The internet world does not only revolve around businesses, work, and investments. Seeking one’s perfect match is what millions of people wish for. And that’s exactly what Match Group, Inc. (NASDAQ:MTCH). For a few years, it has ruled the dating niche with its popular apps like Tinder and Hinge. However, the picture is different today as it faces fiercer competition in the market. Dating apps are more prolific these days, making it difficult for Match to maintain its market share. Thankfully, it maintains a decent performance amidst macroeconomic volatility. Its financial positioning remains sound, helping it sustain its capacity and capital returns. Meanwhile, the stock price stays at its low point. We understand the market apprehension due to stiff competition. Yet, it is a good bargain, given the potential opportunities in Tinder. And if the end goal does not materialize, the price still appears reasonable.

Company Performance

In 2012, Match Group, Inc. revolutionized the online dating market with the release of Tinder. With simple swiping, users can look up other users they like to talk to and eventually meet in person. The company became more of a staple during the pandemic. In 2020, Tinder set the highest record for the most daily activities, with about three billion swipes. Today, Match Group continues to lead the market, but it faces risks associated with the entry of smaller competitors.

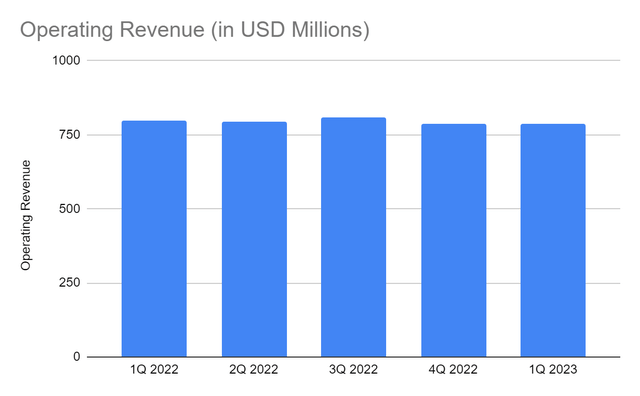

Also, the highly cyclical and volatile global economy impacted its most recent performance. It started the year with its operating revenue of $787.12 million, a 1% year-over-year decrease. We can attribute it to the -$35 million impact of forex. It was 25% higher than its expectations in the previous quarter. Despite this, the decrease rate remained flat, showing the strategies of the company. Most importantly, revenues without the forex impact would have reached $822 million.

Operating Revenue (MarketWatch)

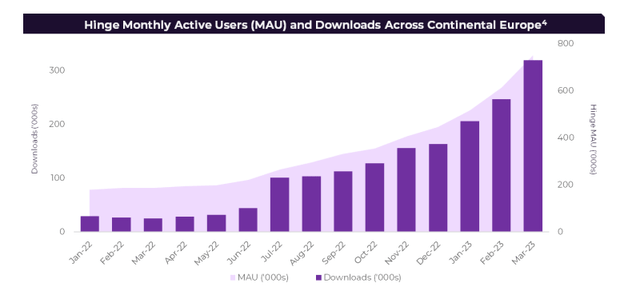

Tinder remains the jewel of the crown, comprising 56% of the total revenue. It remained almost flat at $441 million, an increase of less than 1%. We can attribute it to the decrease in paying subscribers, offset by the increase in subscription fees. With that, its pricing strategies helped cushion the impact of softer demand. Meanwhile, Hinge was only 11% of the total revenue. Yet, it became the primary growth driver of Match. Its revenues of $82.8 million was a 27% increase from 1Q 2022. The substantial increase in its payers and RPP of $25 contributed to its double-digit growth. Indeed, it was an impressive trend for a company of its size amidst the dating app wars. The upward momentum was most visible in Europe. In the past year, it showed a consistent increase in the number of active monthly users. In France, it ranked second for the most-used dating app only two months after its release. Given this, Match Group has two solid brands in its portfolio.

Hinge Monthly Active Users (MTCH Shareholders Letter)

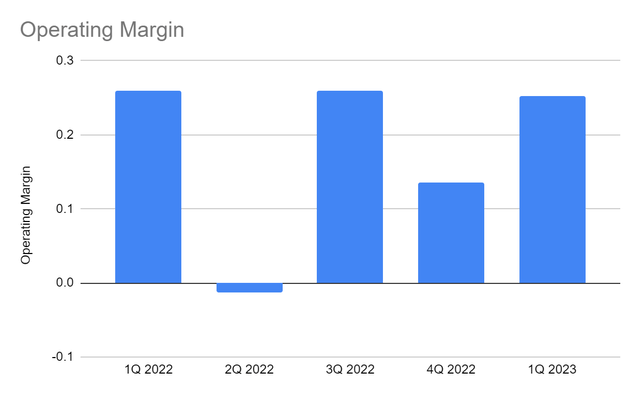

But what made Match secure was its efficient asset management. Its operating costs increased by only 1%. On the other hand, the operating expenses decreased by 2%. Their combined amount of $588 million decreased from 1Q 2022. They also partially offset the $11 million decrease in revenues. Although their impact was lower than that of revenues, they demonstrated the efficient variable and fixed cost management of the company. The operating margin was 25%, lower than in 1Q 2022 with 26%. Yet, it was a substantial rebound from 4Q 2022 with only 13%. The sequential trend of revenues, costs, and expenses was favorable for the company. It showed that it has already coped with the volatile economy and tough market with its pricing strategies and operational efficiency.

