When I think of growth, my mind focuses on capital appreciation rather than dividend growth, and I would assume this is similar for many investors. Growth companies are typically associated with names such as Tesla (TSLA), NVIDIA (NVDA), and Amazon (AMZN). There are also dividend growth companies, as there are many companies that have continuously increased their dividend or distribution on an annual basis. Enterprise Products Partners (NYSE:EPD) is often regarded as the gold standard in the master limited partnership (MLP) space and for good reason. EPD has provided investors with 24 consecutive years of distribution increases, and no matter what has occurred, investors have been able to rely on quarterly distributions.

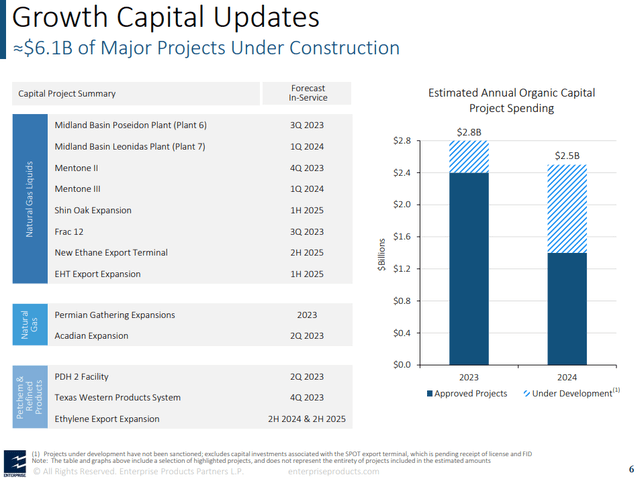

Why can’t a boring energy infrastructure company be a growth company outside of the distribution increases? I think it can, as EPD has $6.1 billion of major projects under construction, and the oil and gas sector is growing, regardless of political views. For a party that has hardliners against oil and gas, things took another turn in May as the Biden Administration grated the Mountain Valley Pipeline Permit in May, and the recent debt ceiling bill includes approvals for the remaining permits to complete the stalled project. For years I have said to look at the oil and gas industry through a lens of necessity, not based on political biases. The reality is that all sources of energy are needed to meet the growing demand for energy, and traditional energy companies will continue to play a critical role on the global stage for decades. After reading through EPD’s Q1 report and looking at the EIA projections, I am more bullish than ever on EPD. In my opinion, the opposition to oil and gas seems to be dissipating in the media. If it has a resurgence during the campaign trail is another story, but I think the narrative may be turning. EPD offers one of the highest quality large dividends and has a tremendous growth pipeline to capitalize on the industry’s future.

Seeking Alpha

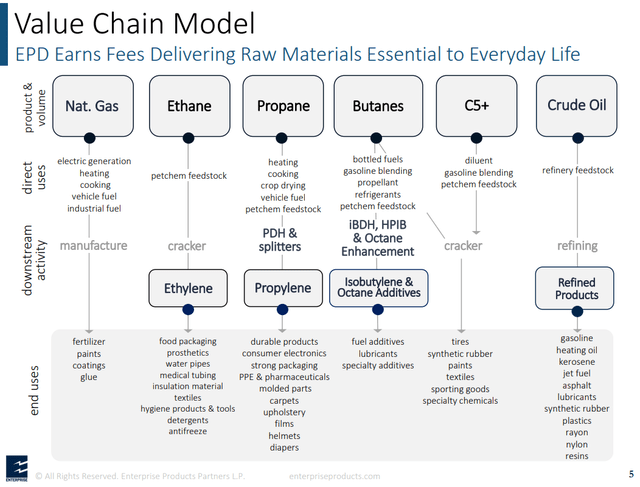

EPD’s first growth story is income and its impressive

Everywhere I look, I see opportunities to generate income. Walking down the street in NYC, every bank has signs advertising their CD rates. Thanks to the Fed, we no longer live in a yield-starved environment. Buying equities yielding 3% for income isn’t that exciting in 2023. On a 1 year CD, I see rates as high as 5.22%, with several financial institutions paying over 5% APY. If you’re strictly looking for income, why would you take on equity risk for a yield that is under what you can get from a no-risk CD? You can even lock in 4.3% APY and higher on a 5-year CD. Some people invest for income, and in this type of market, it’s hard to make a case for dividend stocks paying 2-3% when C.D.s are in the 4-5% range.

