Thesis

Darling Ingredients (NYSE:DAR) has had a huge year, having acquired 4 separate businesses since the start of 2022. This has increased raw material processing volumes but has reduced margins while these are digested. Based on my analysis of the acquisitions and their expected contribution I believe it looks like management has given the absolute base case scenario guidance, providing opportunity for upgrades throughout the year as each acquisition contributes a full year. Diamond Green Diesel is also currently producing margins well above guidance, providing more potential upside. In this article, I will explain my analysis and provide a valuation range that demonstrates the above.

Company Profile

Darling Ingredients has a worldwide network of businesses that collect food waste and byproducts, which they convert and recycle into various other products across 3 core divisions: Feed Ingredients, Food Ingredients, and Fuel Ingredients. Food waste byproducts come from various sources such as bakeries, slaughterhouses, butchers, and grocery stores. This is broadly called “rendering”.

Products predominantly produced in the Food Ingredients segment include pet food, collagen, and gelatin. In the Feed segment DAR produces protein meal, non-food grade oils, hog and cattle hides, organic fertilisers, and various feedstock products that feed poultry and swine.

The Fuel segment takes various oils (primarily soybean oil, used cooking oil, animal fats, and corn oil) and turns this into biogas or low grade energy sources for industrial uses, and renewable diesel. The renewable diesel is the largest component of the Fuel segment and draws from Darling’s 50:50 joint venture, Diamond Green Diesel (DGD), with Valero Energy (VLO).

Darling’s recent acquisitions

In February 2022 Darling acquired Group Op de Beeck for ~$75m. Group Op de Beeck is a Belgian industrial byproduct and organic waste processing company that fits into Darling’s Fuel Ingredients segment. The company takes organic waste, places it into a “digester”, in which micro-organisms break down the matter to produce carbon dioxide, hydrogen, ammonia, and acids. These are eventually converted into biogas, which is used in fertilizer. This process also generates electricity, which is used in their facilities.

In May 2022, Darling announced the acquisition of Valley Proteins for ~$1.18 billion. Valley Proteins is a US-based rendering company with 18 plants across the country. Rendering is Darling’s core business so the rationale for this acquisition is to further increase the scale of the company with more plants, more trucks, and more collection capacity. On the 2Q22 conference call, CEO Randall Stuewe said he expected Valley to contribute $150m in EBITDA in the 2023 year. This suggests a 7.8x EBITDA acquisition multiple, which is about in line with their own multiple. This also implies, on a 7-month basis, that Valley would have contributed about $87.5 million, meaning that the acquisition will contribute an incremental $62.5m in 2023.

In August 2022, Darling finalized the acquisition of FASA Group for ~$563m. FASA is a Brazilian based rendering company with 14 plants, contributing 1.3 million metric tons of animal byproduct. FASA was acquired as Brazil is expected to experience good meat production growth, making it ideally placed to grow its rendering capacity, which can feed the growing demand for renewable diesel. It is understood that FASA will contribute around $100m in EBITDA annually (per the 3Q22 conference call). If we take the midpoint, this suggests, in the 5 months it was owned in 2022, it would have provided ~$42m, leaving $58m of incremental EBITDA to be contributed in 2023.

In April 2023, Darling announced the acquisition of Gelnex, for ~$1.2 billion, also based in Brazil. Gelnex is a producer of gelatin and collagen products with 45,000 tons of production capacity across 17 facilities around the world. It is expected to contribute $75m in EBITDA to the 2023 result (or approximately $100m at an annualised run rate). This suggests a 12x EBITDA acquisition multiple. The rationale behind the acquisition of Gelnex is to bolster their gelatin and collagen capacity, which is a growth industry, as it is increasingly appreciated for its health benefits for hair, skin, nails, joints, bones and muscles.

The company financed all these acquisitions – about $3.0 billion worth – with cash and debt, taking total borrowings from $1.46 billion in 4Q21 to $4.68 billion in 1Q23. This took the leverage ratio (as measured by the bank covenant) from 1.57x to 3.2x. It bears noting that the 3.2x includes the debt for Gelnex but none of the earnings as well as only part-year contributions from the others, so this will decline immediately.

2023 Guidance Looks Low

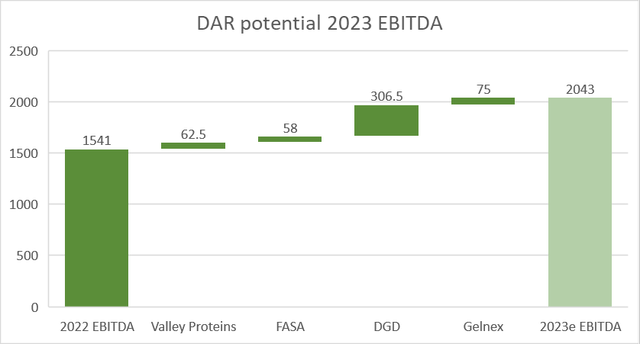

In 2022, Darling produced Combined Adjusted EBITDA of $1,541 million. This excludes $46m of acquisition and restructuring charges but for this analysis it actually makes it clearer to keep it excluded so I’ll just take their calculation for simplicity.

