Co-authored with “Hidden Opportunities.”

In today’s world, we don’t like to wait for anything. Shipping should be immediate, groceries should be delivered within hours, and our ride should be ready to pick us up as we exit the airport. There is one thing, in particular, I detest waiting for – food at a restaurant.

I enjoy a full-course meal comprising an appetizer, the main course, and dessert. And I will be happy if the next course comes in as I am ready for it. I guess that explains why I like dividends so much.

“Good return on dividends means at least you have an appetizer to eat while waiting for the main dish.” – John Neff.

I like my investments to appreciate, but I am impatient to sit hungrily. I am enjoying my appetizer in the form of regular dividend payments, knowing that a tasty main course will arrive just in time. And there is also dessert. Today’s discounted dividend securities have the potential to offer raises and capital upside, both perks missing from guaranteed instruments like Certificates of Deposit (“CDs”) and Money Market funds that are paying historically high-interest rates.

With guaranteed instruments, you have your appetizer, but no main course or dessert is coming in when you are done. With inflation visibly slowing down in 2023, we are close to the end of this interest rate cycle. Once Mr. Market starts pricing in a full interest rate “pause,” or if interest rates start to decline, dividend stocks are set to soar, and the dividend yields will shrink. We are right at that point in time! Therefore, the vouchers for the three-course meal are almost out.

We highlight two +7% yielding picks to act fast before you miss out on this opportunity of a lifetime.

Pick #1: UTG – Yield 8.3%

With a recession expected to hit the U.S. economy as soon as a few months, boosting your allocation to defensive sectors is a good idea.

Utilities are historically a defensive sector of the market due to the following factors:

-

Steady earnings growth: The demand for electricity, natural gas, water, and wastewater services will stay strong regardless of the state of the economy.

“Companies that make products that consumers buy regardless of the economic environment — think diapers and utilities — do quite well because individuals continue buying them” – Ariel Acuña, founder of LTG Capital.

-

Dividend Focused: Most utility companies pay dividends, providing their shareholders with a reliable income stream. Notably, companies from this non-cyclical sector are deemed “widow and orphan stocks” due to their stable cash flows, predictable earnings, and stable income for risk-averse investors.

-

Regulatory Protection: Utility companies are subject to significant regulatory oversight, protecting them from competition. Additionally, these companies protect their profit margins by securing regulatory support to pass on rising costs to their customers. Most importantly, environmental legislation greatly influences utilities’ growth opportunities as companies expand their asset base with powerful incentives from local, state, and federal government bodies.

Despite utilities being attractive in this uncertain economy, individual companies are susceptible to environmental (weather-related) and operational (infrastructure-related) risks. Moreover, companies can easily reprioritize their capital allocation goals, and we have no say in that decision. For income investors, diversification is a powerful ally to ensure the safety and sustainability of dividends.

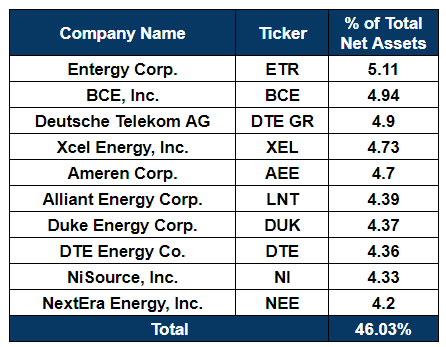

Reaves Utility Income Fund (UTG) is a Closed-End Fund (“CEF”) focusing on current income.

UTG is diversified across 44 holdings, and its top 10 constituents are some of the largest utility and telecom companies globally, well-positioned to maintain their execution through thick and thin. Source.

Utilityincomefund website

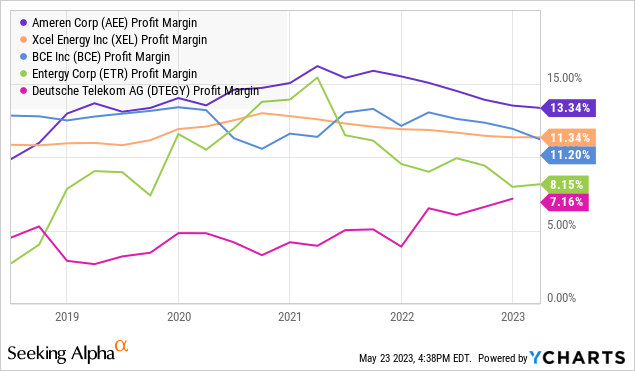

Despite pandemic conditions and high and low interest rates, the fund’s top holdings have maintained, if not strengthened, their profitability in recent years.

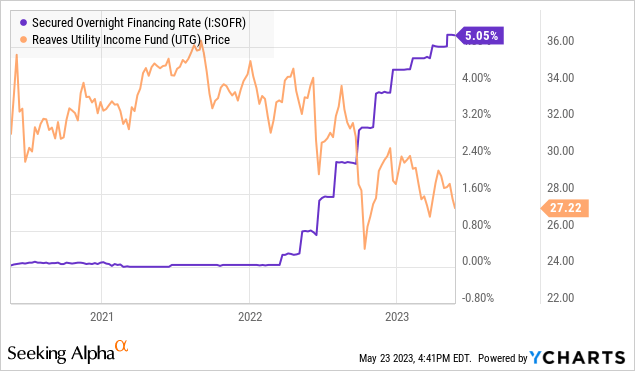

UTG pays monthly distributions of $0.19/share. At current prices, this calculates to an 8.3% annualized yield. It is important to remember that UTG is actively managed. We expect management to opportunistically move in and out of positions to realize returns for us.

