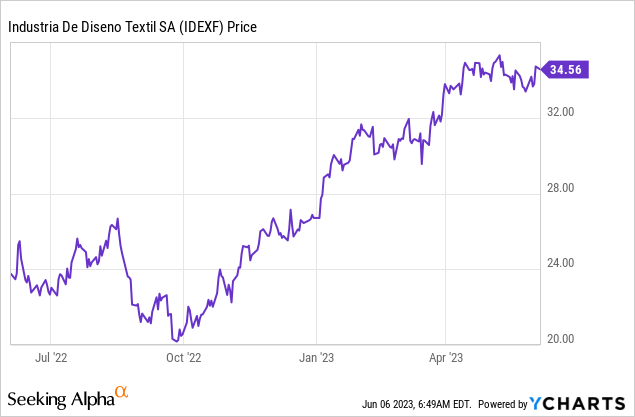

Since I last covered the stock, Inditex (OTCPK:IDEXF), the leading European apparel retailer (primarily through its Zara format), has been a clear winner. If recent commentary is any indication, the company again looks poised for a strong showing in Q1 (scheduled for release this week) – per management at the full-year results, the company was already off to a strong start to the Spring/Summer season, with store and online sales (FX-neutral) up 13.5% (+17.5% excluding Russia/Ukraine) through early-March. The top-line momentum may slow later in the year, however, given seasonal headwinds (e.g., a warmer than usual March/April in Southern Europe), and thus, I wouldn’t pencil in further upside to the EPS outlook just yet. Also concerning are the ongoing wage pressures in Europe, along with elevated inventory levels in the region; further markdowns pose a downside risk to earnings.

Over the mid to long-term, maintaining growth at similar unit economics will be a major hurdle as well – Inditex pulling back on square footage in China and Russia means the company will lose a key driver of growth in recent years, with store expansion in the US likely insufficient to offset the shortfall. At ~20x fwd earnings (~18x excluding the EUR10bn cash position), the stock is pricey and will likely lag an eventual EU retail recovery.

Defying the EU Retail Challenges

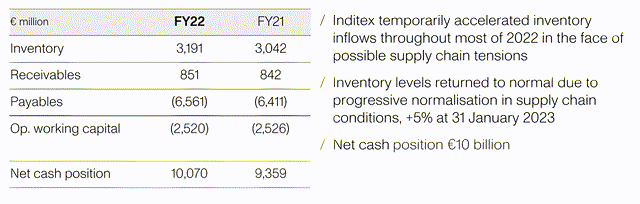

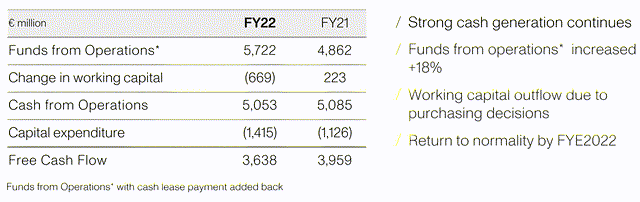

Inditex has executed well in a challenging retail environment – Q4 sales came in at EUR9.5bn (+13% Y/Y), helped by seasonal tailwinds from Black Friday/Cyber Monday and a colder-than-usual December. Pricing has also been solid, with Inditex running at an implied double-digits percentage rate (store sales up 23%, productivity up in the high-teens) despite inventory issues across the industry. Supported by supply chain normalization, inventory at Inditex has also stabilized at +5% as of fiscal year-end, allowing for a negative working capital position (long payable days vs. receivables) and a robust net cash position of EUR10bn. Management execution has also been commendable through a challenging consumer environment; even in a scenario where the traffic mix shifts back toward in-store channels in the coming months, multichannel retailers like Inditex should do fine.

Inditex

Building on the strong Q4, the company has started the fiscal 2023 year strongly, delivering +13.5% growth over the six-week period through early March (+17.5% ex-Russia/Ukraine). Hence, all signs point to the Inditex operating model continuing to work in this environment, outperforming its industry peers. More concerning to me are the factors outside of its control, including European consumer weakness in the face of sticky high-single-digit inflation throughout the Eurozone and their impact on the retail demand environment for the year ahead. Last year also benefited from the release of pent-up demand for outdoor/formal wear categories (areas of strength for Inditex) following on/off COVID restrictions – these tailwinds won’t recur this year, presenting tougher YoY comparables. Hence, I would be cautious about underwriting too much upside based on the early Q1 traction. With management also raising the annual capex guidance to EUR1.6bn, Inditex’s net cash growth will likely slow as well this year.

Inditex

Uncertain Mid to Long-Term Growth Path Amid Narrower Runway

The only negative from Inditex’s full-year results was the step-up in capex to EUR1.3bn, as well as the updated 2023/2024 guidance of EUR1.6bn/year. Management didn’t break out the specifics of the capex allocation, though, other than that the “bulk of the CAPEX we are referring to today is going to the stores.” Whether this means more gross new store openings or refurbishments is unclear; outside of the store, I would also expect higher logistics and tech spending to take up capex dollars. Growth will be necessary – Russia and China have long been touted as key growth markets, so the mass store closures over the last year (515 store closures in Russia and 86 in China per Inditex disclosures) are negatives for the top-line outlook. Any decline in square footage would represent a reversal of the aggressive store opening (and streamlining based on unit economics) playbook that worked so well in recent years. Alongside strong management execution, this has allowed for attractive store productivity and returns on capital, as well as overall cash conversion through the cycles.

From here, Inditex management will shift its focus to the US as the key mid-term growth driver (+3% gross net space growth targeted through 2025). The target of ten additional stores in the US probably won’t fully offset the shortfall left by the Russia and China closures, though most projects in the pipeline are related to store enhancements vs. new openings. Hence, I would underwrite a moderate mid-term growth outlook from here as Inditex pivots toward a slower store and space growth algorithm. While the higher EUR1.6bn of capex should be easily funded by internal cash flows, the ROI on this spending is unclear. Pending signs of an improved earnings growth runway, I would be wary of paying a high-teens P/E (ex-cash) to own the stock.

Inditex

Best-In-Class Retailer Priced at a Premium

All signs point to a strong result for Inditex at its Q1 result this week, as the company looks poised to extend its February/March momentum (+17.5% ex-Ukraine/Russia). While this could mean upward revisions to the consensus EPS algorithm for the full year, it remains early days, and I would be cautious about getting too carried away just yet. For the stock to work, it still needs to overcome numerous hurdles – over the near and long term. On the revenue side, seasonality is an issue (mainly weather-related), while on the cost side, pressures from higher wages and potential markdowns as inventory levels normalize throughout the European retail sector are key concerns. Zooming out, it remains unclear if Inditex can maintain the attractive unit economics of recent years without the growth momentum in Russia and China (net closures in both countries). For an EU retailer, the stock isn’t cheap at a high-teens ex-cash P/E valuation and might lag over penalized names like Zalando (OTCPK:ZLNDY) in a recovery scenario.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here