Introduction and investment thesis

CrowdStrike (NASDAQ:CRWD) has been probably the most stable SaaS company from a fundamental point of view in the past few years characterized by stubbornly high revenue growth rates (despite its increasing scale) combined with best-in-class FCF margin of ~30%. In Q3 FY23 last year there was a small hiccup in fundamentals, where the company tempered near-term growth expectations leading to a correction in the share price. Q4 FY23 earnings showed that CrowdStrike managed to anchor investor expectations on a sufficiently conservative level and the streak of strong quarterly results could quickly reemerge. The positive trends in the preceding, Q4 FY23 earnings print have been the following:

- The company added a record number of new customers driven by its Falcon GO platform targeting the SMB segment

- Growth in net new ARR held up better than management forecasted reaching a new record and increasing slightly yoy

- The yoy growth in remaining performance obligations (RPO) accelerated signaling possible reacceleration of topline growth

In the following I will revisit these trends in the light of recently published Q1 FY24 earnings results. Before addressing these topics in more detail, I would like to start by saying that CrowdStrike is not completely out of the woods yet, i.e., short-term fundamental dynamics remain somewhat uncertain. However, management remained optimistic on the back half of the year that could provide important support for the share price. Thus, the post-earnings sell-off provides a good entry opportunity for investors to accumulate shares at lower prices, which I believe won’t last for long.

Rare dip in new ARR growth

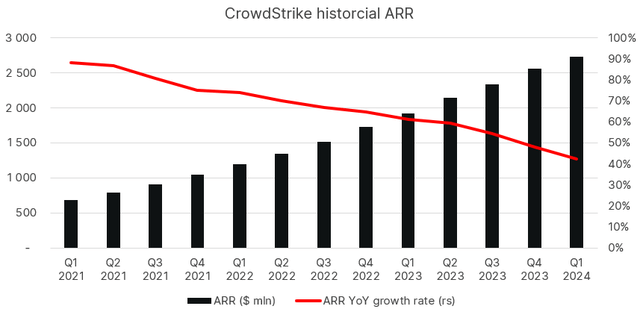

The most important metric for tracking topline growth at CrowdStrike is to look at exiting ARR at the end of the quarter as it provides the most current snapshot of recurring revenues. ARR reached ~$2.7 billion as of the end of Q1 FY24 growing 42% yoy. This proved to be a further gradual decline after 48% and 54% growth in Q3 FY23 and Q4 FY23, respectively:

Created by author based on company fundamentals

If we look at the slope of the line representing the yoy ARR growth rate, we can see that there was a break in the trend in the Q3 FY23 quarter. From this quarter on topline growth is decelerating at a faster pace than it did before. Q1 FY24 results didn’t indicate a change in this trend, so investors can still only guess about the magnitude and duration of the current growth slowdown. The main reasons behind this have been the extension of sales cycles at larger enterprise customers and softening expansion activity in the case of smaller companies amid an uncertain macroeconomic environment. It seems these trends continued into Q1 as well.

Management highlighted on the Q1 earnings call that larger consolidation deals have been pushed out even more during the quarter impacting topline growth to a somewhat larger extent. However, they remain confident that these deals will be closed soon leading to a stronger second half. On the top of that, they indicated that there haven’t been any changes in competitive dynamics lately, which could bode well for the remainder of the year as well.