UTG is modestly leveraged at 20% to boost its holdings’ dividend income and gains. Interest is charged at a rate of the one-month Secured Overnight Financing Rate (“SOFR”) plus 0.65%. Rising borrowing costs have hurt the CEF’s NAV since the beginning of quantitative tightening.

However, we are close to the end of raises in this rate cycle, and UTG is better positioned to grow NAV as rates are held or poised to move downward. With UTG trading almost at par with NAV, this is an excellent time to buy at these elevated yield levels and boost a recurring income portfolio.

Pick #2: VZ – Yield 7.2%

Verizon Communications Inc. (VZ) has been one of the Dogs of the Dow since the Fed’s rate hikes began. As an income investor, such stocks from industries with limited competition, inelastic demand, sector-leading profit margins, and a solid track record of dividend growth present meaningful buying opportunities. We get paid an attractive fee to wait for them to get back in favor.

VZ reported Q1 2023 earnings on April 25th, and at a high level, everything is progressing per management’s original guidance for the fiscal year.

VZ has consistently stood tall with profitability in the U.S. telecom industry, and Q1 was no exception. The company continued to lead with a 41.5% EBITDA margin, in comparison with AT&T Inc.’s (T) 40.7% and T-Mobile US, Inc.’s (TMUS) 34%.

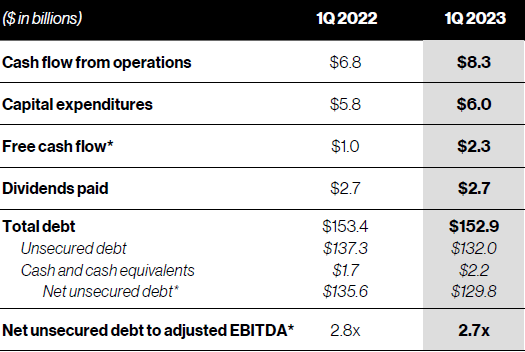

The company is expected to have 17% less Capital Expenditure, supporting Free Cash Flow (“FCF”) growth and leaving management optimistic about another dividend increase later this year.

Mr. Market continues to fixate on the fact that Q1 dividends exceeded the FCF generated by the company during the quarter. VZ paid $2.7 billion for Q1 distributions when FCF was $2.3 billion. And that calculates to a 117% FCF payout ratio. Source.

VZ Q1 Webcast Presentation

We explained in an Earnings Update on AT&T that FCF tends to be lumpy, especially in this industry where companies are expected to make large Capital Expenditures towards 5G and Fiber. Looking at Trailing Twelve Month FCF (Q2, Q3, Q4 2022, and Q1 2023), we see $15.35 billion FCF and $10.9 billion towards common stock dividends. This indicates a ~60% FCF payout ratio, which is a healthy metric.

VZ hasn’t provided a formal FCF guidance for FY 2023, but CEO Hans Vestberg said during the Q4 conference call that the $17 billion an analyst projected was within the ballpark. Assuming a 3% dividend raise in Fall 2023, if VZ were to spend $11.1 billion on common dividends, it would come at a 57-60% payout ratio. VZ has also provided an Earnings Per Share (“EPS”) estimate of $4.55-4.85 for FY 2023, which places its projected annual $2.6/share dividend at a modest 53-57% EPS payout ratio. Both metrics based on FY 2023 earnings guidance indicate that a modest dividend raise will be adequately supported.

At the end of Q1, VZ’s net unsecured debt to adjusted EBITDA ratio was approximately 2.7x. The company maintains an investment-grade A- rated balance sheet and has low near-term unsecured debt maturities, with only $600 million due this year in Q2. VZ ended Q1 with $3.9 billion in cash and cash equivalents on its balance sheet.

Rising rates make dividend stocks less attractive. But a ~7% qualified yield from a leading provider of services critical to the digital economy is something to pay attention to. We don’t know what Mr. Market will do next, but VZ is trading at dirt-cheap valuations and is well-positioned to execute and deliver its guidance and raise dividends to shareholders. At current prices, VZ fits well in a long-term income portfolio for sustainable and growing income.

Conclusion

Have you played or heard of Age of Mythology? It was among the top PC games of 2002 from Microsoft Studios. It involved players choosing ancient civilizations and pursuing the strategic collection of essential resources to humankind – Food, Wood, and Gold. Players work towards building an army and citizenry, fighting enemy units, and capturing their towns. The Greek Civilization, in particular, had a buildable monument called “Plenty Vault.” This unique monument automatically generated three units of food, wood, and gold every 5 seconds; no action was required from the player, effectively supplementing the broader resource aggregation efforts.

In the same sense, dividend stocks are the Plenty Vault of the real world. No matter how the market moves, I get a predictable and reliable cash infusion. And I am buying as much as I can when they are on sale.

“Don’t look for the needle in the haystack. Just buy the haystack.” – John Bogle.

Now is the time to act, as interest rates have likely peaked and start declining soon. At High Dividend Opportunities, we are buying the haystack in the form of our comprehensive “model portfolio” of +45 dividend payers with an overall yield of +9%. We are locking-in “once in a lifetime” dividend opportunities. There are excellent yields available at “dirt cheap” prices, but not for long. Don’t wait until it is too late. You can get started with these two +7% yields!

Read the full article here