This article was published at iREIT on Alpha on Tuesday May 23, 2023. Coproduced with Wolf Report.

Dear readers/followers,

I’ve taken a look at Brandywine Realty Trust (NYSE:BDN) before, and I do own a small stake in the company. This is based on the overlooked current nature of the entire office sector and the underlying quality of the assets we do have here when we look at the business.

Smaller real estate investment trusts, or REITs, naturally come with larger risks.

That’s the reason my own exposure to them is relatively limited – unless they come in at significant quality. And BDN is a smaller REIT. It also doesn’t take any sort of university degree to understand that a 20%+ yielding REIT might have some elevated risk compared to one that trades at 5-8% in this sort of environment.

So why am I keeping my stake in BDN, and sometimes considering expanding my stake?

Updating On Brandywine Realty Trust – Little Long-Term Fundamental Softness Indicated

When I say little, I am not saying that there is no softness implied in this REIT. That is why, I believe, the REIT is currently trading at below 3x P/FFO, and why out of all Office REITs we follow, BDN is one of the most impacted by the downturn. It’s also been “down” for the longest time, starting its decline all the well over a year ago, rather than in the summer or fall of 2022.

The company is BBB-rated, making it the worst-rated office REIT I invest in.

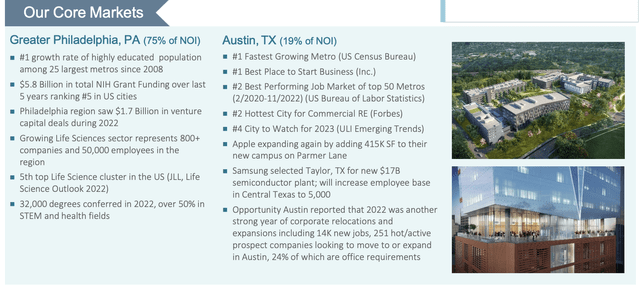

The BDN REIT was founded in 1994. It technically has buildings in five “markets” – Philadelphia CBD (or central business district), the Philly suburbs, Austin, TX, Metro D.C, and a geographical area simply called “other.”

The company can trace its roots back to 1986 as a Maryland REIT, and its current headquarters are in Philadelphia. Some or many of the risks associated with the business are in fact due to its operating geographies, which are more limited and more concentrated than other office REITS.

The company manages over 75 properties in these areas with a 90%+ occupancy and a total lettable area of 13M sq. ft. From those leases, it generates an annualized base rent, or ABR, of over $330M.

However, calling the company a “pure-play” Office REIT is somewhat wrong – at least when looking at its land bank, which it does own and could use to develop properties that are 36% residential, 27% office, and 21% life science.

The company doesn’t downplay its current operating challenges. The focus is on improvement to coverage ratios, maximization of liquidity, and improving what it can in the current environment. It’s important to note that BDN is actually holding a debt portfolio that’s 96% at fixed rate, which lowers exposure and risk somewhat.

However, its main challenge and risk is overexposure to the Philly market.

BDN – Investor Relations

While BDN is actively expanding its footprint, doing so in this environment while maintaining its payouts and quality is a Herculean challenge. This is another reason I believe the company is down.

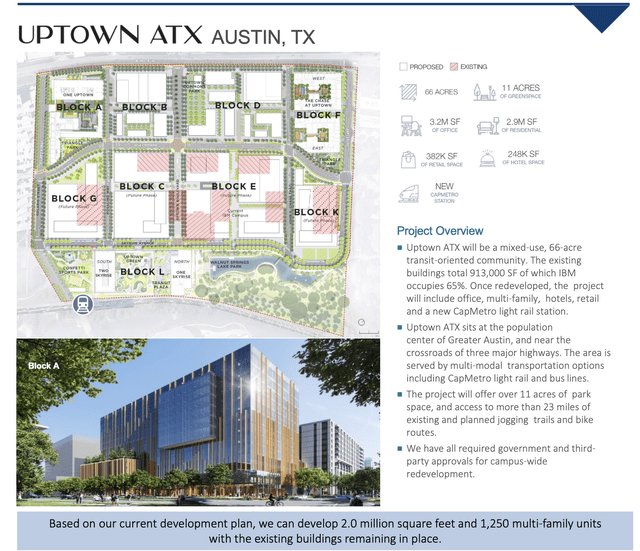

Still, there are multiple attractive projects coming, many of them in Texas.

BDN – Investor Relations

And remember, a huge mistake investors have made in the past is equating a downturn or trouble with the death of a city. BDN is trading as though its Philly NOI is heavily impaired and does not, or might not in the near future, follow its rent obligations or see massive vacancies.

