Written by Sam Kovacs.

Introduction

2023 has been a year in which investors have had a tough time getting a read on the markets.

While the Fed has been busy increasing rates, inflation has somewhat stabilized, the economy has remained hot, with plenty of jobs going around, which has left the permabears wondering what is going on.

I’ve been a bull throughout, and now expect that we will have some choppiness throughout the year as:

- Investors shift their favored sectors.

- lagging effects of the rate hike campaign tamper the economy.

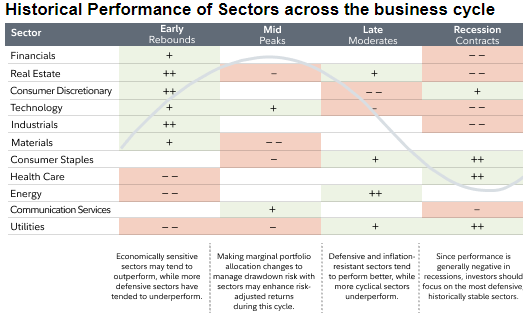

The market goes through a typical archetype of sector performance throughout the business cycle.

Fidelity has a nice table, which I’ve referred to multiple times throughout the years.

Fidelity

The problem is that this is an archetype, and in real life you don’t always get a perfect read of the situation as not all sectors will bottom out and move into the next phase at the same time.

In October 22, the market bottomed at 3,583.

Using Seeking Alpha’s sector performance tab, we can see a couple of clear trends.

Looking at the year-to-date rankings below, we can clearly see the leading performance of technology (communication services is now also biased towards tech), consumer discretionary and industrials.

We also see utilities, healthcare, and energy stocks underperforming.

SeekingAlpha

Real estate and financials are still in the bottom half of the sector rankings.

What does this look like?

To me, it looks like we’re witnessing a near typical archetype of the business cycle.

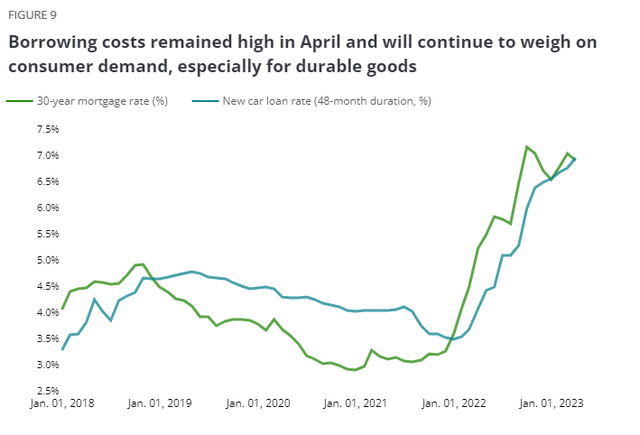

As the Fed will most likely skip its June rate hike to observe the lagging impacts of its policy, we are witnessing a near top of the rate hike cycle.

WSJ

As rates will remain high for a few more months, maybe until the end of the year until we witness more tampering of inflation, we will observe strain on consumers.

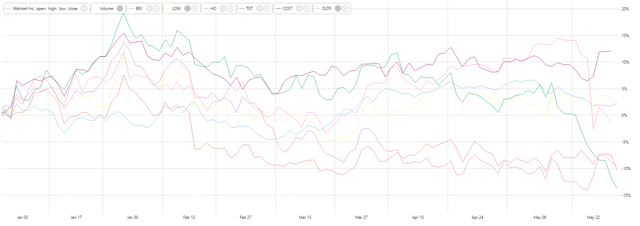

A number of retailers including Lowe’s Companies, Inc. (LOW), Best Buy Co., Inc. (BBY), Target Corporation (TGT) The Home Depot, Inc. (HD), Walmart Inc. (WMT), Dollar Tree, Inc. (DLTR) and Costco Wholesale Corporation (COST) have reported earnings.

The clear trend is that consumers have shifted their purchase preferences, are becoming more selective, and moving purchases from what they want to what they need.

However, these consumers are still healthy, despite a change in consumption habits towards value. Account balances and savings are still above pre-pandemic levels. Pain can be dealt with, without a major recession, or maybe without a recession at all.

Retailer Performance YTD (Dividend Freedom Tribe)

The price action of these different stocks shows that the retailers that the market views as the most discretionary have suffered, and those the market views as most staple-oriented have continued to thrive.

This is reversing, with DLTR falling through the roof on market worries about margins.

The market is clearly pricing a soft landing at this point.

Remember that the stock market is a leading indicator. So it bottomed in October last year, and we’re only starting to see the worst of the Fed’s interest rate hikes in Q3 and Q4 of 2023.

We are now seeing the first moves of a rebound, before the economy goes through the worst of it. This signals an expectation of mild negative impacts on the economy.

