Remarkable Turnaround

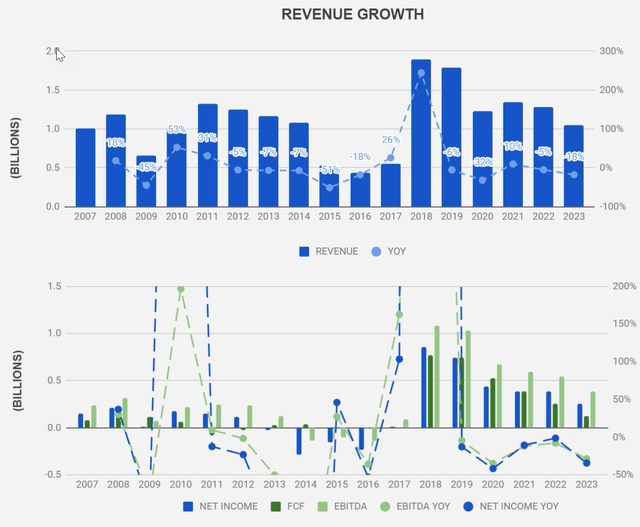

One image is worth a thousand words. It does not take an investing genius to look at Figure 1 and quickly realize something very significant happened to GrafTech International (NYSE:EAF) circa 2018. From inconsistently razor thin free cash flow and mostly negative earnings to a sudden 14.9% and 16.6% free cash flow and earnings yield respectively.

Figure 1: EAF Revenue, Earnings and Free Cash Flow Growth (Author)

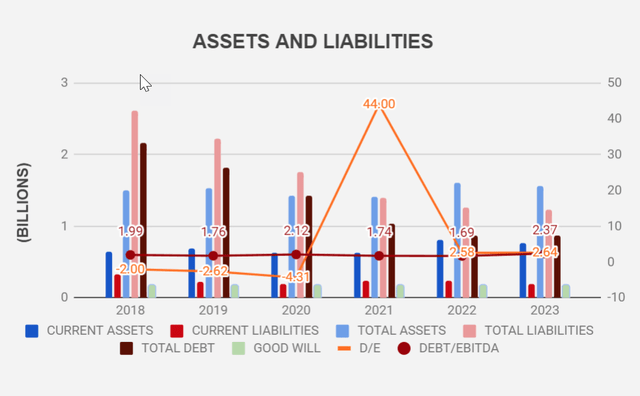

The truth is, the change happened in 2015 when the company was acquired by Brookfield Asset Management for $1.25 Billion. Brookfield quickly realized GrafTech’s potential by refocusing the company on its core business and implementing cost saving measures. By the time the company IPOed in 2018 under the ticker EAF, which symbolizes its core business – graphite electrodes for Electric Arc Furnace steel making – GrafTech posted $1.2B in EBITDA, $854 Million in Earnings and $768 Million in free cash flow. In three years, GrafTech’s EBITDA grew to what Brookfield paid for the company and was producing more graphite electrodes from three plants than it was previously doing from six. There is no doubt the turnaround was a remarkable success, so much so that it caught the attention of Monish Pabrai who invested $4.12 Million in the company in 2019 (Pabrai has since closed his position). However, the company was still facing a very high level of indebtedness and shareholder’s equity remained negative until 2021. The company has since made payments on its original $2.2 Billion debt at an astounding clip of roughly 19% per year, bringing its total debt obligations to 2.37 times TTM EBITDA (Figure 2).