There is very little data to support this assertion, both in earnings and macro. While we’re bound to see a decline in funds from operations, or FFO/AFFO (adjusted FFO) this year, that decline is nowhere near a level that would threaten the company’s ability to meet its obligations.

The company doesn’t have market-leading occupancies – it targets around 90-91% for year-end, and it does take into consideration that the CAD payout ratio (Cash Available for Distribution) rises above 100%, to around 105% (or as high as 95% on the low end).

That BDN is somewhat stretched in terms of payout this year is not open for debate. The assertion that they definitely will cut the dividend, however – that assertion is up for debate.

BDN has been busily diversifying its asset portfolio and seeks to present itself in a different light to take away from the office exposure risk. This is how the company presents its asset portfolio today, at least in terms of how its “land” portfolio is looking.

BDN – Investor Relations

Some fundamental attractions are very clear, though, even when considering the relatively one-sided Philly focus. The company has a relatively attractive lease expiration schedule for an office REIT. Around 50% of the company’s leases do not expire until 2029 or thereafter – with the closest double-digit ABR expiration in 2027. There are a few percent until then – around 30-40%, but spread out fairly well.

In my previous articles, I’ve also gone through the theoretical appeal of some of the REIT’s more ambitious projects – so look back at those for a description of the third-busiest railway station in the country, for instance.

And while the company has seen more pressure than other REITs in the same sector, and many of the aforementioned developments are currently on hold unless mostly/100% pre-leased, I still view these trends as temporary, not permanent.

The last set of results beat revenue estimates and came in line in terms of FFO. So while there is reason to look at some of the company’s metrics, coverages, and risks – the death knell that the market seems to want to assign to the business, just isn’t really there. Yes, BDN will likely have difficulties finding growth near-term. The reversal will have to be enough. The company also isn’t the safest REIT out there – no argument from me on that front.

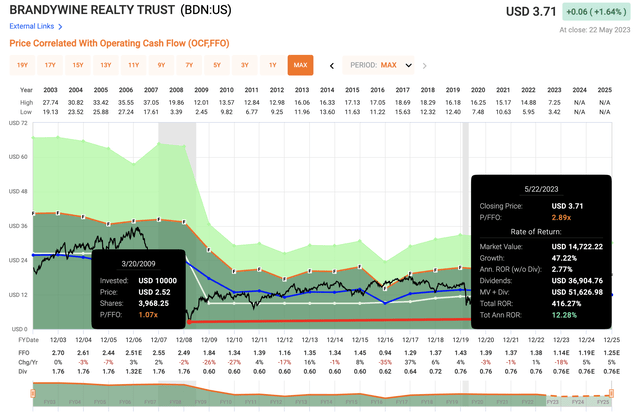

But the company has been in some cycles like this, most notably during the Great Financial Crisis, when the company at times traded below 1x P/FFO. Anyone who invested at that particular time, although you really should have sold in 2016-2017, has still beaten the market even today, thanks to the yield.

FAST Graphs

So, while some investors and analysts would like to characterize BDN as a massively risky play with the potential for complete loss of capital, that is not a stance I stand behind. Otherwise, I wouldn’t still be invested in the company.

In fact, if you have the right sort of risk tolerance, you could make annualized returns close to quadruple digits here, if things play out a certain way.

Obviously, this is not an investment for everyone. But I want to dispel the notion that this company is somehow facing fundamental impairment, because that is not the case.

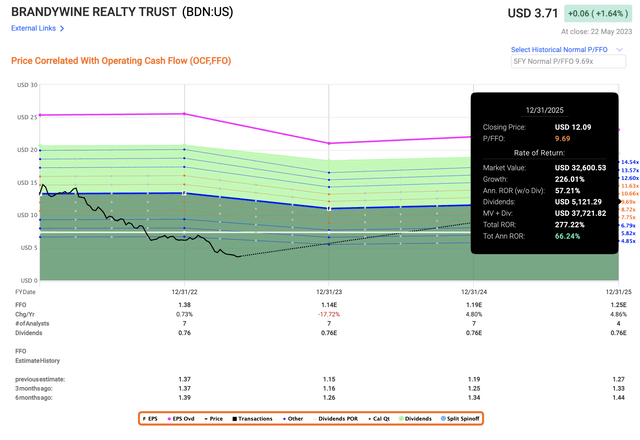

Brandywine Realty Trust Valuation – The Upside Is Massive

Simple full normalization until 2025E brings with it the potential of annualized RoR of 66%+ in less than 3 years, or 277%.

FAST Graphs

Is it likely?

