Thesis

Axon Enterprise (NASDAQ:AXON) is one of those investments that kept coming up when I was looking for new ideas and it didn’t appeal to me because my first thought was okay, it’s just a Taser company and therefore I’m not interested in looking at it any further. But damn was I wrong, the first time I looked at it closely I saw their great business model and big competitive advantage and future growth opportunities.

I am sure that a company like Axon will be of real benefit to humanity by preventing unnecessary deaths and I also believe that Evidence could improve the quality of investigations and therefore help to reduce the number of innocent people convicted or help to convict the guilty.

And I think that investing in things that make our lives better will often lead to excellent results in the long run. However, Axon’s valuation is very high and this has a rather negative impact on the risk/reward at the moment. But with the volatility of the share price, I think there will be buying opportunities in the future, as with almost any stock.

And when there is negative sentiment due to temporary difficulties, I will build a position, as patience is key in this case, but the right time will come.

Analysis

There has been some good news for Axon recently, with its inclusion in the S&P 500 and strong recent results. However, the share price fell relatively sharply after the results for no real reason other than that the shares have no margin for error due to their very high valuation and therefore such falls can occur. Nevertheless, this creates opportunities for new investors to find cheaper entry points, and I think Axon’s long-term path will have quite a few ups and downs. You just have to take advantage of Mr Market’s mood swings.

Competitive Advantage

The combination of body cameras, digital evidence system and Tasers has enabled Axon to build a system that is mission critical for customers once they use it long enough. It makes the work of the officers easier as the Evidence System takes over more and more of the work and automates it. And the more data Axon collects, the more they can automate and drive customers further into system dependency. And this leads to unimaginably high switching costs and a strong customer relationship.

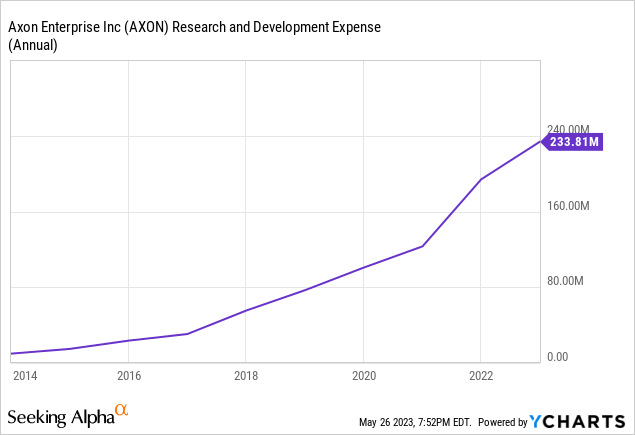

Evidence is likely to be Axon’s core business going forward, which should lead to improved margins, and I think their R&D spending will also lead to more interesting future opportunities as they can really benefit from AI and machine learning. Unlike other companies, AI for them is not just a word that is thrown around in earnings calls or quarterly reports to please shareholders.

Rising R&D costs should be welcome news to all shareholders, as this is an investment in the future and long-term investors are likely to benefit from this investment in the future.

The FedRAMP High classification, the highest level of security certification which they have recently achieved, is also a strong barrier to entry as they can now work with data that other competitors cannot.

In addition, once you are in the Axon ecosystem, it is hard to get out because all the pieces are connected. And through the cloud, Axon is also getting more and more recurring revenue because they get subscription revenue and their Tasers, for example, also need cartridges, which is also recurring revenue. Rather than just getting paid once for a product, they have moved to this more efficient model.

Growth Opportunities

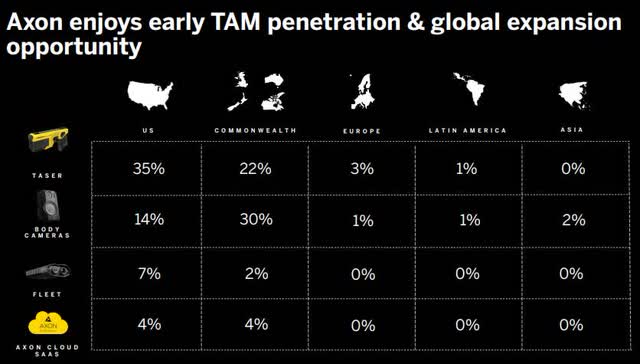

Axon Investor Deck May 2023

This clearly shows that TAM is under-penetrated, especially in LA, Europe and Asia, and once they get their foot in the door with the Tasers and get the customers in their ecosystem, the cross-sell and up-sell opportunities will be there. The TAM is currently $50 billion according to their calculations.

Especially in Europe there are more and more riots and demonstrations, so I don’t think they’re going to cut back on police spending, rather the opposite, and that would benefit Axon. Latin America, on the other hand, is a difficult issue because you have criminals who are really heavily armed and they may not take the police with tasers very seriously.

Reverse DCF

Author

The basis of the reverse DCF is the TTM diluted EPS of $1.88, which implies an EPS growth of 26% over 5 years and then 25% over the next 5 years. The historical growth rate over the last 10 years is only 21.90%, so if you want to achieve a 10% CAGR, the shares are currently overvalued.

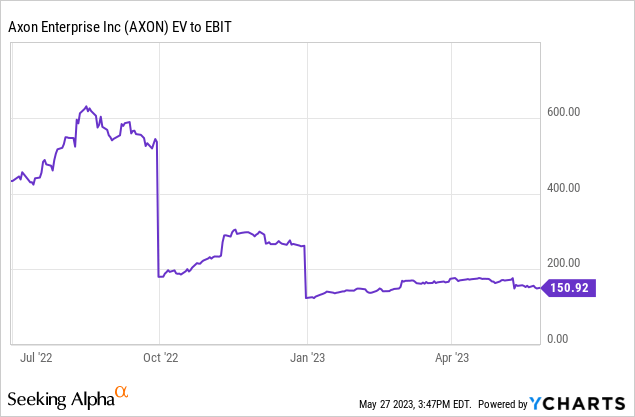

A metric like EV / EBIT also shows that the shares are massively overvalued, but we have to admit that the valuation has improved somewhat over the last 3 years. And even if we use a metric that includes the growth rate, such as the PEG ratio, we get a figure of over 2.5, which also shows the overvaluation.

Conclusion

Axon is a high quality company that I would like to own, but I would not start a position at this valuation. Entry points that are too high simply steal too much of the future returns, and better entry points are often offered, which you then have to take advantage of.

I have no major criticisms of Axon as a company, as the business model is excellent, the execution is also high quality and the future growth opportunities are plentiful. They also have strong barriers to entry and competitive advantages, and every day that customers use their product, they become more dependent on it. The interests of the shareholders are also aligned with those of the CEO, as he has a stake in the company through his ~4% stake, and he has a mission with this company that he wants to achieve.

Read the full article here