Figure 2: EAF Assets and Liabilities (Author)

COVID And Russia: Two Monkey Wrenches

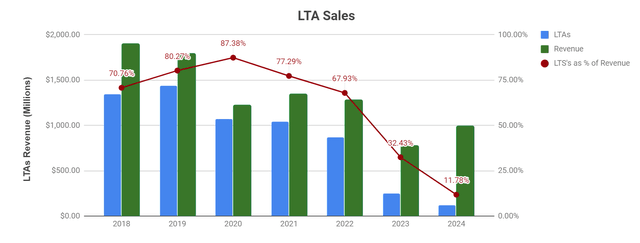

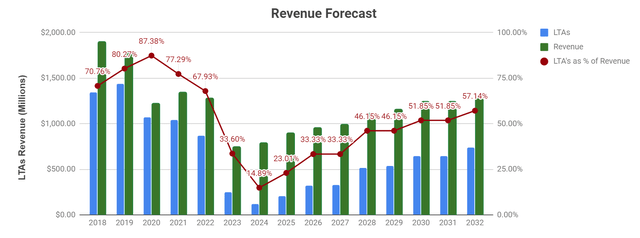

One of the key elements of this transformation was the sale of graphite electrodes to steel makers under Long Term Agreements (LTAs) which are defined by pre-determined annual volumes to be supplied to EAF’s customers. These were essentially guaranteed free cash flows for the company up to the expiration of these contracts. To give a sense of how good these were, the average price for electrodes sold under LTAs in 2020 was $9,600 per metric ton (MT) whereas the remaining sales took place at around $4,900 per MT, roughly half. With COVID, the steel industry had a hiccup, the demand for electrodes softened and many customers started failing their obligations under the LTAs leading to cancellations and legal disputes of these contracts’ terms. Some of these contracts were also affected by Russia’s invasion of Ukraine. EAF suddenly found itself at the edge of a cliff and is doing everything it can to keep all the lemmings from jumping, but many have unfortunately done so. Not only has overall revenue fallen, LTAs’ sales and LTAs’ sales as a percentage of revenue literally crashed as shown in Figure 3. The numbers for 2023 and 2024 are estimates by EAF and analysts, but the picture is painfully clear regardless.

Figure 3: EAF Revenue and LTA Sales (Author)

Adding Insult To Injury

If COVID was not enough to derail an almost unbelievable turnaround, in September 2022 Mexican authorities suspended activities in EAF’s Monterrey manufacturing facility, one of EAF’s three primary plants, the other two being Calais and Pamplona. Since Monterrey is responsible for the production of connecting pins, a crucial electrode component, the impact of this suspension was very severe. The environmental-related suspension was lifted in November 2022 but the consequences are going to be felt through the first half of 2023 according to EAF. The uncertainly imposed by the plant’s closure kept EAF from being able to commit to a portion of customers’ future purchases. Although mixed with an ongoing slump in demand, this major blow can be also seen in Figure 3 above. Revenue will reach a minimum since 2017. What appeared to be a bright future in 2018 is being eclipsed by one blow after the other. COVID led to a temporary economic slump, the Mexican authorities crippled one of EAF’s main facilities and now the quantitative easing-induced inflation is driving up the cost of goods sold. This is a lot of baggage for what is a naturally cyclical business. Are there any redemptive factors to this story?

Looking Ahead

Investors know that with the Brookfield-led changes, EAF is capable of generating healthy cash flows in a cyclical industry. In spite of adversity and a major revenue drop, free cash flow yield and free cash flow margin in the trailing twelve months sit at 9.4% and 11.6% respectively. To add some perspective, 47% of the companies in the Russel 2000 index were unprofitable in 2020. Something that works is clearly already in place. Other positive factors supporting an investment thesis in EAF are: (1) EAF is the only large graphite electrode producer that is vertically integrated, (2) the ongoing decarbonization trend in steel production favors the Electric Arc Furnace (EAF) over the Blast Oxygen Furnace (BOF) approach, (3) demand for petroleum needle coke, the raw material in graphite electrodes, is growing because of its use in batteries for electric vehicles.

Vertical Integration

Through its Seadrift facility in Texas, EAF produces most of the petroleum needle coke required for its graphite electrodes. Needle coke is produced through the refining of decant oil (also possible from coal tar but leading to a lower quality product). This asset isolates the company from changes in the price of this raw material, an advantage most of its competitors do not have.

