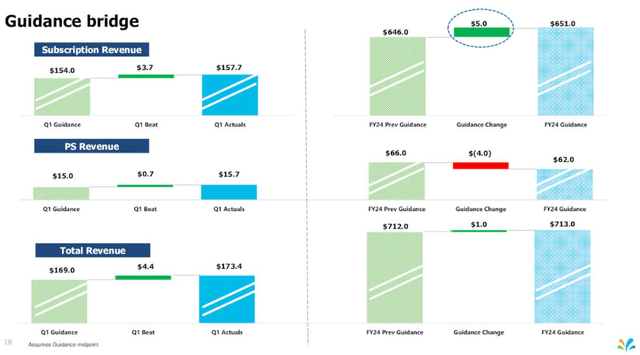

Sprinklr (NYSE:CXM) reported strong fiscal Q1 2024 results, beating revenue and EPS estimates, and it increased the full-year subscription revenue guidance by $5 million at mid-point.

However, the total revenue guidance was increased by only $1 million at the mid-point as the company continues to optimize its low-margin services business, where it now expects lower revenue in fiscal 2024 – $62 million instead of $66 million previously. Given the negligible margins of this business (9% gross margin in fiscal Q1 2024), this is not really a cause for concern and the health of the subscription business is most important to track.

The guidance for fiscal Q2 was in line with the Street consensus at the mid-point and this is somewhat surprising considering the Q1 beat but reflects the likely ongoing management conservatism and a $2 million revenue benefit that accrued in the first quarter instead of the second quarter. So, adjusted for $2 million, the fiscal Q1 still looks healthy and there would have been decent sequential growth in fiscal Q2.

Below is the guidance bridge from the earnings presentation that shows the assumptions and changes to expectations.

Sprinklr investor presentation

Total RPO (Remaining Performance Obligations) and cRPO (current RPO) declined slightly sequentially, but the declines reflect the upcoming big contract removals in the second quarter that are not included in these calculations. Both RPO and cRPO are up a healthy 23% and 19% over the same quarter of fiscal 2023.

Expenses as a percentage of revenue did increase sequentially, but reflect the sales and marketing activities at the start of the fiscal year, and there were also some costs related to the small restructuring the company did in February. But those expectations were also well-managed, and the company still beat the fiscal Q1 non-GAAP EPS consensus by $0.05.

The company now expects even stronger margin improvements this year, and they are reflected in the fiscal Q2 2024 EPS guidance of $0.04-$0.05 versus the $0.03 consensus and the increased full-year non-GAAP EPS guidance, from $0.13-$0.15 to $0.19-$0.21, or a $10 million increase at the mid-point of the guidance range. The increase in the full-year EPS guidance range is well above the $1 million increase in the total revenue guidance and also above the $5 million increase in subscription revenue guidance, as it carries much higher margins than the services business.

Management comments on the earnings call about the macro conditions were generally consistent with prior quarters.

As you heard today, long-term demand trends and engagement for Sprinklr remains strong. However, we recognize that the macroeconomic environment continues to be uncertain and our current assumption is that the broader macro trends from the last few quarters are likely to continue throughout FY 2024.

To that end, the company is still seeing increased deal scrutiny, careful and measured spending, and it takes more people to approve deals, and it also takes longer to close them. But there was no worsening on that side, and if the economy improves, we could see subscription revenue growth re-accelerate. But that is a big if and unlikely in the next few quarters from where we stand today.

The company is pleased with the attention generative AI is receiving and its Sprinklr AI+ solution includes generative AI capabilities through OpenAI integration across its product suite, which it believes makes its own AI even more powerful. You can go over the earnings call transcript and see examples of how new customers, such as the large manufacturer Hilti, have improved their processes and how existing customers such as Americana and Roche are expanding the use of Sprinklr solutions. Another notable mention was an unnamed top-five global technology company that renewed and expanded its business with Sprinklr to over $15 million in ARR. They are now using 40 Sprinklr products in over 13 languages.

Overall, the subscription business is humming despite weak macro conditions, and the company looks well-positioned to grow better than it guided for fiscal 2024.

What does it all mean for the share price in the near and medium term?

I think the fiscal Q1 results are supportive of my previous thesis – that the combination of strong business momentum and an attractive valuation put Sprinklr in a good position to trend higher in the following months and quarters, absent a big market correction. Subscription revenue growth of 22-23% in fiscal 2024 I outlined as a possibility versus the initial guidance for 18% growth at the mid-point of the guidance range, and the current guidance for 19% growth is well within reach.

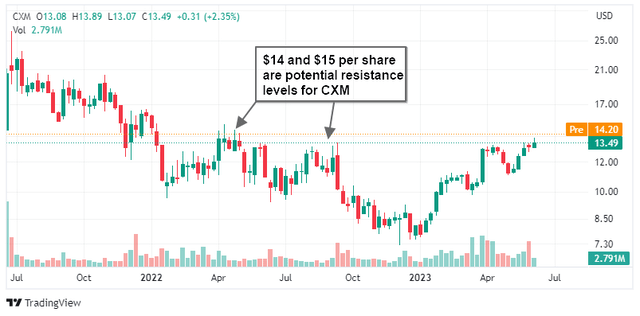

And looking at the chart, the stock made progress recently, and it now needs to overcome resistance around $14 and $15 per share.

Seeking Alpha, TradingView, author’s annotations

The key risks for the stock in the near term are worsening macro conditions spilling over to the equity markets and putting pressure on the stock, and the company missing revenue and EPS estimates in the following quarters or providing guidance that is worse than the Street consensus.

Read the full article here