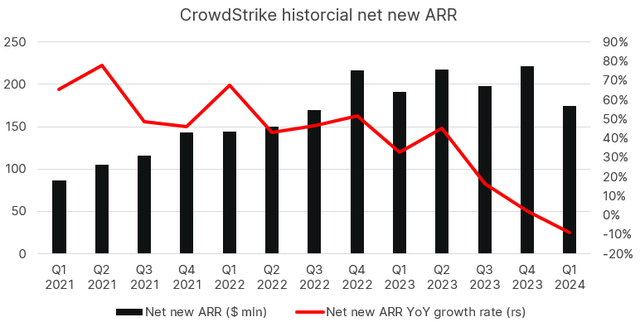

Jumping to net new ARR generated over the quarter, which is the best gauge according to management to track new business trends we can see a softening trend as well:

Created by author based on company fundamentals

In Q1 FY24 net new ARR came in at $174 million (as ARR grew from $2.560 billion to $2.734 billion), which has been a qoq decline of ~21%. As Q1 is seasonally the weakest quarter for net new ARR and a qoq decline from Q4 is typical this shouldn’t a reason for concern for the first sight. However, if we look at the yoy change we can see a ~9% decline, which is the first negative reading in the past several years. As management guided for flat to slightly up net new ARR for FY24 on the previous earnings call and confirmed this goal during the most recent one, this could set the bar higher for the upcoming quarters.

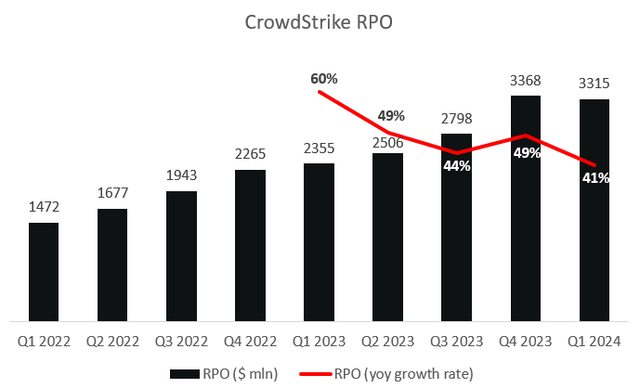

Finally, another sign that topline growth headwinds could prevail on the short run is that RPO grew “only” 41% yoy in the Q1 quarter postponing the idea of a possible turnaround that began to emerge in the preceding quarter:

Created by author based on company fundamentals

The slight decline after the seasonally strong Q4 quarter is not a problem in my opinion, but the significant decrease in the yoy growth rate signals that the bump in Q4 could have been rather a one-off and not a positive change in the trend. However, growth rates over 40% still indicate that ARR growth shouldn’t have much more room to decline further.

Based on the above it seems that short-term revenue dynamics remain somewhat uncertain at the company, but management prepares for a reacceleration in the second half. According to them, this should be aided by larger consolidation deals that are already in the pipeline, which seemed to gain traction in recent quarters with some acceleration since the middle of Q1. Good evidence for this is that in Q1 FY24 the company closed 50% more deals with 8+ modules compared to a year ago, which is expected to continue in the back half of the year. I believe this confirms that CrowdStrike is the leading player in the modern IT security space and has ample room to disrupt the space further in the upcoming years.

Finally, as a closing note for this section there have been some announcements in the Q1 release that could support revenue growth acceleration in the upcoming quarters/years:

- CrowdStrike entered into a strategic partnership with Pax8, a leading cloud marketplace for managed service providers. Based on the company’s website, Pax8 is an important partner of Microsoft (MSFT), so this deal could possibly further sharpen the direct competition between two largest players in the endpoint security market.

- CrowdStrike has been granted the Impact Level 5 Provisional Authorization from the United States Department of Defense, which is the highest level of authorization for the DoDs unclassified assets.

- CrowdStrike introduced Charlotte AI, an IT security analyst based on generative AI. Charlotte could increase the efficiency of security teams who use the Falcon platform by a significant margin.

- CrowdStrike joined efforts with AWS to help customers develop generative AI applications where it assures stringent security requirements with its Falcon platform.

Margin profile remains a bright spot

CrowdStrike has already one of the most enviable margin profiles in the SaaS space with continuously reaching FCF margins north of 30%. The company went in the Q1 quarter one step further and reached GAAP profitability for the first time in its history. Although this won’t possibly last in the upcoming quarters it’s a rare milestone for a company still growing 40%+ at the top.

