A Quick Take On Agora

Agora, Inc. (NASDAQ:API) recently reported its Q1 2023 financial results on May 30, 2022, beating revenue estimates and missing expected earnings results.

The company provides embedded video and related software capabilities to businesses worldwide.

Given Agora, Inc. management’s lowered revenue expectations, continued high operating losses, and ongoing drag from its Chinese Shengwang unit, my outlook for the near term is negative.

Agora Overview

Shanghai, China-based Agora was founded in 2013 to offer software developers with tools to embed video, voice, and messaging functionalities into Internet applications.

The company also has a Shengwang unit that focuses on the Chinese market.

The firm is headed by founder, Chairman and CEO, Bin (Tony) Zhao, who was previously director and Chief Technology Officer of YY, a video social network and was a senior engineer at WebEx Communications.

The company’s primary offerings include embedded software for these functionalities:

-

Video

-

Live Streaming

-

Voice

-

Chat

-

Signaling

-

IoT

-

AR/VR.

The firm acquires customers through direct sales and marketing efforts as well as through advertising and marketing events.

Agora has offices in Shanghai and Santa Clara.

Agora’s Market & Competition

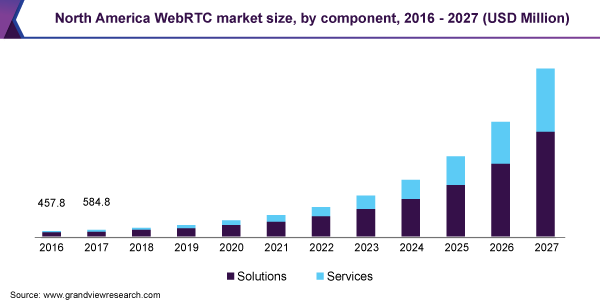

According to a 2020 market research report by Grand View Research, the market for Web real-time communications (RTC) products was an estimated $2.3 billion in 2019 and is expected to reach $41 billion by 2027.

This represents a forecasted extremely high CAGR of 43.4% from 2020 to 2027.

The main drivers for this expected growth are the need for a better user experience, reduced costs, and an increase in work-from-home employee work environments.

Also, the chart below shows the historical and projected future growth trajectory of the N. America WebRTC market through 2027:

N. American Web RTC Market (Grand View Research)

Major competitive or other industry participants include:

-

Amazon

-

Google

-

Facebook

-

Cisco

-

Oracle

-

Ribbon

-

Avaya

-

Apidaze

-

Dialogic

-

Plivo

-

Quobois

Agora’s Recent Financial Trends

-

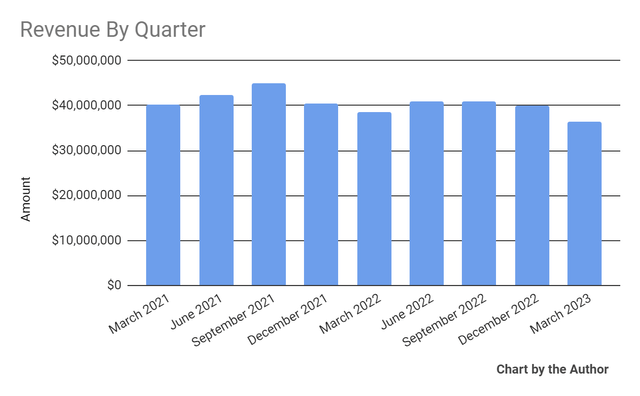

Total revenue by quarter has trended lower in recent quarters:

Total Revenue (Seeking Alpha)

-

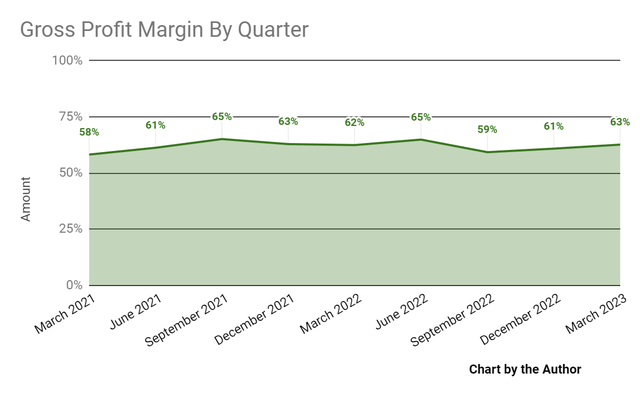

Gross profit margin by quarter moved slightly higher YoY in Q1 2023:

Gross Profit Margin (Seeking Alpha)