Operating Margin (MarketWatch)

Risks

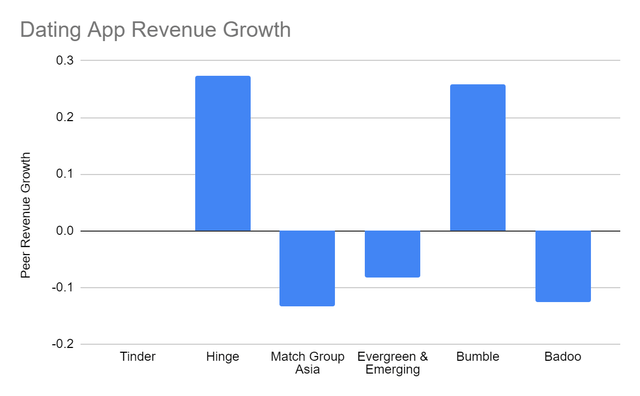

Match Group, Inc. maintains a solid market standing. It remains at the top of the list as Tinder remains the top choice across regions. Yet, it must not be complacent due to the increased market competition. Bumble remains the primary threat to its performance. During its IPO in 2021, Bumble had 2.4 million paying users. In 1Q 2022, the number exceeded three million. In 1Q 2023, it reached 3.46 million, a 15% increase. The Bumble app remains way smaller than Tinder when it comes to the number of paying users. But the sustained increase shows it can go head-to-head with a giant. Also, Bumble reported an RPP of $27.93 versus $13.80 on Tinder. It shows that Bumble generated more returns from its users than Tinder. The increasing number of subscribers and pricing strategies led to a 26% increase in revenues. Its other app, Badoo, had a 7% decrease in subscribers and an RPP of $12.47. On average, Match had an RPP of $16.26 while Bumble had $22.73.

Dating App Revenue Growth (MTCH And BMBL 1Q )

Another risk is the limited entry barrier. As more people engage in online dating, apps are becoming prolific. The business model and app features of Match are easy to emulate. With that, Match must capitalize on branding and product differentiation. The consolation is that Tinder has already stood the test of time. It remains a favorite across regions, so its customer base remains solid.

It must also watch out for interest rate hikes. We saw how interest rate hikes led to forex fluctuations, which had an unfavorable impact on revenues. Also, interest rate hikes mean higher borrowing costs. Match heavily relies on borrowings, which are equivalent to 91% of the total assets. Thankfully, none of them will mature this year. Even so, it must be careful since it can raise interest expenses. So, bottom-line earnings may decrease.

Why Match Group, Inc. May Stay Solid This Year

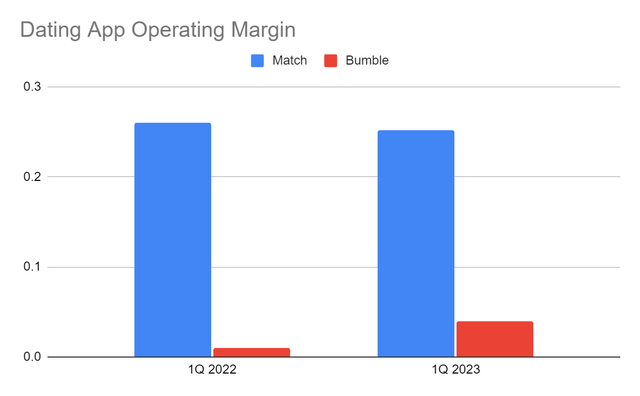

Despite the stiff competition with Bumble, Match Group, Inc. remains a force to reckon with. It may have lower RPPs, but it knows how to utilize revenues better. It is more viable than Bumble, showing better variable and fixed cost management. Its operating margin of 25% is way better than Bumble with only 5%. It can also capitalize on Hinge, which is now the primary growth driver. It has an RPP of $25. Even better, it maintains its solid standing in English-speaking countries while establishing itself in Europe. In Germany, it ranks third on the most downloaded apps. There is also a sustained uptrend in its monthly users in the region. It is an emerging app that has yet to utilize its potential.