Decarbonization Trends In Steelmaking

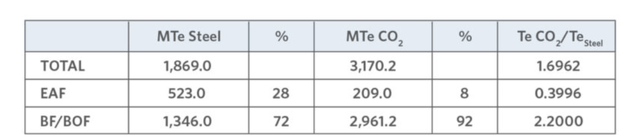

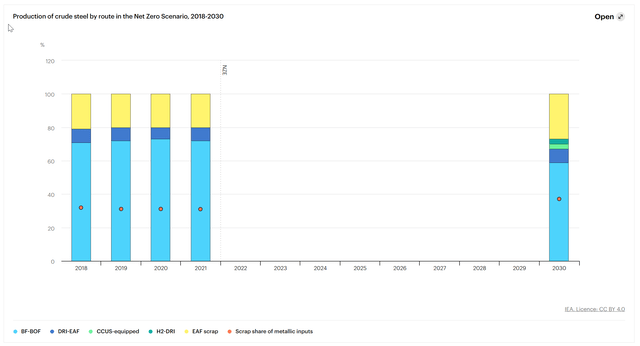

The goal of reducing CO2 emissions is touching every corner of the global economy and steelmaking is no exception. Although BOF is still the main process used in steelmaking, accounting for 72% of the world production, the trend and pressure is increasingly to replace BOF with the EAF approach to the extent that is possible. The benefits are extremely significant. The 28% of steel produced via EAF is only responsible for 8% of CO2 emissions (Figure 4).

Figure 4: CO2 emissions in steelmaking (MIDREX)

According to the International Energy Agency, efforts to put us on a net zero emissions trajectory will lead to a decline in BOF production of 10 to 15% by 2030 with a corresponding share gain of EAF production by roughly 7% (Figure 5). GrafTech itself estimates the demand of graphite electrodes to grow by 3 to 4% annually until 2030.

Figure 5: Trends in Steelmaking with Decarbonization (International Energy Agency)

Petroleum Needle Coke And The EV Industry

Although 95% of EAF’s revenue is currently derived from graphite electrodes, the production of batteries for EVs requires petroleum needle coke and this is therefore an alternative market for this raw material. Being responsible for one fifth of the high quality petroleum needle coke capacity in the world (excluding China), EAF is well positioned to take advantage of this market and the company has acknowledged it in its financial reports and investor presentations. The EV demand for needle coke is expected to outpace that of graphite electrodes by 16% per year in the next decade.

The outlook is positive, I feel like I might have gone overboard in what starts to feel like a sales pitch, and for that reason I think I need to come back down to earth and let the numbers speak. After all, Monish Pabrai has long jumped ship and EAF’s obstacles have not been insignificant. Betting on something Pabrai has rejected definitely gives me some pause, but I like to think independently and reach my own conclusions regardless.