-

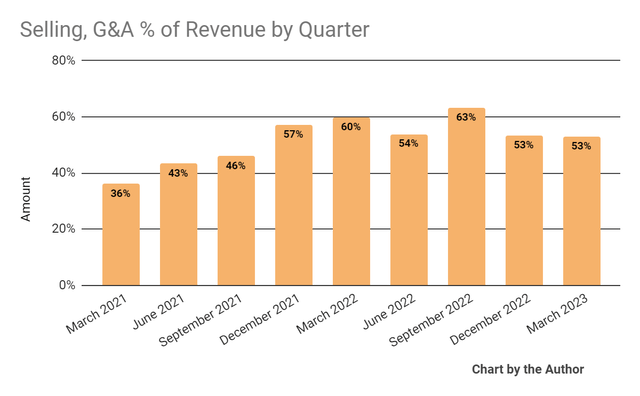

Selling, G&A expenses as a percentage of total revenue by quarter have fallen sequentially in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

-

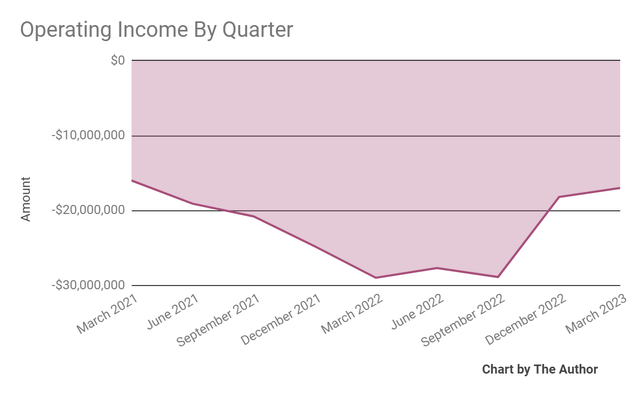

Operating income by quarter has remained heavily negative:

Operating Income (Seeking Alpha)

-

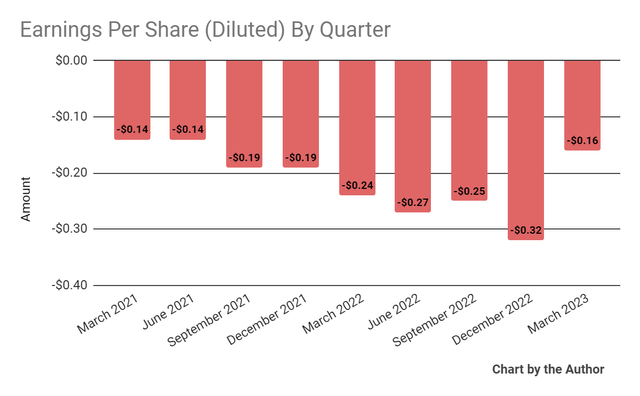

Earnings per share (Diluted) have also remained negative:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

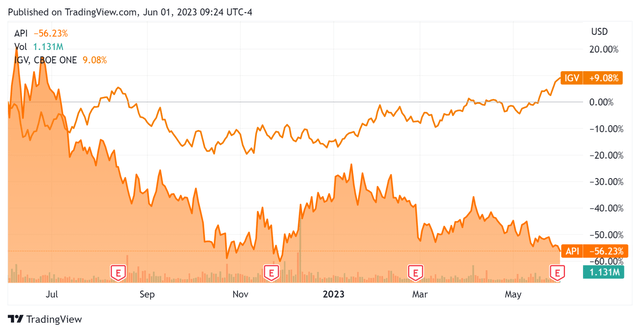

In the past 12 months, API’s stock price has fallen 56.23% vs. that of the iShares Expanded Technology-Software Sector ETF’s (IGV) rise of 9.08%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $225.6 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash used was a hefty $50.6 million, of which capital expenditures accounted for only $5.2 million. The company paid $30.4 million in stock-based compensation (“SBC”) in the last four quarters.

Valuation And Other Metrics For Agora

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (TTM) |

Amount |

|

Enterprise Value/Sales |

0.5 |

|

Enterprise Value/EBITDA |

NM |

|

Price/Sales |

2.0 |

|

Revenue Growth Rate |

-4.4% |

|

Net Income Margin |

-74.9% |

|

EBITDA % |

-57.3% |

|

Net Debt To Annual EBITDA |

4.6 |

|

Market Capitalization |

$291,960,000 |

|

Enterprise Value |

$71,520,000 |

|

Operating Cash Flow |

-$52,380,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.00 |

(Source – Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

Agora’s most recent Rule of 40 calculation was negative (61.6%) as of the Q1 2023 results, so the firm has performed poorly in this regard, per the table below:

|

Rule of 40 Performance |

Calculation |

|

Recent Rev. Growth % |

-4.4% |

|

EBITDA % |

-57.3% |

|

Total |

-61.6% |

(Source – Seeking Alpha)

Commentary On Agora

In its last earnings call (Source – Seeking Alpha), covering Q1 2023’s results, management highlighted the reorganization of the company into two business units, Shengwang for the Chinese market and Agora for the global market ex-China.

