Elevator Pitch

I assign a Hold investment rating to TPI Composites, Inc.’s (NASDAQ:TPIC) shares. TPIC’s FY 2023 outlook is lackluster, and I see the company taking a few years to get its business performance back on track. In that respect, it is fair to rate TPI Composites’ stock as a Hold for now.

Business Overview

On the company’s investor relations website, TPIC describes itself as an “independent manufacturer of composite wind blades” boasting a 38% share of “all sold onshore wind blades on a MW-basis globally excluding China” last year.

TPI Composites’ Key Facilities And Geographical Presence

TPIC May 2023 Corporate Presentation

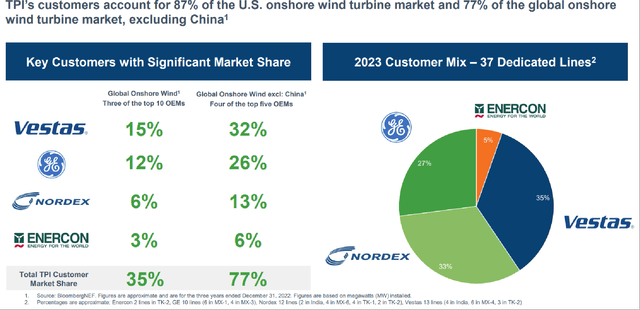

TPI Composites’ Client Profile And Mix

TPIC May 2023 Corporate Presentation

TPI Composites generated 92% of its full-year fiscal 2022 top line from wind blade sales as indicated in the company’s 10-K filing. TPIC’s global service and automotive offerings contributed the remaining 8% of its FY 2022 revenue. Mexico, EMEA (Europe, the Middle East and Africa), India and the US accounted for 43%, 37%, 14%, and 6%, of TPI Composites’ sales, respectively in the prior year.

Management Commentary Relating To 2023 Guidance Was Mixed

TPI Composites provided an update for the company’s fiscal 2023 financial guidance when it released its first quarter financial results and hosted an earnings call for analysts in early May.

TPIC didn’t make changes to its FY 2023 top line guidance in the $1.6-1.7 billion range, but it noted at its Q1 results call that the company’s actual revenue this year could potentially be “closer to the bottom end of our guidance range” as per the outcome of recent negotiations with clients. Assuming that TPI Composites’ top line in the current year is $1.6 billion, this will translate into a -9% revenue contraction for TPIC.

An April 17, 2023 CNBC news article highlighted that “the wind energy sector has been in crisis mode” due to “reduced tax incentives, rising interest rates and inflation”. As such, it is easy to understand why TPI Composites’ wind blades are expected to be lower in this year.

Separately, TPI Composites left its FY 2023 EBITDA margin guidance in the “low single-digit” unchanged, which indicates that its operating profitability for the current year should be inferior to that of FY 2022 (4.2% EBITDA margin).

However, TPIC guided at its most recent quarterly earnings call that Q2 2023 “will likely be the low-water mark for adjusted EBITDA margin”, as the positive effects of “productivity improvements and improving raw material and logistics costs” should be realized in 2H 2023. Management’s commentary is consistent with the sell-side analysts’ consensus financial projections. As per S&P Capital IQ’s consensus data, TPI Composites’ EBITDA margin is forecasted to decline from 2.1% in Q1 2023 to 1.9% in Q2 2023, before rising to 3.3% and 3.7% for Q3 2023 and Q4 2023, respectively.

In a nutshell, TPI Composites’ 2023 guidance and related management commentary imply that TPIC’s top line will continue to be under pressure in the near term, but its operating profitability is expected to reach a trough in the second quarter of the current year.

This Should Be A 2025 Story

TPIC is now valued by the market at a consensus forward next twelve months’ Enterprise Value-to-Revenue multiple of 0.57 times according to S&P Capital IQ’s valuation data. As a comparison, TPI Composites traded at between 0.75 times and 1.00 times consensus forward next twelve months’ Enterprise Value-to-Revenue between June 2020 and November 2021.

In my opinion, a substantial valuation multiple expansion is only likely to materialize when TPIC’s top line hits a meaningful milestone and its EBITDA margin improves significantly. It will take some time for TPI Composites to achieve a better set of financial results, and I view TPIC as more of a 2025 story.

At the company’s Q1 2023 results briefing, TPI Composites outlined its goal for its “wind revenue to eclipse $2 billion” and delivering “a high single-digit adjusted EBITDA margin” in “the next couple of years.”

TPIC currently boasts 37 wind blade production lines at the end of the first quarter of 2023 as indicated in its May 2023 corporate presentation. Looking ahead, the company targets to have the number of wind blade production lines increased to 44 by the beginning of 2025 as highlighted at its quarterly earnings call. Therefore, it is realistic to assume that TPI Composites’ intermediate term wind sales goal of $2 billion will most probably be attained in 2025.

Similarly, TPIC has a good chance of expanding its EBITDA margin from the low-single digit level now to the high-single digit range by 2025.

One key factor is the utilization rate of TPI Composites’ wind production facilities. TPIC’s wind production utilization rate was 84% in the first quarter of 2023, and the company’s medium target is to realize a higher utilization rate of 90% for the mid term. In my view, TPI Composites’ wind production facility utilization rate is expected to go up to 90% or higher in 2025, when its capacity expansion plans are completed (i.e. when the 44 production lines are in operation). An increase in utilization rate should lead to positive operating leverage, which will have a favorable impact on the company’s future profitability.

The other key factor is revenue mix. TPIC is also in a good position to realize higher operating profit margins by its sales mix. Specifically, TPI Composites’ asset-light global services business generates high-margin repair and inspection revenue streams (vis-a-vis its core wind blades business), and TPIC has plans to increase the revenue contribution of its global services businesses in the years ahead as disclosed in its May 2023 corporate presentation.

Closing Thoughts

2023 is expected to be a difficult year for TPI Composites, considering expectations of top line contraction and modest operating profitability. I think that a significant turnaround for TPIC will only happen in 2025. As such, a Hold rating for TPI Composites is appropriate, as a meaningful improvement in TPIC’s financial performance is less likely to happen this year or next year.

Read the full article here