Once it is clear to the market that rates will stop going out, the bottom should definitely be in for financials and real estate, which should bounce back as we move fully into the rebound phase of the market.

This thesis is the basis for today’s investment suggestions.

There is still a considerable number of consumer staples stocks which are still at elevated prices, benefitting from the market favoring them through the recessionary part of the cycle. Remember these will not necessarily do well as the economy worsens, as market participants look out to what’s next.

In the same way, many real estate stocks and financials have felt the full wrath of the market this year.

An inversion in the performance of these 3 sectors is likely to happen in between Q3 2023 and Q2 2024. When exactly is up for grabs, but astute dividend investors would be well served by selling expensive consumer staples and buying cheap real estate and financial stocks.

Sell Walmart

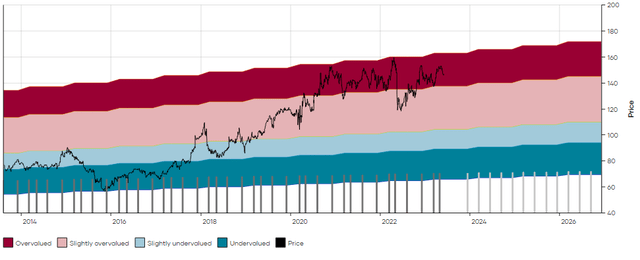

Walmart Inc. currently trades at $146 and yields 1.55%.

A look at the DFT Chart below gives a good explanation of why WMT stock has failed to make much progress since the pandemic: it is historically overvalued.

WMT DFT Chart (Dividend Freedom Tribe)

It is crazy to me to think that dividend investors are clinging on to a stock which has been growing the dividend at 2% per year (and I’m being generous rounding up here…) and which yields less than 2%.

I understand that a lot feel they are safe, as since 2016 the stock has been a steady gainer.

But if we have learned anything from markets, it is that nothing lasts forever, and there is no real reason for WMT to trade at such a premium, other than as a reaction to a fear factor.

The company only pays out 52% of its earnings yet refuses to increase its dividend by a healthy amount. Why? The retailer is so huge that it will be hard for it to grow significantly, and because of its “recession proof” history, it gets a pass from the investing community.

But for investors who are seeking to maximize dividend income to live off income in retirement, WMT has no place in their portfolios.

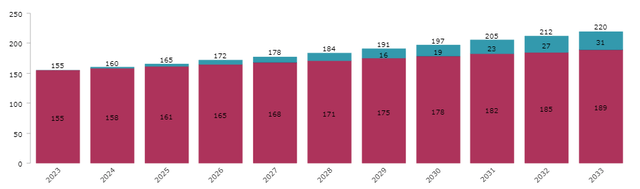

If you invest $10K in WMT today, and reinvest the dividends at the current yield, while the dividend continues to grow at 2%, then in 10 years you can expect WMT to provide you with $220 in annual income.

WMT Income Projection (Dividend Freedom Tribe)

This is 2.2% of your original investment, and an insignificant amount.

WMT is not a dividend stock. It is a defensive consumer staples company, and the exact sort of stock which will only provide respite for a quarter or two at the most before it has nowhere to go but down.

I recommend all dividend investors sell WMT stock based on valuation.

Sell Coca-Cola

2020 showed investors what can happen when a stock reaches an overextend valuation and a shift happens. The Coca-Cola Company (KO) stock went from $60 to $37.

And of course many stocks declined severely before staging a recovery, but the point remains that buying or holding stocks when they are historically overvalued, especially when sector shifts could hinder them in the near term, is a very dangerous play.

KO currently trades at $60, down somewhat from its 2022 highs of $65.

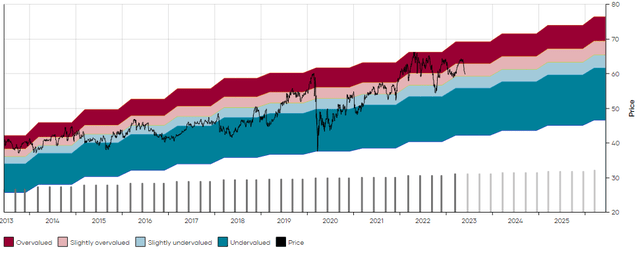

KO DFT Chart (Dividend Freedom Tribe)

I believe the stock could further decline to $50 to $55. These would not be massive declines, but because of the dividend profile of KO, selling and reinvesting in stocks with better income profiles makes sense.

As a reminder, the dividend profile is determined by analyzing in conjunction dividend yield and dividend growth potential. We focus on high quality stocks which have safe dividends, but of course dividend safety is also a major priority of ours.

In KOs case, it is clear the dividend isn’t going away, but does it provide enough of a kick to get us excited?

