A Quick Take On GoDaddy

GoDaddy (NYSE:GDDY) reported its Q1 2023 financial results on May 4, 2023, missing both revenue and EPS consensus estimates.

The firm provides a suite of website hosting and related services worldwide.

I previously wrote about GoDaddy with a Hold rating here.

While its U.S. payments business is a bright spot with substantial growth potential, total revenue growth is still falling short of past years.

Until management can reignite double-digit revenue growth, as it says it will do, I’m still on Hold for GDDY.

GoDaddy Overview

Tempe, Arizona-based GoDaddy was founded in 2014 to provide a suite of website hosting services to organizations around the world.

The firm is headed by Chief Executive Officer Aman Bhutani, who was previous President, Brand Expedia Group and Technology Senior Director at JPMorgan Chase.

The company’s primary offerings include:

-

Website Hosting.

-

SSL Certificates.

-

Website Creation Software.

-

Digital Marketing.

-

Business Applications.

-

Payments.

-

Search Engine Optimization.

GDDY serves individuals, businesses, developers, and domain investors.

GoDaddy’s Market & Competition

According to a 2020 market research report by Grand View Research, the global market for web hosting services was an estimated $56.7 billion in 2019 and is forecast to reach $180 billion by 2027.

This represents a forecast strong CAGR of 15.5% from 2020 to 2027.

The main drivers for this expected growth are the growing number of individuals and companies seeking a web presence and an increased desire to perform more business functionality in the cloud.

Also, the onset of the COVID-19 pandemic has generated strong growth in Internet-based activity, providing a boost to the industry.

Major competitive or other industry participants include:

-

Automattic.

-

Wix.

-

Weebly.

-

Shopify.

-

BigCommerce.

-

Squarespace.

-

Mailchimp.

-

MindBody.

-

Others.

GoDaddy’s Recent Financial Trends

-

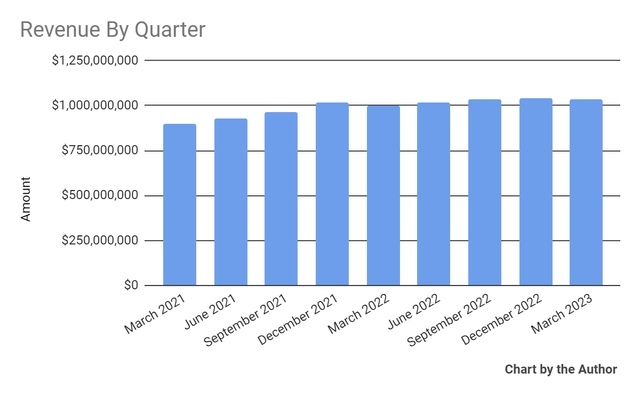

Total revenue by quarter has grown per the following chart:

Total Revenue (Seeking Alpha)

-

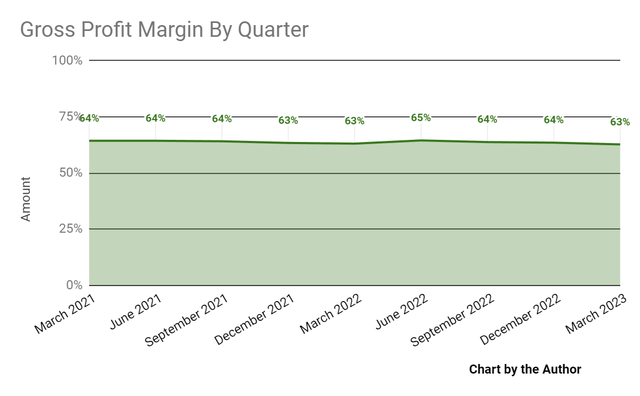

Gross profit margin by quarter has remained stable:

Gross Profit Margin (Seeking Alpha)

-

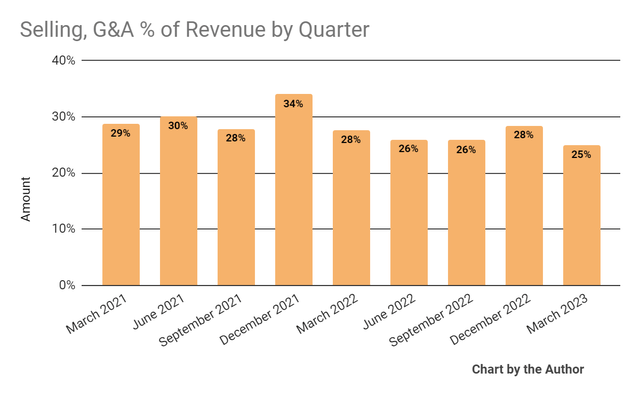

Selling, G&A expenses as a percentage of total revenue by quarter have dropped in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

