Atomera Incorporated (NASDAQ:ATOM) is the inventor of a technology called MST (Mears Silicon Technology), a thin film of re-engineered silicon that can be applied as a transistor channel enhancement to CMOS-type transistors.

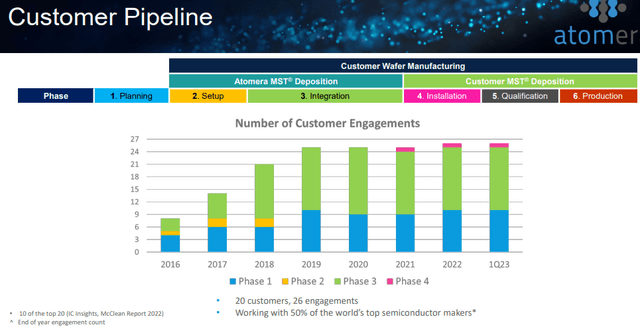

Market adoption is a very slow-moving process, with 20 companies in various states of trials.

ATOM IR presentation

The company is finally able to enjoy its first production win with STMicroelectronics N.V. (STM), and this is a significant win, possibly a company-altering event.

- This is a big and high-profile win that visibly removes lingering doubts about market acceptance of the MST technology.

- It might very well get other customers over the line in the form of domino theory (or even just to maintain competitiveness versus STM).

- But even STM is going to move slowly, royalty payments (the holy grail of the company) are expected only in the coming 18-24 month time frame.

- The first of two milestone payments will happen when STM installs the MST technology on an EPI deposition tool in one of their fabs) and could arrive in Q2, but it’s more likely to be Q3 as STM suffers from some internal delays with the tool modification.

- Once installation is complete and STM has successfully dialed in the tool, they will be ready to build MST wafers and the companies will work on integrating the MST film into STM’s devices to create an optimized new design flow, followed by a manufacturing process qualification (roughly a 9-month process, on average).

- Upon wafer-level qualification, STM will officially be in production, triggering a second milestone payment and sales will produce royalty payments.

- STM is going to use it in its flagship smart power products, which is a large application.

- The license is for a node and half a node shrink, anything beyond that requires a new license agreement and royalties go up in terms of dollars per wafer as wafers on lower nodes cost much more.

While STM might still back out, given the fact that they have not exactly hurried this decision (STM signed the first integration license in early 2018), the odds for that seem particularly low.

For obvious reasons, management isn’t going to disclose what kind of milestone or royalty payments the company might receive from STM, but here is an earlier general ballpark (Q1 2023 CC):

we’ve been talking about a business model that had a kind of our list price of upfront milestone payments would be is total of about $3.2 million. And then our royalties that we were looking for a range between 1% and 3%.

The royalty rate for the first customer is likely to be on the lower side, but it depends on the amount of gross margin their technology brings to clients.

Royalties start high and come down when volumes increase at a particular customer. Royalty per wafer increases when clients move to new smaller nodes (as well as triggering a new license contract).

There is some progress in some of the other clients as well (Q1CC):

Likewise work with JDA number two is ongoing with new experiments to follow-up on our initial trials and as specified in our JDA, if we can meet those requirements, we will have milestone payments to announce. We are also active with each of our four other licensees including ST, who we’ve discussed earlier and AKM who had gone into a pause after a fab fire in 2020. We are now planning to resume our work with AKM either at their facilities or through a foundry partner.

There are also opportunities in new segments like memory (Q1CC):

Further, we are encouraged by better traction with memory customers themselves. I have not highlighted this area in the past as the memory customers are particularly challenging to break into, but we are confident in the big gains MST can bring to this space and hope to see adoption in that market in the future.

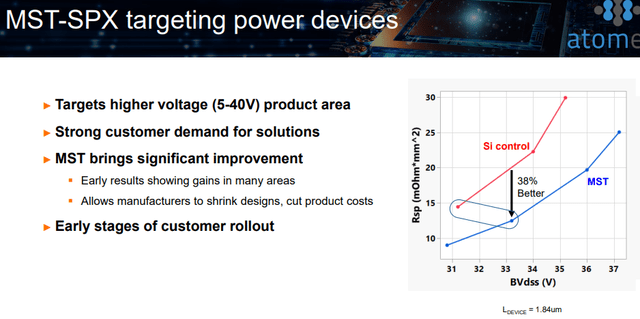

And also power devices.

Power devices

ATOM IR presentation

Here is the relevant part from the Q1CC on their MST-SPX technology:

In discussions with customers about our 5-volt power management focused solutions, we are consistently asked if MST can help for higher voltage transistors up to the 40-volt range used in a wide set of applications requiring greater power.

Over a year ago, Atomera started designing silicone to enhance these very hard to improve devices. Our early test data shows very promising results in this slide gives one of the most important specs from our first silicone. MST brings both lower on resistance and higher breakdown voltage, so reading the graph vertically we see a 38% lower on resistance at the same breakdown voltage, which would be extremely attractive to power device manufacturers.

If this technology continues to progress as we hope, it will open up a much larger slice of the power market for us

Bosch is buying TSI, their third-party foundry

There are a few possible implications:

- While Bosch is buying TSI for the SiC market, it is going to continue the TDCS (technology development area) under which Atomera falls, at least for some time.

- TSI uses Atomera’s MST technology in their manufacturing, Bosch could offer the tantalizing possibility of expanding this when they familiarize themselves with the advantages.

So this could be both negative and positive, jury still out.

Finances

Apart from milestone payments, which tend to be lumpy, the company doesn’t generate revenues yet. OpEx is always highest in Q1, but management expects FY23 non-GAAP OpEx to be between $16.25M-$16.75M.

This will roughly be their cash burn if there are no milestone payments, but at least one of these (from STM) is expected. The company had $17.1M in cash and equivalents left at the end of Q1.

The company also has an ATM facility, but that’s not much in use due to the low share price (they sold 49.6K shares in Q1 at an average price of $6.40 per share). Management does argue that it’s still likely to be their cheapest source of finance.

The company roughly has a market cap of $225M (at $9 per share), the company could be worth a multiple of this in 4–5 years’ time.

Conclusion

The STMicroelectronics N.V. deal is likely to be a company-altering event for Atomera Incorporated, something investors have waited years for. It could very well induce other customers to speed up and reach such agreements as well.

If Atomera Incorporated is good enough for STM, it should be good enough for others. We should keep in mind that STM didn’t exactly take a rash decision, this is the result of years of evaluation.

But keep in mind, this is a very slow-motion process, taking place years rather than months or weeks. Even the royalties from STM are likely to be 18 months away at the minimum.

The company has cash for at least another four quarters, and milestone payments and their ATM could stretch that into the firmer grounds of royalty earnings, but that’s far from a given.

So there are still considerable risks, but the risk/reward situation for Atomera Incorporated has shifted notably for the better.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here