I mentioned above that Valley Proteins should contribute an incremental $62.5 million EBITDA for the year and FASA should contribute an additional $58 million if they both meet expectations. In addition, Gelnex is expected to contribute $75 million for the 9 months it will be a part of the Group.

Further, Diamond Green Diesel (DGD) has also recently completed an expansion to 1.2 billion gallons of renewable diesel capacity and Stuewe guided on the 4Q22 conference call that it is expected to produce this at a minimum EBITDA margin of $1.10 EBITDA per gallon, which has already been upgraded to $1.25. If this is achieved that would produce $1,500 million EBITDA, $750 million of which would be Darling’s share. As DGD contributed $443.5m EBITDA in 2022, this represents a $306.5m incremental EBITDA uplift.

If we add all these incremental EBITDA contributions to the 2022 EBITDA, we get an EBITDA estimate of $2,043m. I’ve shown this in the following waterfall chart:

DAR SEC filings and author’s analysis

Source: DAR SEC filings and author’s analysis

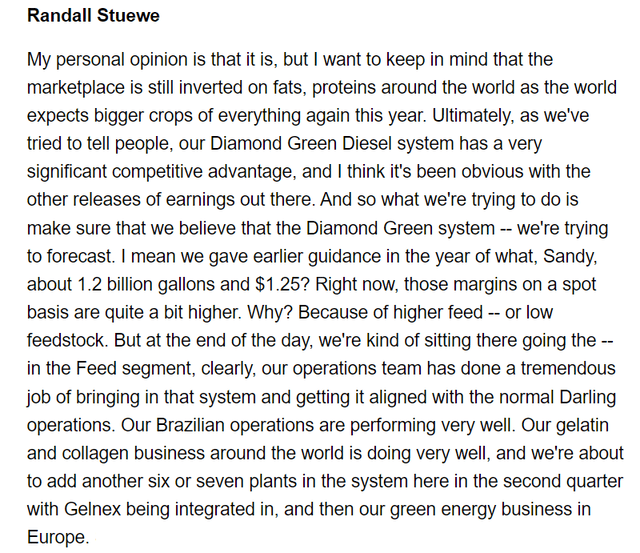

This suggests there is a fair bit of conservatism baked into the guidance. In fact, although they approached it differently, an analyst suggested on the call that guidance looked a bit conservative, and Stuewe agreed. His response is worth quoting in full:

1Q23 conference call

-

Randall Stuewe, DAR CEO, 1Q23 Conference call

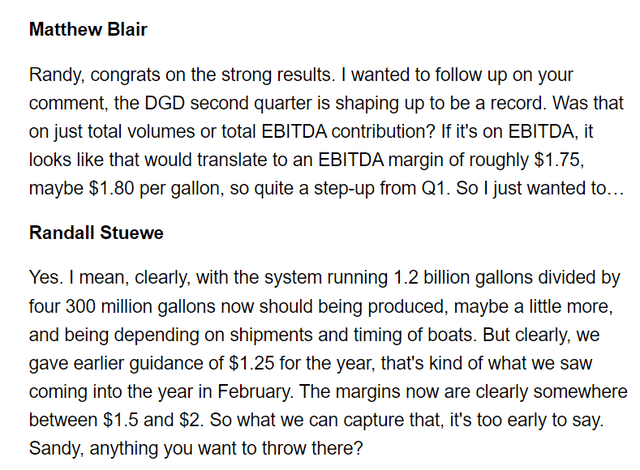

Further, in the same Q&A, another analyst asked about the strong 2Q23 that is expected for DGD. Lower fat prices, which is a raw material input cost for renewable diesel production, are leading to higher margins, which could be well north of $1.50 EBITDA per gallon. Again, the exchange is worth quoting in full:

DAR 1Q23 conference call

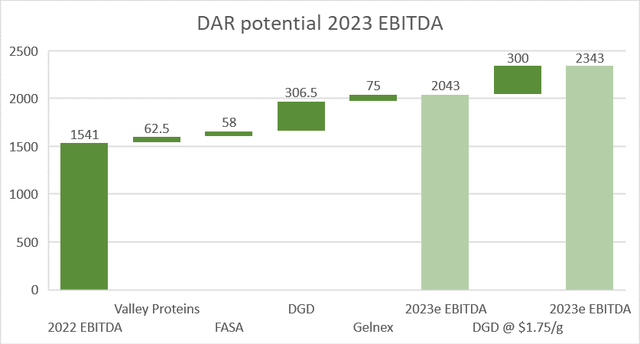

Hypothetically speaking, this could be another $300m EBITDA contribution to DAR, as shown on the following waterfall chart, an extension of the one above.

DAR SEC filings and author’s analysis

Considering how far above guidance this is, it feels quite aggressive, but we should also bear in mind that in 4Q22, DGD EBITDA margin was $1.40 per gallon, for the full year 2022 it was $1.18 per gallon, and for 1Q23 it was $1.01 per gallon. It moves around quite a bit but margins materially above the current guidance level have been achieved in the past so it is not outside the realm of possibility.