Since there will be different legal entities and different tax jurisdictions, this presents potential regulatory, operational, foreign exchange, and financial risks to investors to the extent of the firm’s Chinese operations.

Regarding generative AI technologies, management believes they can serve to “significantly expand the scope and opportunity of real-time engagement.”

The firm has begun working with certain customers to “create pilot applications in certain verticals.”

The company’s Agora unit retention rate was 130% and its Shengwang unit retention rate was 92%, indicating very different product/market fit and sales & marketing efficiency rates.

Total revenue for Q1 2023 fell 5.7% YoY and gross profit margin rose 0.2 percentage points.

The revenue drop was largely attributed to the Shengwang unit, its disposal of the Easemob customer engagement cloud business, a drop in usage from the K-12 education sector, and the depreciation of the RMB against the US dollar.

Selling, G&A expenses as a percentage of revenue dropped 6.8 percentage points YoY while operating losses were reduced by 41.4% YoY.

As of the end of the quarter, the company had repurchased 31% of its $200 million repurchase authorization program, so it still had $138.7 million remaining.

Looking ahead, management has stopped providing annual guidance and will instead focus on quarterly guidance.

For Q2 2023, management has forecast total revenue of $35.5 million at the midpoint of the range, or a 13.4% drop YoY.

Leadership did not provide guidance on its expected EBITDA results.

The company’s financial position is moderate, with ample liquidity, no debt but substantial free cash burn.

Agora’s Rule of 40 performance has been quite poor due to highly negative operating results, dragged down by its Chinese operations.

Regarding valuation, the market is valuing API at an EV/Sales multiple of around 0.5x.

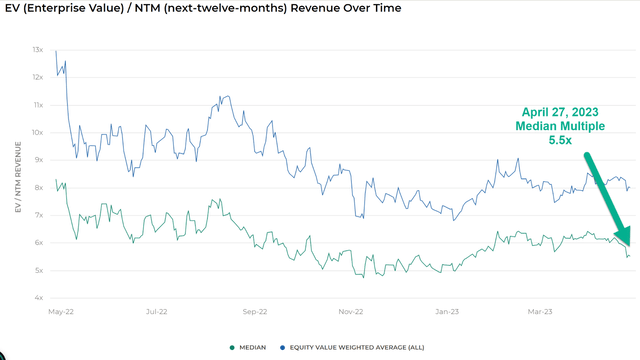

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

EV/Next 12 Months Revenue Multiple Index (Meritech Capital)

So, by comparison, API is currently valued by the market at a substantial discount to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

Risks to the company’s outlook include an economic slowdown that may be underway, reduced credit availability which may affect customer/prospect spending plans and lengthening sales cycles which may reduce its revenue growth potential in the near term.

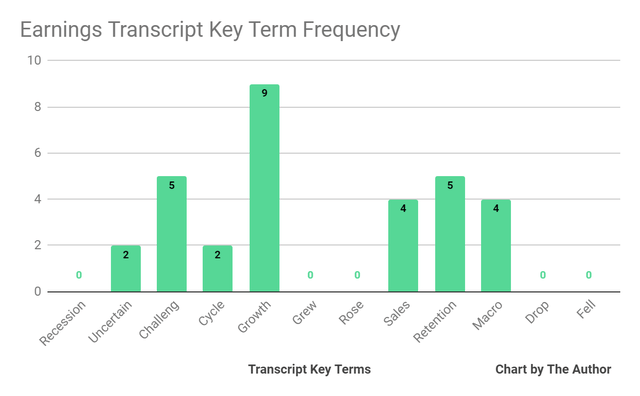

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited “Uncertain” two times, “Challeng(es)(ing)” five times, and “Macro” four times.

The negative terms refer to the challenging macroeconomic environment it faces and related business uncertainties.

Given Agora, Inc. management’s lowered revenue expectations, continued high operating losses, and ongoing drag from its Chinese Shengwang unit, my outlook for the near term is negative.

Read the full article here