Investors like certainty in an uncertain world, and perhaps that’s why tech juggernauts in the Nasdaq have had a banner year so far. However, one hardly makes money in the stock market by chasing crowd favorites and it pays to have a contrarian mindset and buy beaten down quality value stocks when the market simply isn’t interested.

This brings me to Federal Realty Investment Trust (NYSE:FRT), which as shown below, now trades below $90, and sits just shy of its 52-week low. I last covered FRT here back in April, highlighting the quality of its portfolio. In this article, I discuss why now may be a great time to layer into this premier REIT for income and potentially strong gains.

FRT Stock (Seeking Alpha)

Why FRT?

Federal Realty Investment Trust is one of the oldest REITs on the market today, having been around for six decades. It’s also a Dividend King with 50+ years of dividend growth. FRT’s portfolio of 102 shopping center and mixed use properties cover 3,200 tenants and 3,100 residential units.

What sets FRT apart from peers is its focus on quality over quantity. This includes having properties in Tier 1 gateway markets on both U.S. coasts as well as Phoenix and Chicago. Compared to its large peers such as Regency Centers (REG) and Kimco Realty (KIM), FRT also has the lowest percentage (10%) of median households in its vicinity having annual income less than $75K.

FRT boasts the highest population density and median household income compared to its peer group, with an average population size of 177K within a 3-mile radius of its properties and an average household income of $151K.

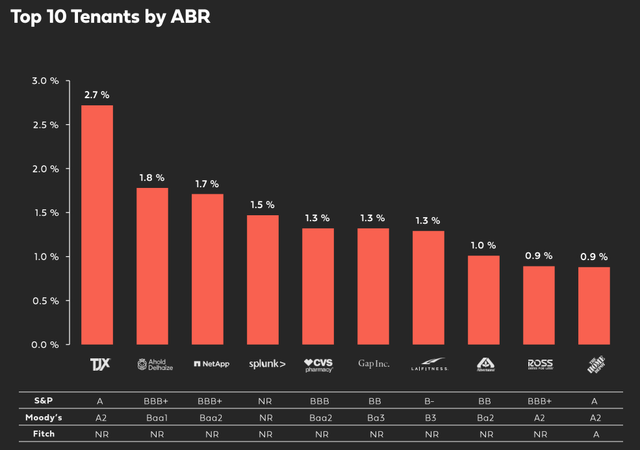

This combined with high barriers to entry due to high property values results in durable competitive advantages for FRT. It’s also well diversified by tenant, with no tenant representing greater than 2.8% of annual base rent. As shown below, FRT’s top 10 tenants are a mix of retailers and tech companies (in mixed use centers), including TJX (TJX), NetApp (NTAP), Splunk (SPLK), and CVS (CVS).

Investor Presentation

Meanwhile, FRT is growing quite well amidst economic uncertainty, with FFO per share rising by 6% YoY to $1.59 during the first quarter. This was driven by 3.6% same-store NOI growth over the prior year period. FRT is also seeing healthy demand, as it has a 94.2% leased rate, which grew by 50 basis points YoY.

In particular, FRT’s premier properties, Assembly Row, Bethesda Row, Pike & Rose, and Santana Row are key differentiators in the portfolio with 98% occupancy and tenant sales that are well above 2019 levels.

Near term headwinds include the recent bankruptcy of Bed Bath and Beyond, which has limited impact on some of FRT’s properties. The good news is that BBBY’s properties have a low base rent of $15 per square foot, which management expects to be able to easily lease up when they become available late next year.

Moreover, while talks of a recession may be cause for concern, it’s important to consider that retail locations are a primary source of income for some private operators, and that a flight to quality is currently underway with FRT not seeing a decline in the leasing pipeline but rather a robust uptick, as noted during the recent conference call:

We’re seeing great demand on the retail leasing side, specifically in the small shops. We have not seen a decline of anything considerable as it relates to people’s ability to fund projects and make decisions.

They’re making decisions for the long term, and they’re understanding that with these recession discussions that these headwinds that we’re facing, the decisions that they’re making are critical to their livelihood, especially for the mom-and-pop.

There’s a flight to quality that continues to happen in our portfolio. I’m feeling very bullish about what I see in our pipeline. Again, I honestly, I was expecting it to level off a little bit, and it has not. It is as robust as ever. So, I’m very encouraged.

Meanwhile, FRT carries a solidly investment grade BBB+ credit rating from S&P, and is reasonably leveraged with a net debt to EBITDA of 6x. Management expects to get to mid-5x next year. It also has a robust $740 million pipeline, with only $250 million in remaining spend, which can be easily fulfilled with FRT’s $1.3 billion in available liquidity on tap.

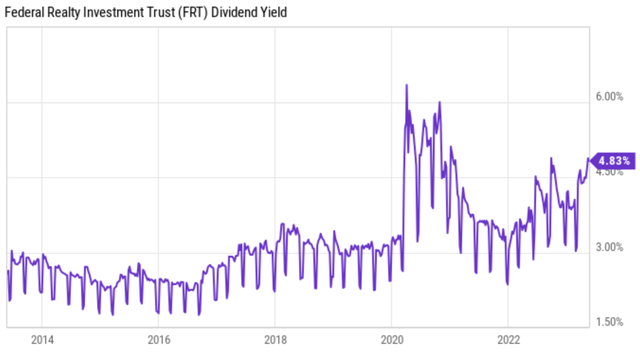

Importantly, FRT currently yields 4.8%, and the dividend comes with a 68% payout ratio and 54 years of consecutive growth. As shown below, FRT’s dividend yield now sits at around its highest level over the past 10 years outside of the early pandemic timeframe.

YCharts

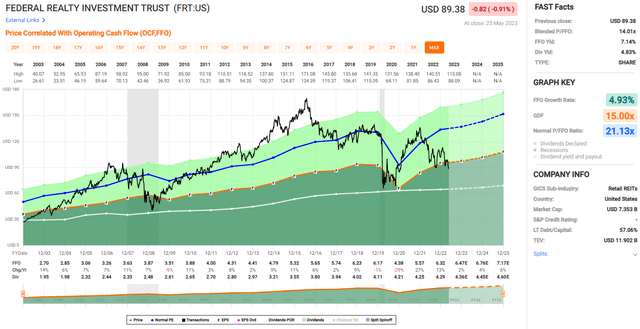

Lastly, FRT now appears to be dirt cheap at the current price of $89.38 with a forward P/FFO of 13.8, sitting far below its normal P/FFO of 21.1. Analysts have a consensus Buy rating with a conservative average price target of $115, which equates to a forward P/FFO of 17.7. Even if we assume a low fair value P/FFO of 15, FRT could very reasonably deliver a potential 13% total return over the next 12 months.

FAST Graphs

Investor Takeaway

Federal Realty Investment Trust is one of the premier names in retail REITs and now appears to be a bargain given its stable portfolio and growing portfolio, strong tenant base, investment grade credit rating, and solid and historically high dividend yield.

With a well below average valuation and robust leasing pipeline, FRT could potentially deliver double-digit total returns over the next 12 months. As such, such value investors seeking a sleep-well-at-night type investment may want to seriously consider FRT at its current deeply discounted level.

Read the full article here