All that to say, this is not my base case, but is a demonstration of what is plausible.

Valuation

Using the above analysis, we can produce a range of valuation outcomes just by tweaking our EBITDA assumptions based on a range of outcomes.

My assumptions for the valuations are as follows:

-

Capex investment of 5.5%-6% of revenue;

-

Working capital investment of around 14% of incremental revenue;

-

An 8x EV/EBITDA multiple for the DGD equity accounted contribution to the valuation, which is in line with DAR’s current EV/EBITDA multiple;

-

WACC of 8% derived from 4% risk free rate, 5.3% equity risk premium, 1.2 beta, and 5.3% cost of debt based on most recent A-3 and A-4 notes issued to fund Gelnex;

-

Terminal growth rate of 2%.

My variable assumptions are shown in the following table:

|

Assumption |

Guidance case |

Base case |

Bull case |

|

2023 Adj EBITDA est |

$1,875m |

$2,002m |

$2,389m |

|

4 yr Revenue CAGR |

5.5% |

9.1% |

12.3% |

|

4 yr Adj EBITDA CAGR |

7.8% |

11.0% |

16.5% |

|

2023 DGD EBITDA |

$750m ($1.25/g) |

$750m ($1.25/g) |

$1,050m $1.75/g |

|

Valuation |

$66.94 |

$70.41 |

$95.59 |

Notes:

-

My base case forecasts Combined Adjusted EBITDA of $2,002m, which is ahead of guidance and consensus, but also doesn’t assume that all of the incremental EBITDA contributions come through in 2023, building in some contingency.

-

The EBITDA contribution from DGD in the bull case is assumed to be volatile and return to $1.50 and $1.25 margins in future years.

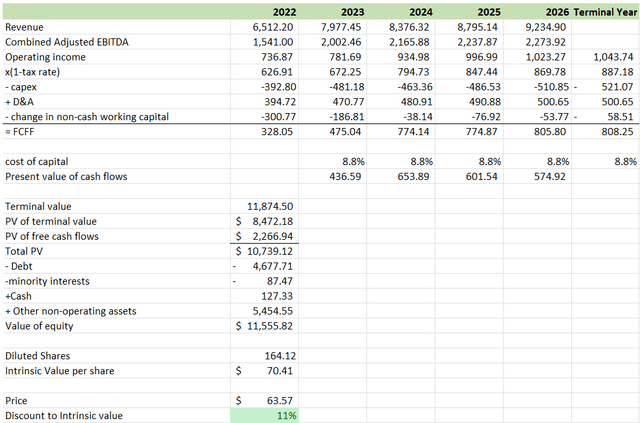

My base case FCFF model is below:

Author’s analysis based on FactSet data

Downside Risks

Whenever a stock seems mispriced I find it prudent to ask why? What might the market be seeing that I am not? In other words, what could go wrong? I’ll discuss a few things that could be on the market’s mind beyond merely focusing on the company’s guidance.

Commodity prices are an inherent risk in the Darling business model. The market prices for tallow, yellow grease, meat/bonemeal, soybean oil, corn oil, palm oil, soy meal, and renewable diesel all move in different directions and impact the margins Darling can earn. These are the commodities that Darling sells and they have little control over it. In the last few years these commodity prices have been quite strong and have been windfall for the company. A reversal in these prices could lead to EBITDA weakness and could be the source of conservativeness from management.

Any changes to the Low Carbon Fuel Standard (LCFS) could also have a negative impact on the earnings of DGD, which has been a beneficiary of the program. The LCFS is a credits system that has the effect of increasing demand for renewable diesel. The standard is in effect in California — which is a major market for renewable energy — while Washington, Oregon and British Columbia also have programs in place. While the risk of this program changing to the negative might be low, the fact remains that it artificially props up the renewable diesel price.

Similarly, DGD is the recipient of other blender tax credits, which is probably a more significant impact than the LCFS. These tax credits provide a tax credit of $1.00 per gallon of renewable diesel produced. The program has been extended out to 2027, so the risk is that it is not extended further beyond this date. Whilst I think it is likely that the government will continue incentivizing the use of greener fuels and energy sources to meet decarbonization targets, it remains unclear if this will continue to be the path chosen for renewable diesel.

Any negative changes in any of the above, what I consider to be the most pertinent risks for Darling’s business, will have a downward impact on the company’s earnings and its valuation.

Conclusion

Darling Ingredients is a company with a lot of moving parts and 4 major acquisitions in the last 12 months have made analysis of the company and its future prospects a little more difficult. Because of its exposure to commodities prices on both the sales and the costs lines, margins can move around, making Darling a prime candidate to be analysed with scenarios.

I have presented three, the purpose of which was not to provide a concrete valuation, but to provide a range out of potential outcomes. Starting with guidance and assuming modest growth thereafter, it would appear that the company is close to fairly valued. However, if, as discussed, this proves to be conservative, there is upside to be had with an aggressive bull case valuation of $95.59. The true valuation of the company will be somewhere in the middle, but with the current share price reflecting the bottom of the range, guidance upgrades are a real possibility, which makes Darling Ingredients a buy.

Read the full article here