The answer is no. KO has historically achieved a 5% dividend growth rate, and while there is a case for payout ratios further improving in upcoming years as the company continues to find new avenues of growth and cost optimization, nothing is done yet.

In April, when I suggested members of the Dividend Freedom Tribe sell KO at $63, I said:

KO continues to deliver as a company, finding new avenues of growth, offsetting volume declines with pricing, and doing all the right things.

I cannot complain about the company’s operations or its results.

It’s price is chronically high.

I know that won’t last.

If KO can improve its cash flow payout ratios even more in the next few years, and show increased dividend growth, then I might be interested in KO, but for now, it is a clear sell for me.

Nothing has changed. We provide guidance to buy KO below $46 and sell above $60. KO is at the inflection point now between our Sell List and our Watch List.

If you invest $10K in KO today, and the dividend grows at 5% per annum, while you reinvest dividends at a constant yield, then 10 years from now, you’d expect $685 in dividend income, or 6.85% of your original investment.

KO Income SImulation (Dividend Freedom Tribe)

This is 3x more than from a Walmart investment, but still well below our threshold of 8% for a good income opportunity and 10% for a great income opportunity.

Now is maybe the last good time to realize capital gains and redeploy cash.

Buy VICI properties

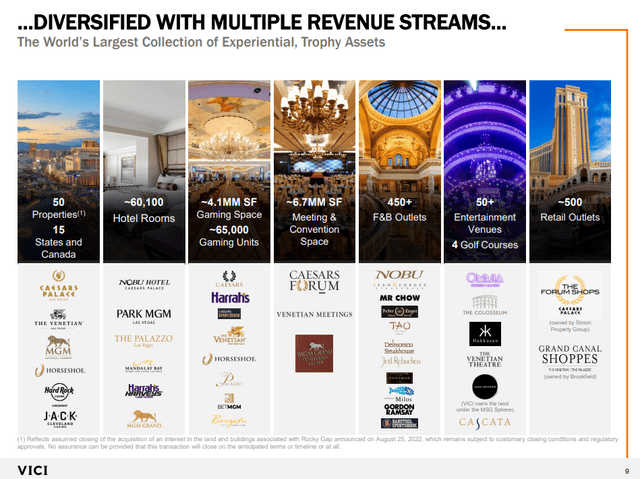

Vici Properties Inc. (VICI) is a relatively new real estate investment trust, or REIT, which has been in acquisition mode since its formation to deviate from its overexposure to Caesar’s Palace when the stock was initially launched in 2018.

Since then, the triple net lease REIT has expanded its presence to 50 properties spread in 15 states as well as in Alberta, Canada.

May Investor Presentation (VICI)

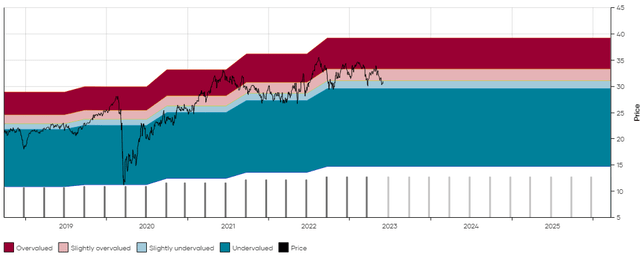

VICI stock currently trades at $31 and yields 5%, its median yield over its 4 years of existence.

VICI DFT Chart (Dividend Freedom Tribe)

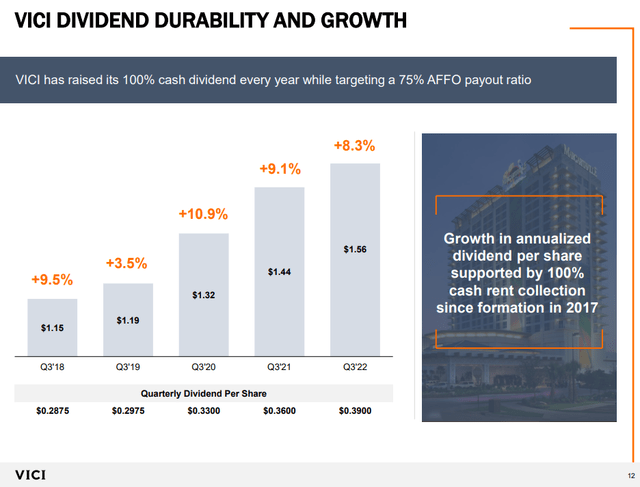

During this time, VICI has continued to increase its dividend aggressively as it has acquired more properties.

Dividend Growth (VICI)

The 8-10% dividend growth rates are not typical of a stock which yields 5%, providing phenomenal income potential for dividend investors.

