Investment thesis

Our current investment thesis is:

- Although RL has a strong brand, the company has faced increased competition, contributing to slowing demand and tightening margins.

- We do believe current fashion trends are favorable to RL but this is not a concern long term. Trends change but RL has shown itself to be resilient and adaptable.

Company description

Ralph Lauren Corporation (NYSE:RL) designs, markets, and distributes lifestyle products globally.

Their offerings include a wide range of apparel for men, women, and children, as well as footwear, accessories, and leather goods such as handbags and belts. The company also provides home products like furniture, bedding, and tableware, along with fragrances.

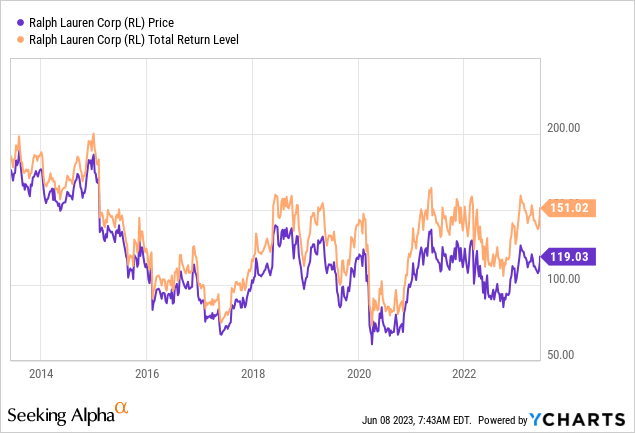

Share price

RL’s share price has declined in the last decade, reflecting a period of difficulty for the company. This is a reflection of changing industry dynamics and increased competition.

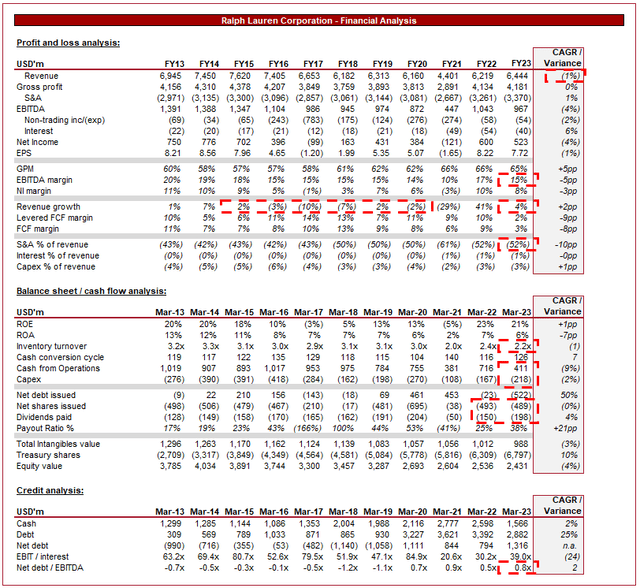

Financial analysis

Ralph Lauren – Financials (Tikr Terminal)

Presented above is RL’s financial performance for the last decade.

Revenue & Commercial Factors

RL’s revenue performance has been poor, with a decline at a rate of (1)% per annum.

RL is very much a lifestyle brand, creating a quintessential all-American design philosophy, focusing on both design and quality. Despite the nature of changing trends in the fashion industry, RL has remained at the forefront of fashion for many decades. This has been achieved by staying true to its ideals while leaning into changing market trends. There is also an argument to suggest its designs are evergreen, with its quality highly valued by consumers.

RL operates its own stores, as well as wholesaling and distribution through third parties. It is a truly global brand, reaching heights arguably no US fashion house has.

The fashion industry has experienced many trends in the last decade which have impacted the business, both positively and negatively.

We have seen a significant shift towards e-commerce retailing, as consumers are increasingly using technology and are demanding convenience. We believe this to have been an issue for many of the traditional brands, as the cost of entry into the market has significantly reduced. No longer do brands need to fight for retail space in stores. Further, e-commerce has contributed to aggressive pricing, as the lack of overhead costs (owning and running store locations) has contributed to further investment in customer acquisition. RL has developed its online capabilities but we see this more as a defensive move and has not materially improved the business.

Further, we have seen the rise of fast fashion. Fast fashion is the concept of creating similar designs to trendy products quickly and at affordable prices. We are currently in a social media era where people increasingly are homogenizing around what is popular, which has contributed to the increased demand for fast fashion. This has been a major issue for traditional brands such as RL who have stayed committed to their design philosophies.

To combat these threats, we have seen traditional retailers develop their value proposition. Taking an omnichannel retail approach is one key way. The integration of online and offline channels has become crucial. The objective is to create a seamless shopping experience for customers across various touchpoints. An example of this is shopping online but picking up /trying on in store, which reduces the time commitment of delivery and returns.

The fashion industry has also experienced changing consumer trends and behaviors.