Dating App Operating Margin (MTCH And BMBL 1Q)

It may also see hope on the horizon as it focuses on reestablishing Tinder. It works on improving its features to enhance user experience. It makes continued improvements in its key areas, namely user experience, deeper engagement, monetization, and price optimization. Enhancing user privacy and women’s experience are some of its goals. In a study, the majority of women said privacy remained a primary concern for them. As such, enhancing women’s experience and reintroducing its Incognito Mode can be pivotal for the success of its plan. This move can help Match regain previous users, retain the active ones, and capture new ones. Most importantly, it is a reasonable step for the company to secure its market positioning. It is also realistic since Tinder realizes increasing returns. It is a new hope, given the massive increase in subscription revenues from 1Q 2023.

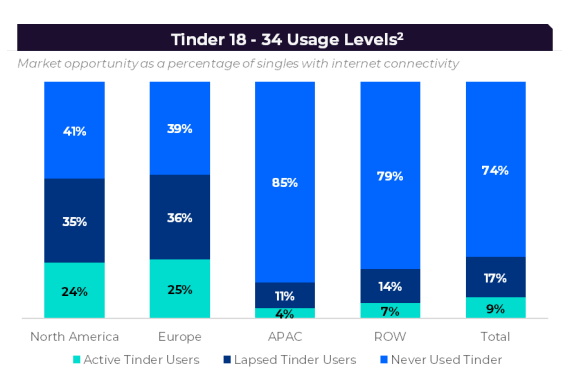

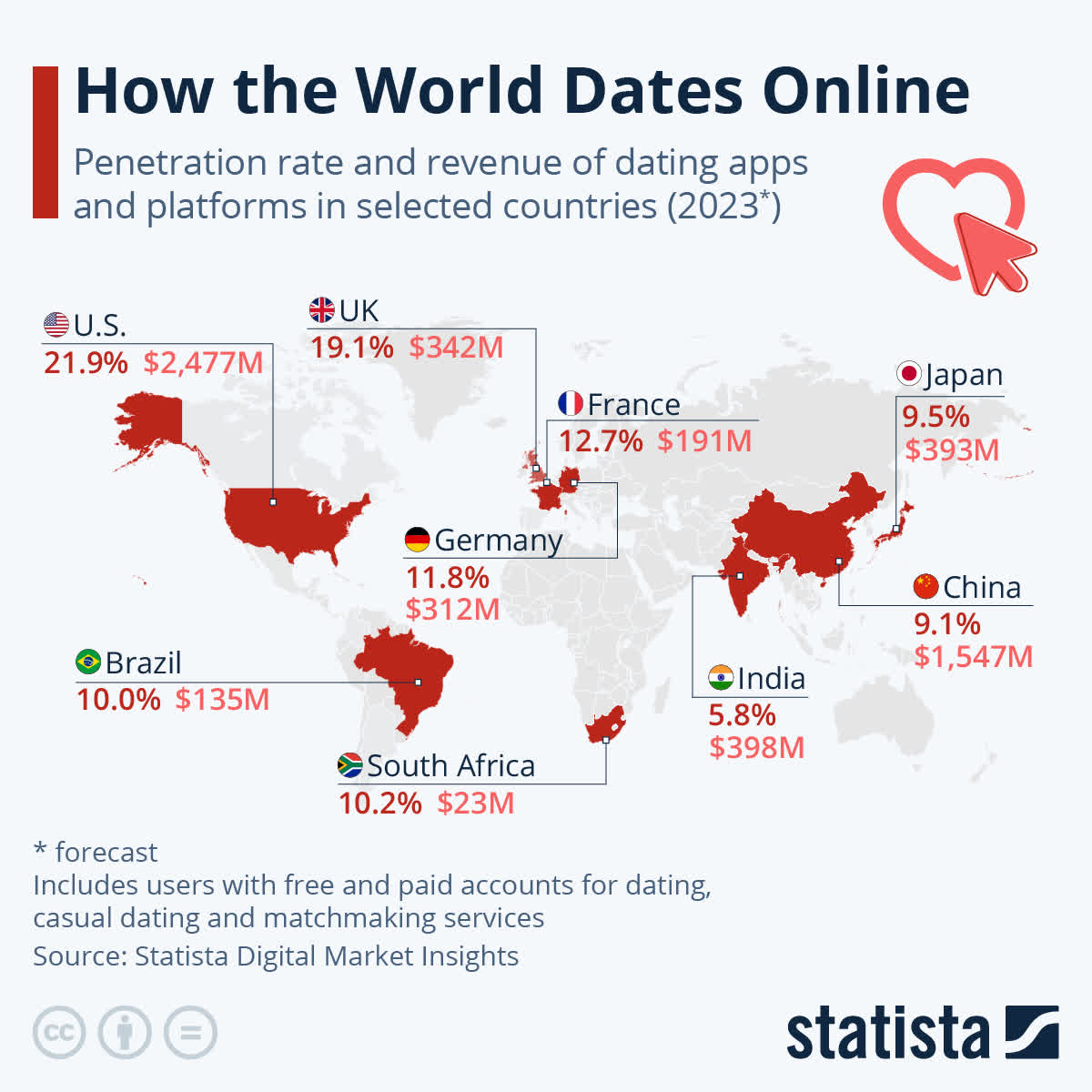

Also, there is still enough room to expand. As of its most recent report, it has not yet penetrated 74% of the global market. It is consistent with the estimates of Statista on the online dating market penetration rate. With that, innovation and enhanced marketing may be fruitful. It can generate increasing returns if the company completes its Tinder roadmap.

Tinder Usage (MTCH Shareholders Letter)

Infographic: How The World Dates Online (Statista )

Moreover, inflation has already relaxed at 4.9%, a 46% drop from the 9.1% peak in 2022. While prices stay elevated, lower inflation means more stable purchasing power. It can increase customer confidence and discretionary spending, boosting revenue growth. Match may have a better grip on its operations to stabilize costs, expenses, and margins. The decrease in inflation can even flatten interest rate hikes, which can help maintain borrowing levels.

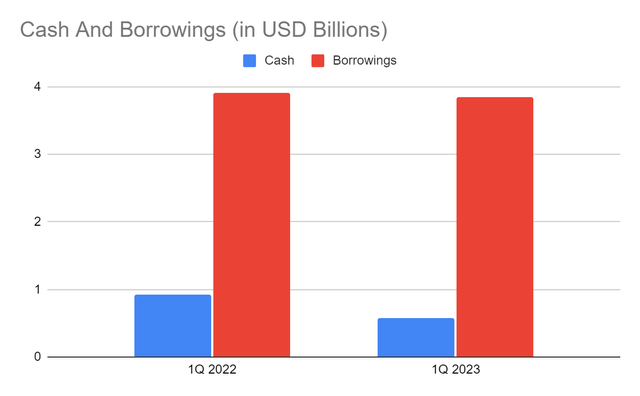

But what makes Match a secure company is its decent financial positioning. Cash levels remain adequate for its operating capacity and share repurchases. The only thing that worries me is the noticeable cash burn of $340 million from 1Q 2022 or $28 million per month. The current cash reserves can only cover two years of operations. But of course, that is if the company does not generate earnings. Thankfully, it has enough earnings to cover its borrowing repayments. Its Net Debt/EBITDA Ratio remains