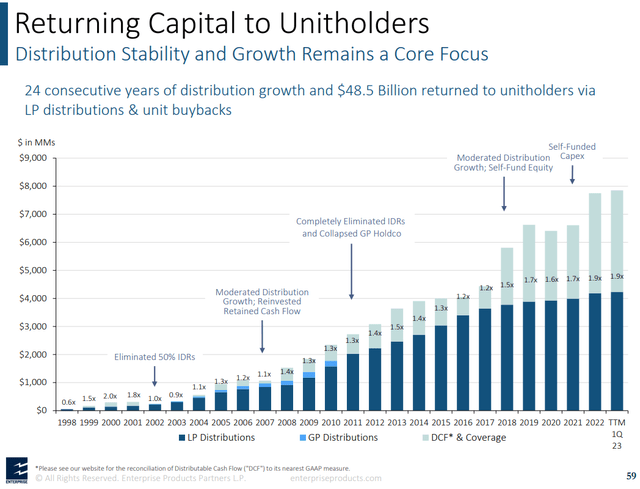

Since going public, EPD has returned $48.5 billion of capital to unitholders through distributions and buybacks. This has occurred while maintaining a large distributable cash flow (DCF) coverage ratio, which currently sits at 1.9x. EPD started paying a quarterly distribution of $0.08 in the fall of 1998. Since then, the quarterly distribution has increased 5.13% to $0.49. EPD pays an annual distribution of $1.96, which is a 7.64% yield. If EPD maintains the current 5-year distribution growth rate of 2.63%, its distribution would increase to $2.02 in 2024 and grow to $2.23 in 2028.

From an income perspective, EPD is attractive by all accounts. The additional yield compared to a CD or T-bill makes the equity risk palatable because you’re generating more than an additional 2%. Unlike T-bills or C.D.s, the distribution from EPD isn’t fixed. While there is a chance the distribution could be reduced, EPD has a track record of increasing the distribution through every economic event, including housing, banking, oil, and pandemic. The long track record is a testament to EPD’s cash flow generation, management, and stability of its business model. I am expecting EPD to continue growing its distribution annually, and I feel there is a possibility that the growth rate can increase when its backlog of projects comes online.

Enterprise Products Partners

EPD’s 2nd growth story is operational, and could lead to future appreciation

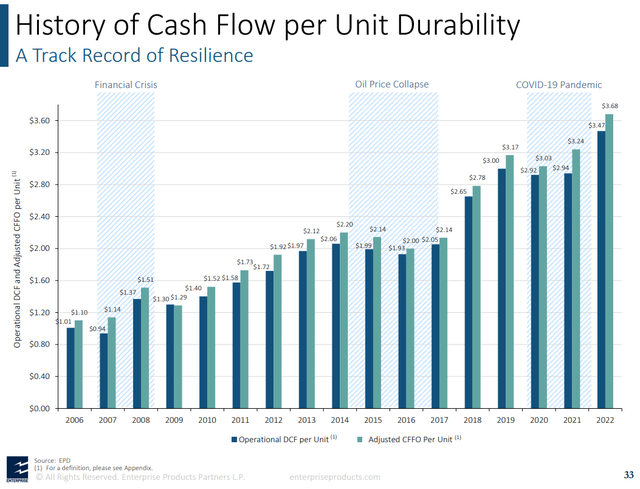

Since the oil crash of 2015, EPD has increased its revenue by 150.29% ($34.6 billion) to $57.62 billion in the TTM compared to its 2016 fiscal year. EPDs annualized EBITDA has increased by $4 billion (82.98%) over this period from $4.82 billion to $8.83 billion. Two of EPD’s most important metrics are their cash flow per unit and return on invested capital (ROIC). Since the dip in 2016, EPD has increased the amount of operational DCF each unit produces by 79.79% ($1.54). In 2016 each unit generated $1.93 of DCF, and in 2022, each unit generated $3.47 of DCF. This is a metric that I don’t see many people discussing. Since 2005, EPD has had an average historical ROIC of 11.94%. When I see the longevity of EPD’s ROIC, it indicates that management allocates capital efficiently and the business is able to grow and generate additional cash from its operations.