Well, put it this way. It took less time for the company to decline from that level than 3 years. But no, I don’t consider it likely given the current interest rate and macro environment that will see a sub-par quality office REIT (compared to peers like Highwoods (HIW), Boston Properties (BXP), or Kilroy (KRC)) advance up to averages before its higher-quality siblings.

Will the company cut the dividend?

You should honestly count on it.

(iREIT added BDN to our Dividend Watch List.)

I say this despite the fact that BDN’s Q1 2023, reported in April, was actually a good quarter. Mark-to-market rental rates were at 14.95% on GAAP, and for the full year, it remains at 11-13%. The company did have early termination activity (renters leaving), but the quarterly GAAP on a same-store basis actually outperformed, and capital costs were in line with what’s expected in the business plan.

A look at occupancies.

From an occupancy and leasing standpoint, our Washington, D.C. portfolio continues to underperform. Conversely, our Philadelphia CBD, University City, Pennsylvania suburbs and Austin portfolios which cover 94% of our NOI are 91% occupied and 92% leased. So fundamentally operating platform is solid with a stable outlook. We have reduced our forward rollover exposure through 2024 to an average of 6.6% and through 2026 to an average of 7.4%. We continue to see the quality curve thesis play out as our physical tour volume has been very, very encouraging.

(Source: BDN earnings call.)

I want to highlight that we’re actually not seeing a softness that would justify the sort of valuation decline we’re seeing. The demand trend indicators are still solid – with tours actually above the quarterly average, as well as above pre-pandemic averages. The assumption that people are not interested in office space, or BDN’s office space is not backed by facts. Tenant expansion outweighs tenant contraction.

Total leasing is up 23% on a QoQ basis, with a good pipeline of over 3.3M sqft. The company’s focus is leasing and liquidity. On the liquidity front, the company has raised over $300M since YE22.

There is talk of looking at the dividend – and frankly, it would be irresponsible if there wasn’t discussion given a 20% yield that currently consumes much of what the company could be using on other fronts.

We kept the dividend at $0.19 cents for the first quarter. Certainly as our business plan progresses, the board will closely monitor capital market conditions, overall liquidity, sale activity progress and our payout levels as they evaluate the dividend going forward. We also from an additional liquidity enhancement plan to enter into 2 construction loans this year; one in our 100% fully leased 155 King of Prussia Road and our Life Science project in Schuylkill Yards later this year.

(Source: BDN, earnings call.)

As I said – you should expect a dividend cut.

And there is something to be said, perhaps, for waiting on that cut. On the other hand, if the board put its foot down and decides to weather the storm, then your opportunity to enter could be lost. It’s a question of your risk tolerance and expectations.

The simple fact is this, and this is somewhat of a quote from management. As long as the dividend is covered, the company will want to continue paying that.

The unknown variable here is the capital markets, which will influence this.

However, what I think is very important to point out is that even with a forecasted double-digit decline in AFFO that puts the annual AFFO down to $0.78/share, the dividend of $0.76 is still covered.

Obviously, this is far from an ideal situation. But beyond 2023, the expectation is back to growth – and currently, forecasts do not include a dividend cut.

BDN is massively undervalued. S&P Global analysts put the company at no more than $5.5, but this is still a 42.6% upside, and well below the average target of $15/share we saw around a year ago.

As you know, I don’t trust target changes like that without fundamental changes in the company’s safety – and while we have seen macro changes, I don’t believe that we’ve seen enough of a downturn change to warrant this sort of decline.

The company is currently trading very close to 0.25x to its NAV, which means that the market is more or less saying “Your properties are soon worthless.” The tenants and the underlying activity beg to differ, as do I.

I will give you my current thesis on BDN here.

Thesis

- Brandywine Realty Trust is perhaps one of the more volatile and pressured businesses in the Office REIT space out there today. However, all too often, and also often in this company’s history, pressure is mistaken for an actual risk of bankruptcy. That was not the case in the GFC, and I don’t believe it to be the case now.

- We need to be prepared for a right-sizing of the dividend – a 50% cut would de-risk the company insofar as payout goes, but the current signals about such a cut are unclear – I’m speculating here based only on yield, but the numbers and forecasts still make the dividend possible.

- BDN is one of the currently riskier REIT plays we have in our coverage spectrum. I give the company a minimum price target, or PT, of $10/share. It’s a spec “BUY,” and at iREIT our official PT is $10.5/share.

This play isn’t for everyone – but Brandywine Realty Trust stock is not as bad as some people seem to make it out to be. I expect that in a few years, we will be looking back on articles such as this one and thinking “I wish I’d put in $100k.”

Questions?

Let me know!

Read the full article here