-

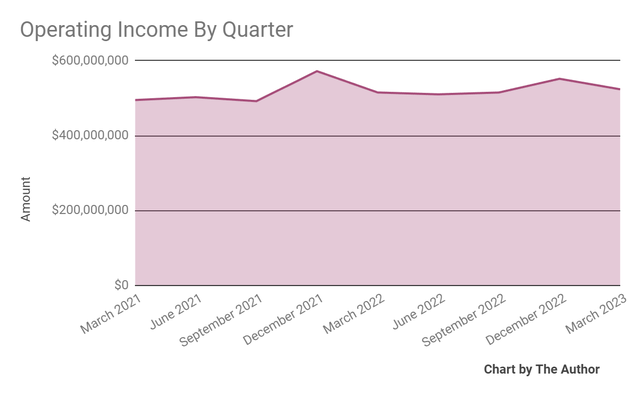

Operating income by quarter has remained flat more recently:

Operating Income (Seeking Alpha)

-

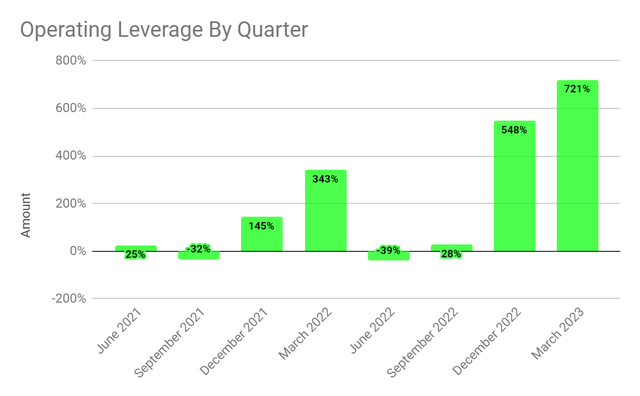

Operating leverage by quarter has increased significantly in recent quarters:

Operating Leverage (Seeking Alpha)

-

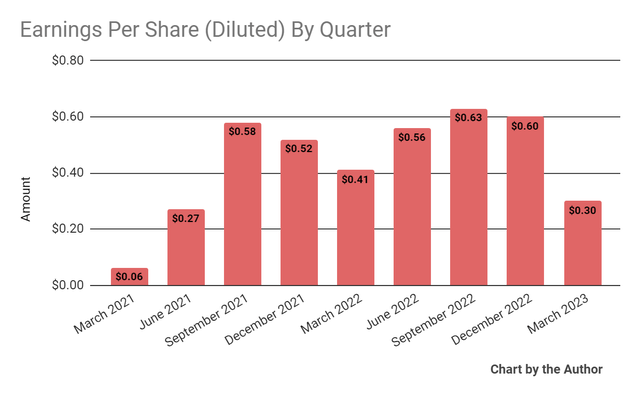

Earnings per share (Diluted) have fluctuated per the chart below:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

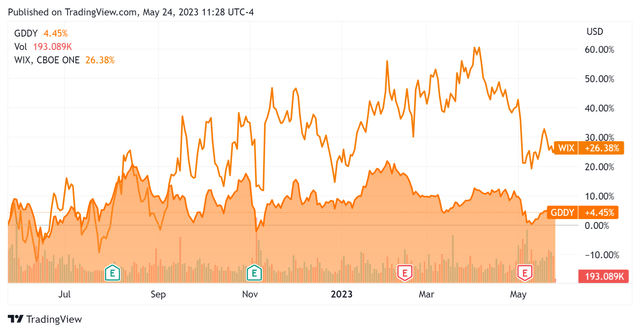

In the past 12 months, GDDY’s stock price has risen 4.45% vs. that of Wix.com Ltd.’s (WIX) growth of 26.38%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

For the balance sheet, the firm ended the quarter with $1.05 billion in cash, equivalents, and trading asset securities and $3.83 billion in total debt, of which only $18.3 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was an impressive $928.9 million, of which capital expenditures accounted for $70.2 million. The company paid a hefty $277.1 million in stock-based compensation in the last four quarters, the highest rolling twelve-month total for the last eleven quarters.