Enterprise Products Partners

In Q1 of 2023, EPD recognized record pipeline transportation, fee-based natural gas processing volumes, and near-record marine terminal volumes. EPD is currently on pace to place $3.8 billion of assets in service throughout 2023. In Q2, the PDH 2 facility and expansion of the Acadian Gas Pipeline system are scheduled to be completed and begin commissioning activities. In the 2nd half of 2023, EPD is on pace to complete its 12th NGL fractionator in Chambers County, two natural gas processing plants in the Permian Basin, and the 1st phase of the Texas Western products pipeline.

Enterprise Products Partners

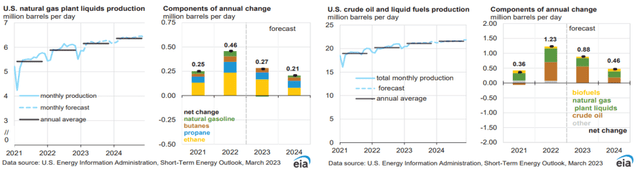

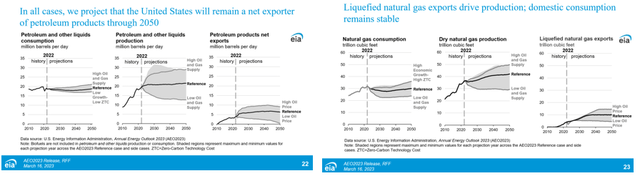

There are two critical reports that the EIA publishes, which include the International Energy Outlook (published every two years) and the Annual Energy Outlook. The Short-Term Energy Outlook from the EIA is clearly indicating that U.S. crude oil and liquid fuel production, in addition to natural gas production, will increase over the next two years. The reference case in the Annual Energy Outlook from the EIA projects that petroleum and other liquid production will slightly increase from now through 2050, and dry natural gas production will increase by roughly 20% through 2050. The EIA is also projecting that the United States will remain a net exporter of petroleum products and liquified natural gas (LNG) through 2050. The equation is simple, the more fossil fuels are produced, the need for transportation, storage, and refining will increase, and midstream operators will continue to see elevated needs for their services.

EIA EIA

Despite the track record over the last 5-years, I feel that EPD can be a future growth story for capital appreciation. The setup on the global energy stage favors EPD. Renewables will increase their position on the global stage regarding energy consumption over the next several decades, but the reality is that oil and gas will remain viable components of the global energy mix. Looking at the short-term picture, oil and gas production is expected to increase domestically over the next several years. EPD is placing new assets online to support production growth. One of the best aspects of this business model is the competition is already established, and there is enough room for everybody to benefit. New companies are not popping up in the midstream space due to regulations, land requirements, environmental studies, etc. EPD’s historical ROIC averages indicate that the new assets will help drive future operational DCF per unit, and the decades-long upward trend will continue.

EPD generates billions in cash annually and rewards unitholders by allocating billions towards buybacks and distributions. Management is aligned with shareholder interests, as 32% of the common units are owned by management. I think oil and gas stocks are still out of favor, and over the next several years, the narrative will continue to change as oil and gas remain the dominant sources of energy. Based on the historical numbers, EPD should continue to grow its top and bottom line, and eventually, the market should notice how much cash per unit is being generated and distributed and positively impact the unit price.

Enterprise Products Partners

Conclusion

EPD units have slowly recovered to the low point of their pre-pandemic levels. Oil and gas don’t grab headlines the way tech companies do and will never be the latest craze, such as A.I., but oil and gas are essential for the current and future standard of living. EPD can be both an income growth story as well as a capital appreciation growth story. EPD continues to deploy capital to grow while allocating billions annually to its capital allocation program. I believe that units of EPD will exceed $30 in 2024 while maintaining its distribution growth. When you can get 5% on a CD, it’s hard to take equity risk to generate income, but EPD generates a larger yield than non-risk assets and prospects for capital appreciation. EPD has a historical ROIC of 11.94%, which makes me believe the assets that are coming into service in 2023 will push its DCF higher and help make a case for a larger valuation in the future.

Read the full article here