Working Out Plausible Math

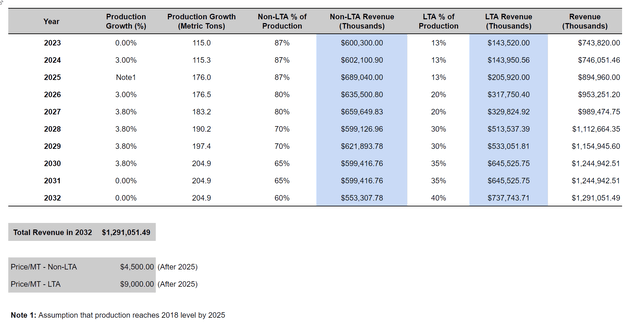

I am always conservative when forecasting future cash flows and I usually do not consider more than one scenario. The only scenario I care about is one I can believe in, which causes me to always exclude assumptions that are too rosy to begin with. Because I need to shoot for a target, adding multiple sets of assumptions only makes things blurry in my mind. I start with EAF’s own production forecast for 2023 and 2024 in terms of thousands of MT as well as growth rates over the next decade (between 3% and 4%). I grow the 115,000 MT of 2023 by 3% to 2024 and I assume that by 2025 the issues with Monterrey are sorted out and production levels are back to 2018 levels, supported by some global economic recovery. From there I grow production at the rates shown in Figure 6 until we reach about 200,000 MT, EAF’s current production capacity. I am assuming the company will not expand capacity in the next decade. The table in Figure 6 also shows my assumption that a gradual recovery in LTAs will take place, peaking at 57% of total revenue as shown in Figure 7, an extension of Figure 3 to the year 2032. I assume prices per MT of $6,000 and $9,600 for non-LAT and LTA respectively until 2025 and then cut the non-LTA price to $4,500 and the LTA to $9,000 to account for cyclicality in prices. By 2032, the total revenue will be around $1.3 Billion. This represents an annual growth rate of 6.32% between 2023 and 2032, but essentially 0% growth compared to 2022 sales.

Figure 6: EAF’s Revenue Forecast (Author)

Figure 7: Revenue Forecast Including LTA’s (Author)

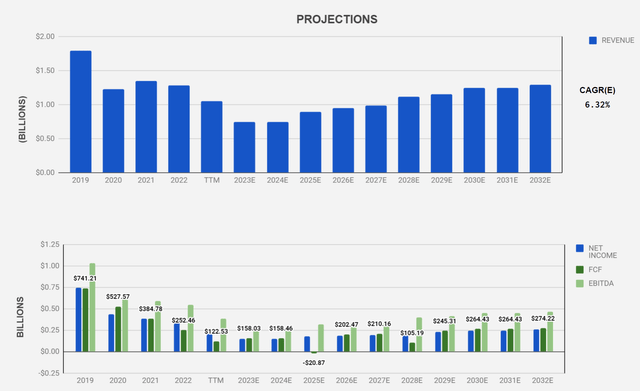

I also adjust free cash flows for years 2025 and 2028 based on historical standard deviation (Figure 8). Reality is not a perfect mathematical model and I like to add some extra cushion to absorb misjudgments in my forecast. If this scenario meets reality, EAF’s revenue in 2032 will be 72% of 2019’s numbers. I make no assumptions regarding the potential EV-related market for petroleum needle coke. The terminal value of the company is estimated using a hybrid approach that results from averaging the outcome of the perpetual growth model and an exit price to free cash flow multiple of 5.9.

Figure 8: EAF Revenue and FCF Forecast to 2032 (Author)

At this point, it’s just a matter of working out the internal rate of return (IRR) of these cash flows assuming the current stock price of $4.46 per share and adjusting for net debt. The magic number is 10.54%, roughly in line with the average annual return of the S&P 500 after 1957. In this context, the potential return is not all that magical since it is a lot easier to simply buy the index. Personally, because I consider my forecast to be at the low end of a rather cautious vision of the future, I have made a small bet on EAF (1.34% of my portfolio). This will give me the opportunity to discuss my investment prowess with future me, and it will grant me bragging rights if I end up making money with a stock thrown away by Monish Pabrai. On a more serious note, given the cyclicality of the industry, the uncertainty related to the recovery of the lucrative LTAs and the fact that the current return is on par with the expected return of the market, I would not go out of my way to buy EAF. However, if the near future turns out to be more bleak than we expect and the stock price drops further, I think EAF might be a very interesting opportunity. After all, 2023 will not be the last year humanity will be using steel.

Final Thoughts

After a praiseworthy transformation at the hands of Brookfield, GrafTech International has hit a few unexpected roadblocks that have slammed the brakes on revenue and free cash flow. However, the current economic uncertainty will eventually become less uncertain, and a few tailwinds will likely propel the business to higher free cash flow yields. Two particularly favorable factors are the global decarbonization efforts and the continued growth of the EV market, both of which will increase the demand for graphite electrodes and petroleum needle coke, the bread and butter in GrafTech’s business. Having reduced debt to very acceptable levels and sorted out the issues with its production facilities, it is now a matter of just navigating the near-term storm with the same strategy put in place in 2015. I would not recommend jumping on EAF stock head-first, but those looking for under-the-radar opportunities can definitely put this one on their list.

Read the full article here