Valuation And Other Metrics For GoDaddy

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

3.4 |

|

Enterprise Value / EBITDA |

19.6 |

|

Price / Sales |

2.8 |

|

Revenue Growth Rate |

5.3% |

|

Net Income Margin |

8.0% |

|

EBITDA % |

17.4% |

|

Market Capitalization |

$11,210,000,000 |

|

Enterprise Value |

$14,100,000,000 |

|

Operating Cash Flow |

$999,100,000 |

|

Earnings Per Share (Fully Diluted) |

$2.09 |

(Source – Seeking Alpha)

As a reference, a relevant partial public comparable would be Wix.com (WIX); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Wix.com |

GoDaddy |

Variance |

|

Enterprise Value / Sales |

3.0 |

3.4 |

12.9% |

|

Enterprise Value / EBITDA |

NM |

19.6 |

–% |

|

Revenue Growth Rate |

8.4% |

5.3% |

-36.8% |

|

Net Income Margin |

-14.6% |

8.0% |

–% |

|

Operating Cash Flow |

$96,780,000 |

$999,100,000 |

932.3% |

(Source – Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

GDDY’s most recent Rule of 40 calculation was 22.7% as of Q1 2023’s results, so the firm is in need of some improvement in this regard, per the table below:

|

Rule of 40 Performance |

Calculation |

|

Recent Rev. Growth % |

5.3% |

|

EBITDA % |

17.4% |

|

Total |

22.7% |

(Source – Seeking Alpha)

Commentary On GoDaddy

In its last earnings call (Source – Seeking Alpha), covering Q1 2023’s results, management highlighted the growing optimism by the firm’s customer base.

The firm exceeded a $1 billion annual run rate in gross payment volume for its U.S. payment platform services.

However, the company’s aftermarket resales and large transaction segments have become unpredictable and subject to ongoing volatility.

The company also experienced continued foreign exchange headwinds in its international business due to a strong US dollar.

GoDaddy’s customer retention rate was 85% in Q1, indicating modest sales & marketing efficiency.

Total revenue for Q1 2023 rose 3.3% year-over-year and gross profit margin fell 0.3 percentage points.

Selling, G&A expenses as a percentage of revenue dropped 2.7 percentage points year-over-year and operating income grew by 1.6%.

Looking ahead, for the full-year 2023, management guided to 5% topline revenue growth at the midpoint of the range, while stating they see a return to double-digit growth sometime in the future while not sacrificing profitability.

The company’s financial position is moderate, with substantial liquidity but relatively high long-term debt; free cash flow has been impressive over the past 12 months at nearly $930 million.

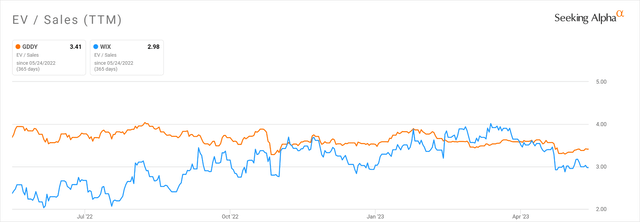

Regarding valuation, by comparison to WIX, the two companies’ EV/Sales multiples have converged in recent months with WIX’s multiple improving relative to that of GDDY, as the chart shows here:

EV/Sales Multiple History Comparison (Seeking Alpha)

The primary risk to the company’s outlook is a slowdown in the global economy, driven by higher cost of capital and a growing concern over credit availability, at least among U.S. customers.

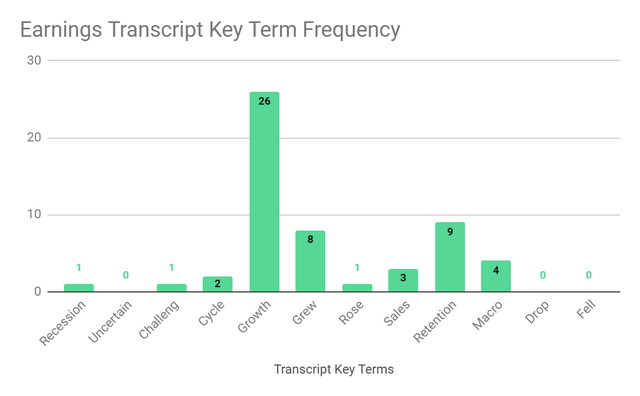

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management cited ‘Recession’ once, ‘Challeng[es][ing]’ once, and ‘Macro’ four times.

The negative terms refer to difficult macro conditions that have negatively impacted the flow of larger deals as companies delay purchases until the economic outlook improves.

A potential upside catalyst to the stock could include a drop in the cost of capital, reducing the negative pressure on stock multiples.

However, after 2022’s annual revenue growth of 7.2%, management has downgraded its 2023 growth rate to 5%, a meaningful drop.

While its U.S. payments business is a bright spot with substantial growth potential, total revenue growth is still falling short of past years.

Until management can reignite double-digit revenue growth, as it says it will do, I’m still on Hold for GDDY.

Read the full article here