As we touched on previously, the rise of social media platforms has transformed the way brands connect with consumers. It is increasingly valuable for brands themselves to interact with consumers, reducing the value provided by retailers. RL continues to market well to its core demographic through Instagram and adjacent outlets, but on TikTok for example, its impressions are low. This could create difficulties in attracting the younger generation.

Further, the slowing demand in the last decade could just be due to a change in popularity. Streetwear and athleisure have become dominant fashion trends, blurring the lines between sportswear and casualwear. RL has been adapting to this shift by incorporating streetwear-inspired elements and athletic influences into its collections but this is not sufficient. RL is known for its layers, denim, and shirts. The two do not marry well and this is evident. The issue for investors is that fashion is cyclical and so it is inevitable that brands will face periods of softening demand. This said, we do not think there is a fundamental risk to RL, the brand is far too large.

We also see opportunities for RL in the coming years to improve growth.

As a global brand, RL is an inspirational brand in many countries. Continued economic development represents opportunities for global expansion, particularly in emerging markets with a growing middle class and increasing disposable income.

Further, direct-to-consumer retailing is a key area of strength. This has become a legitimate expansion strategy due to a number of factors named above, such as increased e-commerce and brand marketing to consumers. The benefit here is that RL cut the middleman’s margin out, allowing for increased revenue and margins.

If we compare RL’s growth to other Apparel, Accessories and Luxury Goods (Utilizing SA’s quant rating tool), the company underperforms. Its 5Y revenue growth is only 0.83%, far below the average of 5.85%.

Moat

The unique offer with RL is its brand. Due to the longevity of the brand thus far, we are not concerned by a potential sustained decline.

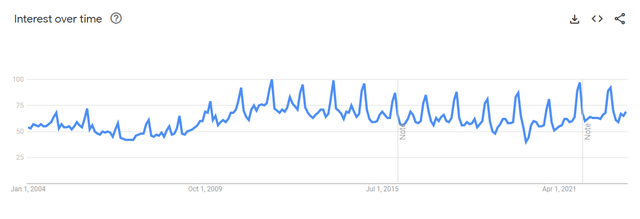

As the following illustrates, the interest in “Ralph Lauren” remains strong and if anything, has improved in the last 2 years.

Brand interest (Google Trends)

The key message from our commercial analysis is that RL’s revenue slowdown, and decline in some periods, is a reflection of increased competition and changing consumer trends. We do not think RL will experience a sustained decline but it is too early to say growth has fully returned.

Economic & External Consideration

Current economic conditions represent a risk to RL’s near-term performance. With heightened inflation, we are seeing consumers reduce their discretionary spending. For this reason, there is a slowdown in retail spending.

We believe inflation will continue to decline in the coming quarters, but improved trading will not occur until we see expansionary monetary policy return.

Margins

RL has an EBITDA-M of 15% and a NIM of 8%. Margins have declined across the historical period, reflecting increased competition (and so greater discounting and less ability to increase prices) and cost inflation.

RL has been unable to wholly pass on cost increases, as well as offset the decline through increased direct-to-consumer selling. GPM has improved, with c.5% gains in the last 10 years, suggesting the increased DTC and scale economies are working, but this is clearly not sufficient.

Further, S&A spending as a % of revenue has increased from 43% of revenue in FY13 to 52% in FY23, reflecting a large degree of operating cost expansion during a period of revenue stagnation. The concern here is that RL’s marketing spending is declining in effectiveness.

If we compare RL’s margins to others in the industry, we note the average EBITDA-M of profitable companies (#30) is 15.7%, which is marginally above RL’s level. Despite the margin slippage, this is a relatively good performance, with primarily premium brands exceeding the business.

Balance sheet

Inventory turnover has declined in the most recent period, implying the revenue slowdown was more than expected. Management should target the c.3x level achieved prior, which should assist with improving RL’s cash position.

RL is conservatively financed, with a ND/EBITDA ratio of 0.8x. This gives the company flexibility to raise debt if required, although historically this does not look to Management’s objective.

Valuation

Valuation (Tikr Terminal)

RL is currently trading at 9.4x LTM EBITDA and 8.5x NTM EBITDA. This is in line with the company’s historical average. During this period, RL has struggled to achieve consistent growth and has faced sliding margins.

Based on our analysis of the business, RL’s struggles stem from increased competition and changing trends. These factors have developed throughout the decade and are not overcome in our view. For example, RL is not materially different financially from its position in FY19, 4 years previously. For this reason, we believe the company remains adequately valued based on how markets view this company.

Final thoughts

RL is a highly popular global brand. The company has stayed true to its design identity while innovating. From an absolute perspective, RL’s financial profile is attractive (good margins and scale) but relative to the past, the company is slipping. Increased competition and the inevitable change in trends have impacted the business. We see potential in the business and if sustainable growth can return, we see value here.

Currently, however, the company looks appropriately valued based on its financial profile.

Read the full article here