decent at 3.5x. Also, no borrowings have current maturities. So, it can focus on enhancing its apps and target more users. We can confirm it in the Cash Flow Statement. The movement of cash can be reflected by the lower cash inflows from operations. CapEx remains low since Match is not capital-intensive. With an FCF/Sales Ratio of 13%, Match continues to convert a substantial revenue portion into cash. The company maintains the balance between viability and sustainability.

Cash And Equivalents And BS Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Match Group, Inc. has been in a downtrend. It took a nosedive in 2021 and stayed at its trough since then. At $38.97, the stock price is 54% lower than last year’s value. Despite this, the massive cut makes it a good bargain. The PE Ratio conveys undervaluation, given the PE multiple of 32.44x and NASDAQ EPS estimates of $2.02. It gives a target price of $64.50, so investors may be comfortable even if the Tinder turnaround does not materialize. The EV Model confirms it, given the target price of ($14.43 B EV – $0.34 Net Debt) / 278,398,000 shares = $50.47. Moreover, Match sustains capital returns through share repurchases. In 1Q 2023, it repurchased 2.6 million shares for $112.5 million. Investment returns are also decent using the cumulative EPS and the average stock price change since its separation from IAC (IAC). It had a cumulative EPS of $4.68 while the average stock price change was $4.9. It means that for every $1 EPS, the stock price increased by $1.05, or 5% stock price returns. To assess the stock price better, we will use the DCF Model.

FCFF $898,000,000

Cash $578,450,000

Borrowings $3,840,000,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 278,398,000

Stock Price $38.97 Match Derived Value $55.48

The derived value adheres to the supposition of a potential undervaluation. There may be a 42% upside in the next 12-18 months. Investors may see this opportunity to buy shares at a discount.

Bottomline

Match Group, Inc. remains the leading dating app brand despite the fierce market competition. It maintains a solid performance with well-balanced revenues and margins. It also has a decent financial positioning to suffice its operating capacity, Tinder reestablishment, and potential expansion. Even better, the stock price is undervalued with enticing upside potential. The recommendation is that Match Group, Inc. is a buy.

Read the full article here