown Customer Identity Solution with Okta’s Customer Identity Cloud, further demonstrating the growth of Okta’s product suite within its customers.

Okta recently achieved a significant milestone after receiving the U.S. Federal Risk and Authorization Management Program (FedRAMP) High Authorization for Okta for Government High. This modern identity platform is specifically designed for the U.S. Federal government and its mission partners. Okta for Government High serves as a secure identity solution that enables federal agencies to meet their stringent security requirements. It adheres to over 420 baseline security controls, ensuring the secure handling of mission-critical information.

These recent customer wins highlight the long runway for growth available for the company as many of its customers embrace additional products and solutions offered by Okta.

Product Advancements

Okta made significant advancements to its Workforce Identity Cloud in Q1, enhancing its offerings for customers. One notable advancement was the improvements made to Okta FastPass, which provides advanced phishing resistance to every user, regardless of device or operating system, enabling users to have a seamless experience without the need for passwords.

Another notable achievement was the continued adoption of the Okta Identity Engine (OIE). Over 40% of Okta’s workforce customers have transitioned to OIE, thanks to its inclusion in every new workforce customer deployment since early 2022. The company also introduced self-service OIE upgrades, streamlining the upgrade process and paving the way for more customers to experience the benefits of OIE.

Additionally, Okta is currently beta testing Okta Privileged Access, which extends secure access management and identity governance capabilities to privileged resources. This allows businesses to centrally manage policies and controls for modern cloud infrastructure such as AWS, EC2, and Kubernetes. The company expects this product to be generally available by the end of the year.

On the Customer Identity front, Okta leveraged its extensive logins and security event data to develop Security Center, a real-time insights dashboard for potential security attacks. This feature provides security teams with timely information to respond effectively and protect against threats in today’s complex technology landscape.

Technology Partnership Developments

Okta continues to forge strategic technology partnerships to offer innovative solutions and strengthen security. Last month, Okta announced an expanded go-to-market alliance with Alphabet Inc (GOOG), enabling Google’s Workspaces global and public sector sellers to co-sell Okta’s Workforce Identity Cloud alongside Google Workspace. This collaboration aligns the strengths of both companies, promoting a best-of-breed approach to security and productivity.

Another notable partnership was established with Zoom Video Communications (ZM), introducing Okta Authentication for end-to-end encrypted meetings for joint customers. By leveraging Okta’s authentication capabilities, meeting hosts can verify the identities of participants, ensuring secure and trusted online interactions.

Recognizing the importance of channel partners, Okta unveiled the Elevate partner program, designed to recognize and reward partners for their contributions across the entire value spectrum, from finding and developing opportunities to delivering and managing Okta solutions.

The Industry Outlook

The global identity and access management market is experiencing significant growth, driven by various factors shaping the modern business landscape. With the rise of cyber threats and data breaches, organizations are increasingly prioritizing cybersecurity measures, making IAM solutions indispensable. The market size for IAM reached $15.93 billion in 2022, and it is projected to witness a compounded annual growth rate of 12.6% from 2023 to 2030, according to Grand View Research.

Regulatory compliance requirements, such as GDPR and CCPA are compelling organizations to implement robust IAM solutions to manage user access, privacy, and consent effectively. The accelerated adoption of remote work models and BYOD – Bring Your Own Device – practices necessitates IAM solutions that ensure secure access and protect sensitive data in distributed work environments. Additionally, the growth of cloud computing and SaaS applications has driven the need for IAM solutions that enable seamless and secure access to cloud-based resources.

In this thriving market, Okta holds a unique position as a leading provider of cloud-based IAM solutions. During an earnings call, management emphasized the company’s commitment to being a neutral and independent partner in the identity management space. Unlike some competitors that bundle identity security with application offerings, Okta’s approach provides customers with the freedom to choose the best technology solutions without being locked into a specific vendor. The company believes this independent and neutral choice will give Okta a competitive edge against major platform providers like Microsoft Corporation (MSFT), ensuring its long-term success.

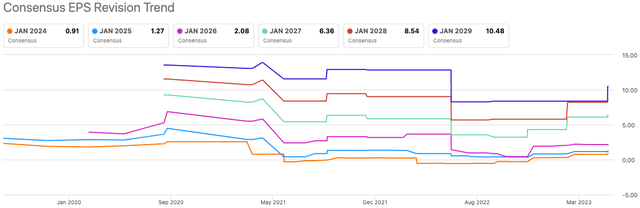

Earnings Revisions May Trigger A Reversal In Fortunes

Despite recent downgrades by JP Morgan and BMO Capital, earnings expectations for the upcoming fiscal year have trended higher in the last three months. At Beat Billions, we believe positive earnings revisions will act as a catalyst driving stock prices higher in most instances. I believe this positive trend is likely to gather pace in the second half of this year aided by the increasing appeal of Okta’s security solutions amid a multi-year global digital transformation where companies of every size and scale are forced to embrace digital trends.

Exhibit 4: EPS revisions

Seeking Alpha

With the company yet to break through to profitability, Okta is not cheaply valued. This is an area of concern for me although the company’s Q1 results suggest Okta is well and truly inching closer to breakeven.

Takeaway

Identity management remains a critical aspect in today’s digital landscape. Okta’s differentiated approach to identity management, coupled with its commitment to providing comprehensive and scalable solutions, positions the company for continued growth and solidifies its reputation as a trusted leader in the industry. Despite a challenging macroeconomic environment, the company has demonstrated remarkable resilience and substantial progress. Although I am yet to be convinced to invest in Okta stock today (since investing is not just about finding growth stocks but also about allocating assets strategically while maintaining a diversified portfolio), I believe Okta stock is gearing up for a reversal in fortunes where the stock could break into a positive trend.

Read the full article here