Investment Thesis

Stem, Inc. (NYSE:STEM) is a clean energy solutions provider. The stock is down more than 60% from the highs set this year, and down even more from its all-time highs.

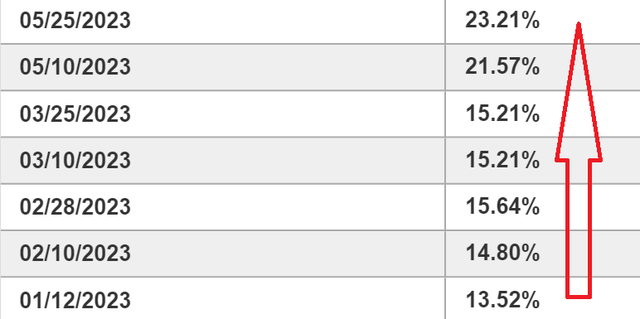

In fact, the stock is heavily shorted, with approximately 23% of its shares sold short.

Benzinga, short interest

Moreover, it appears that this shorted stock has perhaps become too crowded. And I believe this poses a problem. It’s not that shorts are totally wrong on Stem. There are substantial reasons to be short this stock, particularly given its unimpressive GAAP gross margin profile.

However, my contention is that shorts are not sufficiently weighing up the risk-reward of staying short right now.

Because, as you’ll soon see, there’s actually a business turning around here and striving to reach EBITDA profitability starting in H2 2023.

Why Stem? Why Now?

Stem specializes in energy storage solutions. They provide digitally connected systems and services that help manage energy storage, using AI. Stem designs energy storage systems, which aim to reduce energy costs. At its core, Stem is a hardware-selling business, with razor-thin margins. And that is something that shorts have been clinging to.

On the other hand, there’s a lot to like about Stem’s recent progress. Consider what Stem’s CEO John Carrington said on the Q1 earnings call:

We reported another new record for contracted backlog, which was up 120% year-over-year, driven by strong first quarter 2023 bookings.

We expect bookings growth to continue through the year as customers are increasingly standardizing on the Athena platform.

Simply put, Stem’s prospects could be set to improve.

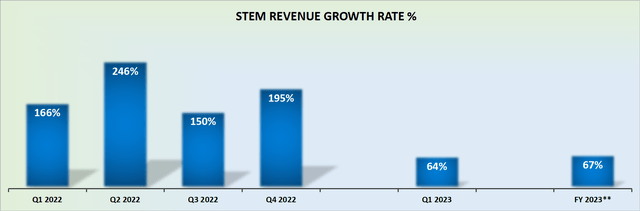

Revenue Growth Rates Set To Reaccelerate

STEM revenue growth rates

Stem’s prospects are very nuanced, with both good and bad elements.

Stem’s revenue growth rates for Q1 2023 were up 64% y/y, which is a significant deceleration from the exit rate in Q4 2022.

That being said, Stem has once again reaffirmed its guidance, and states that the full-year revenues should grow by around 67% y/y relative to 2022.

Typically, this would be a pretty terrific growth rate, but once you consider that 2022 saw its revenues increase by more than 180% y/y, this guidance leaves a lot to be desired. However, I urge readers to consider the following:

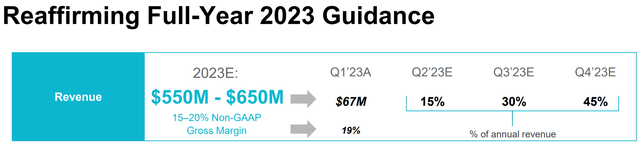

STEM Q1 2023

What we see above is that Q4 is expected to see around 45% of its total revenues for this year. This would mean that Stem expects around $270 million in revenues in Q4.

And if that revenue would materialize in Q4, this would imply that its revenues will increase by approximately 75% y/y. In other words, this would mean that Stem’s revenue growth rates are not fizzling out. But actually stabilizing. And doing so at a very high rate of growth.

That’s the good news. Now, let’s address the bearish thesis.

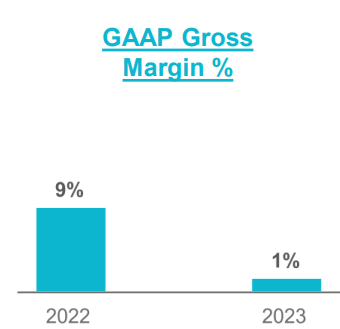

The Business is Simply Not Profitable

This is what the bears are encircling and putting forth, that Stem is not a viable business. Case in point, Stem’s GAAP gross margins stand a razor-thin 1%.

STEM Q1 2023

Stem makes the case that going forward its backlog of orders will be executed with a more attractive gross margin profile and that they seek to improve its gross margin profile further in the back half of 2023.

In fact, Stem declares that it will be EBITDA positive in H2 2023 and that the growth of its services operations will be the main driver behind the improvement in profitability.

All that being said, when asked on the earnings call whether Stem’s larger Front-of-the-Meter (”FTM”) projects would carry lower margins, the answer was moderately evasive but could lead one to imply that since bigger contracts are typically done with companies that have their own procurement engines already, these projects could ultimately see further downward pressure on Stems gross profits margins.

The Bottom Line

This is my critical argument: investor enthusiasm for Stem has now washed out. The company’s backlog is rapidly growing. And Stem is striving to be EBITDA profitable in H2 2023. Hence, the company is staging a comeback.

But at the same time, Stem shorts remain stubbornly shortsighted. It’s not that I believe that shorts are whole inaccurate on their assessment, but rather that the risk-reward of staying short at this valuation doesn’t make too much sense.

The Stem, Inc. business is already at 1x sales. Meaning that investors are already pricing in a lot of negativity.

Read the full article here