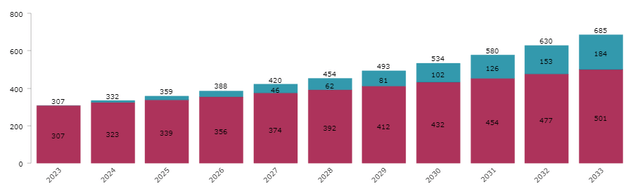

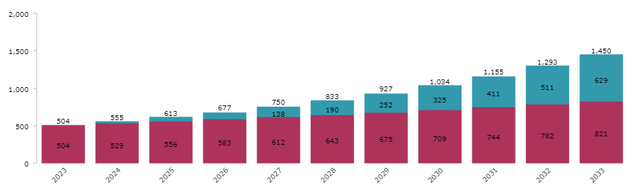

If you were to invest 10K today at the current price, and reinvest dividends at the same yield, while the dividend grows at 5% (a conservative more realistic outlook for future dividend growth), then in 10 years, you’d expect $1,450 in annual income.

VICI Income Projection (Dividend Freedom Tribe)

This is 14.5% of your original investment and a phenomenal income opportunity.

What is likely, though, is that when Real Estate stock prices pick up again, likely as rates top out, we’ll see VICI get rerated at a higher valuation.

Even a rerating to a 4% yield would suggest 25% upside in the price.

The income potential and stock price potential of VICI is much better than you could expect from a stock like Coca Cola, making it a great replacement to increase your income and expose yourself to upside over the next 12-18 months.

Buy Charles Schwab

The Charles Schwab Corporation (SCHW) was a victim of the banking fallout following the failure of Silicon Valley Bank and Signature Bank earlier this year.

In the initial aftermath of the SVB Financial Group (OTCPK:SIVBQ) failure, we initiated coverage of Charles Schwab for members of the Dividend Freedom Tribe, where we said:

It is a mistake to assume SCHW is a bank. It’s primarily a broker, that happens to own a bank, which is just a few percentage points of its assets.

Investors don’t treat brokerage cash as they do checking account cash, as it serves a different purpose. Schwab has plenty of available borrowing capacity.

The risk of a failure seems overblown on all accounts,

A straight line has been drawn from SIVB to SCHW and this just doesn’t seem to make sense

A month later, we provided an update when the company reported earnings.

Ever since July last year, deposits at the banks have been declining month over month as clients have been “cash sorting”, i.e.: moving their cash to better paying money market funds.

The increase in deposits in money market funds clearly outpaces the decline in bank balances as the firm opened over 1 million brokerage accounts in Q1 and received over $132bn in assets (not only money markets).

This, however does come at a cost to Schwab, which now has funds which it must pay more for. This pressures the company’s net interest margin.

This will only really start to show in the numbers in Q2, when Schwab’s Q2 revenue is likely to decline by mid-to-high single digit percentage points.

These higher cost liabilities have a weighted duration of less than 9 months, meaning that this spike in funding costs is expected to subside by the end of 2024, as the rate of cash sorting has been slowing down every month this year.

As SCHW still pays just 27% of its earnings, this should NOT impact the stock’s dividend policy or its rate of growth, as management still plans on reaching its objective of 3% net interest margins by 2025, despite the shorter term headwinds.

While the fears of the stock following in SIVB and Signature Bank’s (OTCPK:SBNY) footsteps have disappeared as most investors have come to accept that it was not happening, the price has yet to recover, as there have been very few inflows into financial stocks over the past quarter.

This results in Charles Schwab, which still yields 1.9%, above its 10-year median yield of 0.97%, and makes it a top replacement for a Walmart position.

SCHW DFT Chart (Dividend Freedom Tribe)

SCHW has a very low payout ratio, a great business, and a high growth dividend policy.

This year, the firm increased the dividend by 25%. This was likely the last of the very aggressive dividend hikes to catch up from the two years of flat dividends throughout 2020 and 2021.

Looking forward, though, SCHW can still likely increase its dividend at a 12-15% CAGR, fueled by growth coming from doubling down on servicing RIAs and self-directed investors by developing ever better digital experiences.

Within a year or two, SCHW is likely to resume its aggressive share buyback program as well, which should ease it.

Many analysts are viewing the cash sorting challenges the firm faced as coming to an end in the next few months.

The bottom could be in for SCHW stock, and it could be a double in the next two years.

Conclusion

Being exposed to the right sectors is extremely important. There is often some lag in portfolio managers (us included) in moving between sectors, which can cause some temporary underperformance relative to markets. After having the right sector mix to beat the S&P 500 Index (SP500) in 2022, we have underperformed the S&P 500 this year, giving back some of our outperformance, but in the process have geared ourselves towards the moves that we expect to happen in the later part of the year and next year.

Astute dividend investors make these “buy low sell high” transactions and get paid to wait.

Read the full article here