The driver behind the further improving bottom line has been the continued improvement in the company’s gross margin profile due to investments into data centers and workload optimization. These drove subscription gross margin above 80% for the first time, which is expected to expand further over the upcoming years.

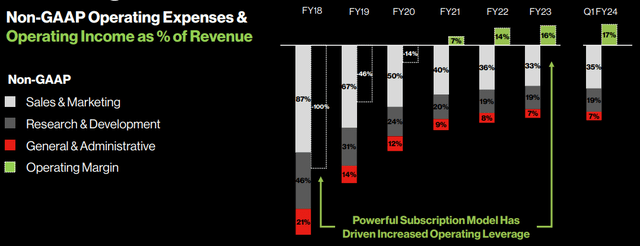

This has been the reason that despite seasonally increasing S&M expenses CrowdStrike managed to slightly increase its non-GAAP operating margin from FY23 levels, which trend could continue in the upcoming quarters:

CrowdStrike Q1 FY24 earnings presentation

We can see from the chart above that despite the fact that S&M expenses increased to 35% of revenues in Q1 FY24 compared to FY23, non-GAAP operating margin increased from 16% to 17%. I believe this is another good proof for the company’s unmatched operating model.

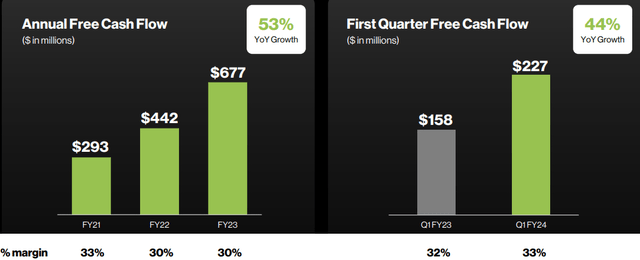

Based on this it’s no wonder that the company increased its cash pile to almost $3 billion during the Q1 quarter by adding another $227 million:

CrowdStrike Q1 FY24 earnings presentation

With this, FCF margin came in at 33%, slightly above the company’s recently refined 30-32%+ long-term target. Adding the 33% FCF margin and the 42% yoy growth in ARR gives us a Rule of 75 company demonstrating the efficiency of the company’s operating model.

Quick thoughts on valuation

CrowdStrike had a market cap of $38 billion before releasing Q1 results, which based on pre-market drop of 10% should be closer to $34 billion. For FY24 analysts are expecting revenues of $3 billion leading to a forward Price/Sales ratio of 11.3. For the first sight this could seem aggressive as many companies trade at a P/E ratio like this, and not at a P/S ratio.

However, if we consider that revenues could grow at a CAGR of ~30% over the upcoming 3 years (analyst consensus), the multiple would decrease to ~5.5 for the beginning of calendar year 2026 assuming 2% annual dilution from SBC. Applying a realistic 25% net margin to this it would result in a forward P/E of 22, only slightly higher than the S&P500’s current ratio of 18. This shows that only in a few years’ time CrowdStrike’s current valuation premium could diminish quickly if shares stay at current levels.

I believe this isn’t a realistic scenario as I couldn’t imagine at the beginning of 2026 that CRWD shares trade at a valuation close to the S&P500, rather still at a nice premium like today due to the company’s leading position in one of the most important spaces in IT. This gives me strong confidence that from a long-term perspective shares are valued too conservatively currently and should outperform the S&P500 by a wide margin in the upcoming years.

Conclusion

CrowdStrike Q1 earnings release disappointed those investors who priced the company for perfection leading to an initial negative market reaction. I believe this provides a limited opportunity for long-term investors to acquire shares at a somewhat lower price. Based on management comments on the Q1 earnings call the tide could turn quickly in the upcoming quarters leading to improving topline growth numbers beside already strong margins. I believe it’s better to buy these rumors now than wait until news come out.

Read the full article here